Thesis

At one point in time, banking meant marble floors, long lines, and paper statements. In the 2020s, banking has become digital and mobile. While the COVID-19 pandemic forced consumers to shift online out of necessity, online banking remained popular in the post-pandemic period. In 2019, online banking was the primary method of account access for just 22.8% of US households, behind both mobile banking and in-person teller visits. By 2024, that number had reached around 70%.

The rise of digital banking normalized consumer expectations for instant access and mobile-first financial management. Furthermore, once they experienced the accessibility and ease of digital banking, consumers began to expect it from every financial service. In 2022, 78% of customers who used embedded financial services (i.e., financial tools built into non-financial products) said they were likely to use similar services again.

Consumer-facing companies have been quick to adopt embedded finance services due to both changing consumer expectations and the opportunity to expand their business models. From 2023 to 2024, independent software vendors offering both payment acceptance and embedded finance features increased 72%, while in 2024, over 50% of marketplaces that did not provide embedded financial services said they planned to add them within the following year. Meanwhile, a 2024 survey of 500 senior US executives found that 82% were planning or considering expanding their embedded finance capabilities.

As adoption of these products with embedded financial services has grown, so has demand for chartered banking partners. Non-bank financial institutions need a chartered banking partner to obtain the legal authority to provide core banking functions, such as direct payment rails with the Federal Reserve, issuing accounts or cards, and supplying FDIC insurance. The number of chartered banks has fallen roughly 50% between 2005 and 2025. Meanwhile, approval rates for new bank charters dropped precipitously after the 2008 financial crisis: from 2005 to 2007, about 170 charters were approved per year. This dropped to just 7.5 on average in the post-GFC era from 2009 to 2024, representing a ~96% drop.

Compounding the issue, in 2024, among the approximately 60 top banking-as-a-service (BaaS) sponsors, which are chartered banks that provide non-bank companies access to their banking license, only 50% had more than one partnership, and 10% had more than ten. With 81% of executives reporting in 2024 that offering embedded financial services was somewhat or significantly more complex than expected, demand for not only a chartered banking partner but also one with easy-to-use technological integrations is high.

Designed specifically to address this market gap, Lead Bank is a Missouri state-chartered bank that expanded from a small community lender outside Kansas City into a national BaaS sponsor. It is an FDIC-insured bank that lets fintech and consumer companies embed banking features such as loans, cards, and accounts directly into their own products via API integrations. Companies can adopt core banking features through Lead Bank’s platform, with options for traditional business and consumer banking to deliver a full-service solution.

Founding Story

The current iteration of Lead Bank was formed in August 2022 through a $56 million acquisition of Lead Bank by Luna Parent, a holding company. Lead Bank was co-founded by Jackie Reses (CEO and Chair), Ronak Vyas (Chief Technology Officer), Homam Maalouf (Chief Product and Data Science Officer), and Erica Khalili (Chief Legal and Risk Officer).

Prior to this, Lead Bank was originally chartered as Garden City Bank in 1928. Then, CEO Josh Rowland re-founded the entity as Lead Bank in 2010, following five years of declining community-bank performance after his family took control of the company. By the time he sold the company in 2022, Rowland had turned it into the 22nd-largest bank in the Kansas City area by deposits and begun expanding into fintech partnerships. While Rowland and the previous leadership team were expected to remain in their positions following the acquisition, Reses and her co-founders soon took over.

Born into a family of entrepreneurs, Reses started multiple businesses while at Wharton to help pay for her tuition. After graduating, she began her career in investment banking at Goldman Sachs before joining the private equity firm Apax Partners, where she became a partner and the head of the firm’s media group. On the corporate side, she worked at Yahoo before joining Square, where she served as executive chair of Square Financial Services while leading Square Capital, the small-business lending unit.

Reses was frustrated with Square’s banking partnerships because sponsor banks typically used legacy technology, making it difficult for partner fintechs to customize customer transactions. She eventually applied for Square to become an Industrial Loan Company (an alternative to the standard banking charter in certain states that allows banking services without Federal Reserve regulation), leading Square to become one of just two ILC charters approved in the last 19 years as of November 2023.

After leaving Square and spending time angel investing in fintechs, Reses looked to try her hand at entrepreneurship. In a March 2025 interview, she said, “One of the problems I’ve seen is that fintechs have put a beautiful sheen on the front end of an app to make financial services easier. And I think we’ve all felt that with fintech apps that we use; the infrastructure, however, is terrible.” Using the holding company Luna Parent, backed by Coatue, Ribbit Capital, Andreessen Horowitz, and Zeev Ventures, Reses focused on Lead Bank for its combination of small size and early adoption of a banking-as-a-service offering, and acquired it in August 2022.

After acquiring Lead Bank to use its charter as the foundation for a technology-focused product, Reses called on many of her old colleagues from Square; each of her co-founders is a former Square Financial Services executive. Reses also looked to fintech executives she had befriended over her career, including longtime friend Kristine Dickson, who served as Chief Financial Officer before Auspaker’s October 2025 transition, and Chief Design Officer Albert Song, with whom Reses had previously worked at Yahoo.

Other than Chief Operating Officer Brooke Clouse, who started her career at Lead Bank as a teller in 2008, Reses has focused on recruiting fintech executives with strong industry connections to source future business partnerships. Part of this has been through Lead Bank’s remote-first work policy, which has allowed executives, including Reses, to remain in Silicon Valley rather than relocate to Kansas City. Chief Financial Officer Ken Auspaker, who joined in October 2025, is another example, having previously served as Chief Business Officer at deposit-network fintech IntraFi and before that as a managing director in Evercore’s financial technology investment-banking group.

Product

Source: dashdevs

Lead Bank is an FDIC-insured, state-chartered bank that provides both a full-service bank for businesses and consumers and a banking-as-a-service (BaaS) platform for fintechs, consumer companies, and digital asset firms. Its modular, API-driven infrastructure lets partners assemble the banking capabilities they need, including lending, card issuing, FDIC-insured deposit accounts, and payment transfers, and integrate them directly into their own products. Lead Bank has also expanded into crypto, offering payments, custody, and settlement services to digital asset companies.

BaaS Partner Platform

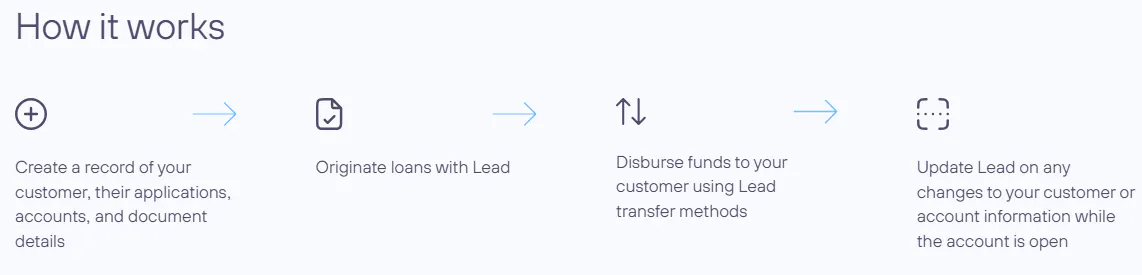

Lead Bank’s primary product is its BaaS Partner Platform, which provides fintech companies with a regulatory foundation and banking/payment infrastructure to offer traditional and embedded financial products. The platform can be broken down into four core products: lending, transfers, cards, and accounts.

The platform allows non-chartered companies to originate and distribute both term loans and lines of credit, supporting both secured and unsecured loans for commercial and consumer customers. The partner company can choose more complex loan structures, such as buy-now-pay-later and fee-based lending products. After loans are originated with Lead Bank, funds can be disbursed directly to the customer through Lead Bank’s transfer services.

Source: Lead Bank

The platform’s transfer offerings are among the features that motivate fintechs to seek chartered partners in the first place, providing them with a direct connection to the Federal Reserve. All chartered banks have a master account with the Federal Reserve that enables them to hold reserves and send or receive money through the government-operated national payment networks.

Banks use three main transfer rails (the infrastructure that allows for transfers) through the Federal Reserve: Fedwire for real-time, high-value transfers between banks; Automated Clearing House, or ACH, for batch processing of credits and debits; and FedNow, an instant payment network open 24/7. Lead Bank’s platform supports APIs or files, offers multiple settlement options, and provides a direct connection to the Federal Reserve. Partners can offer transfers and payments with real-time, same-day, or next-day settlement options. In other words, partner companies are using Lead Bank’s BaaS Partner Platform to rent its Federal Reserve master account access to offer payments, deposits, and transfers themselves via the US banking system.

Lead Bank’s partner accounts can send and receive funds using ACH, domestic wires through Fedwire, internal transfers among Lead Bank accounts, and checks, with an international wire offering set to release.

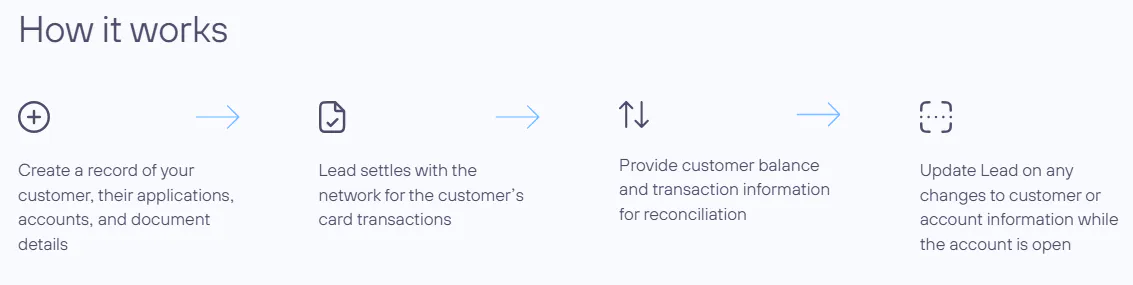

Partners can also offer branded debit, prepaid, or credit cards through the platform. Lead Bank provides flexible Banking Identification Number (BIN) sponsorship and the issuing processor of the partner’s choice. Licensed banks issue BINs to identify the bank responsible for the card and underlying account, a requirement for card offerings. Lead Bank’s flexible platform allows the partnering company to choose its preferred tech stack through an issuing processor (the technology company that connects the non-bank’s front-end software to the card network and bank systems), and Lead Bank’s integrations support the selected processor’s APIs. Lead Bank supports both consumer and commercial card selections, originating receivables, processing settlements with card networks, and providing program oversight to ensure regulatory compliance.

Source: Lead Bank

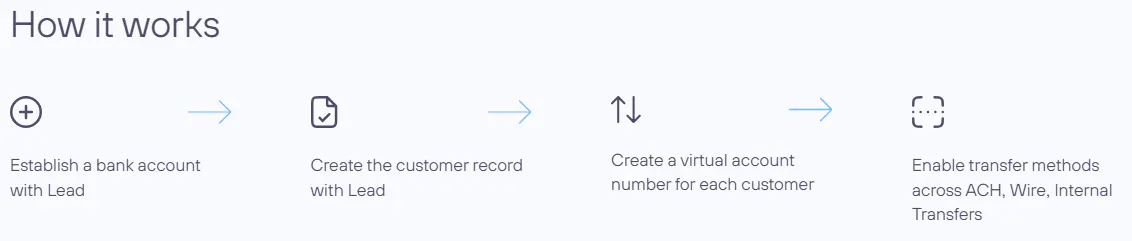

Lead Bank’s final BaaS product offering is accounts, supporting two FDIC-insured account types: Virtual Account Numbers and For Benefit Of (FBO) Accounts. Virtual Account Numbers allow a fintech partner to create multiple account numbers for their consumers that all map to a single account. This makes it easier to track and reconcile payments and deposits by assigning different permissions and limits to other accounts and using them for different purposes. FBO accounts enable a company to manage funds on behalf of its customers, improving regulatory compliance through fund segregation.

Source: Lead Bank

As of May 2026, Lead Bank had a network of 23 program banks: FDIC-insured partner institutions that hold customer deposits originating from fintechs or brokerages, providing maximum regulatory coverage. Program banks “sweep” funds collected by a financial intermediary like Lead Bank into accounts to maximize FDIC insurance for end-users, diversify counterparty risk, and increase deposit capacity.

While each product offering in the BaaS Partner Platform is distinct, they are commonly used in conjunction. One such use case is enabling users to move funds between bank accounts and cryptocurrency wallets. Using FBO accounts and Lead Bank’s payment rails, partner companies can provide on-ramps and off-ramps by transferring fiat currency to the account to purchase cryptocurrency, and transferring fiat currency back to the user account after the cryptocurrency has been exchanged.

Another cross-product use case is digital banking. Partners can open accounts for their customers and offer the same capabilities as a traditional bank. Debit or credit cards can be issued with BIN sponsorship; consumers can take out loans, receive direct deposit, and initiate payments. The platform’s customizable API integrations allow the product to be tailored to the partner’s preferences, integrating cleanly with their existing platforms or offerings.

Business Banking

While Lead Bank’s focus is on its fintech partner platform, it also leverages its full-service banking capabilities to offer both business and consumer banking. Lead Bank’s business offerings include checking, savings, investments, and commercial loans.

Lead Bank offers two business checking account types, both with online and mobile banking. The All In Business Checking account has a higher initial minimum deposit and unlimited analyzed transactions, while the Essentials Business Checking account has a lower initial minimum with limited free transactions. The more premium account, All In Business Checking, is FDIC-insured, offers IntraFi Network Deposit accounts, and charges fees based on account activity.

Lead Bank also offers money market accounts and certificates of deposit to businesses looking to earn interest on their savings. Both have a $2.5K minimum to open, with money market accounts offering unlimited transactions and no maintenance fees for balances over the initial requirement (and a five-dollar monthly fee for balances below $2.5K). Lead Bank also offers business loans, with terms and amounts subject to the discretion of its business banking team. Lead Bank’s business banking offerings are more of an upsell to fintech partners who use Lead Bank’s platform to bank on behalf of their customers than a competitive offering compared to traditional business banking platforms.

Personal Banking

Lead Bank offers national personal banking solutions digitally, with two in-person banking locations in Missouri. Its personal banking offerings are similar to its business banking offerings, including checking, savings, investments, and lending solutions.

The products themselves are structured similarly, with checking as an example. Consumers can choose between a premium account with no fees if a minimum balance is maintained, and an elementary account that charges fees after a small number of free personal checks. Lead Bank also offers personal money market accounts and savings accounts with no fees and unlimited transactions.

Customers looking to invest can use certificates of deposit and health savings accounts (HSAs). Certificates of deposit are structured the same as their business counterparts, while HSAs are available to individuals covered by a high-deductible medical plan. HSA accounts are used to accumulate tax-free funds that can be used to pay non-reimbursed medical expenses. Individuals can also take out personal loans, home equity loans, and mortgages.

Market

Customer

Lead Bank focuses on fintech companies without a banking charter that are looking to provide banking services. These companies can use Lead Bank’s partner platform to offer those services in compliance with regulatory requirements, rather than applying for or acquiring a banking charter themselves. While Lead Bank’s full fintech partner list is not public, the disclosed companies fall into two groups: consumer and SMB-facing fintech platforms, and cryptocurrency companies.

Examples of fintech companies that use Lead Bank’s BaaS Partner Platform include Ramp* and Affirm. Ramp, a corporate finance automation platform, leverages Lead Bank’s card-issuing capabilities to provide its business customers with branded charge cards, with Visa as the payment processor.

Affirm, a buy-now-pay-later fintech, uses multiple platform features, including lending, accounts, and transfers, for the infrastructure behind its consumer loan products. Affirm is a case study of the integrated BaaS platform offering at scale. Using multiple platform features, Affirm provides a user-friendly interface via Lead Bank’s API integrations that lets consumers split purchases into smaller installments. Affirm relies on a small group of originating bank partners, including Lead Bank, to originate loans facilitated through its product offerings, which amounted to $21.5 billion in fiscal year 2024.

Digital-asset companies working with Lead Bank include Bridge and Revolut. Lead Bank has been one of the first chartered banks willing and able to operate in the heavily regulated digital-asset space. Bridge, a stablecoin orchestration platform owned by Stripe, partnered with Lead Bank and Visa to launch stablecoin-linked card-issuing solutions for fintech developer clients. Lead Bank issues the cards, which allow end consumers to make purchases using a stablecoin balance at Visa-supported merchant locations.

In March 2026, the partnership expanded with plans to reach over 100 countries, with Lead Bank also serving as the participating bank in Visa’s on-chain stablecoin settlement pilot. Revolut, a global neobank offering full-service digital banking solutions, uses Lead Bank’s infrastructure to provide banking services in the United States, including card issuance and cryptocurrency trading.

Market Size

In 2023, the global banking-as-a-service industry was valued at nearly $16 billion and projected to grow roughly fourfold over the following decade. While Lead Bank operates only in the US, North America was the largest market in the global BaaS industry in 2021 by market share, accounting for 34.1% of revenue.

The BaaS market’s growth is being driven by the rapid expansion of embedded finance. Embedded finance in the US alone was estimated to be worth $20 billion in 2024, while traditional banks are projected to lose about $60 billion in annual revenue to embedded finance by 2028 as customers increasingly access financial products through non-bank platforms. Over 84% of fintech companies were already using bank-provided APIs to deliver financial solutions as of mid-2024, a trend that benefits BaaS providers like Lead Bank, who serve as the licensed, compliant backbone behind those products.

Meanwhile, the complex regulatory environment and dwindling number of chartered banks in the US are pushing the BaaS market toward a select group. While community banks have explored BaaS offerings to generate additional revenue as community-bank performance has stalled in the years since the global financial crisis, few are willing, and few have the scale or the technology, to take advantage of this market opportunity. Among the roughly 60 top BaaS sponsors, chartered banks that provide non-bank companies access to their banking license, only 50% had more than one partnership as of 2024, and 10% more than ten.

Competition

Competitive Landscape

As the BaaS landscape continues to mature, the key players fall into two groups: sponsor banks and middleware providers. In the early years of the industry, small community banks exploring BaaS sponsorship did not have the resources to build out their own technology. This led to the creation of middleware providers that developed API layers and developer-friendly documentation to enable easy integration of regulatory infrastructure into a customer’s product offering.

As sponsor banks have continued to grow in the market, some have begun building their own technology platforms. Developers have also taken notice and created chartered BaaS sponsor technology platforms as a differentiator. Lead Bank is one example, emphasizing in-house technology development to avoid reliance on middleware providers for customer success.

Middleware providers are still a key component of the BaaS landscape despite the emergence of tech-forward banks. They provide multi-bank connectivity, allowing fintechs to mix and match different products from different sponsors; program management functions such as risk scoring, compliance-as-a-service, and KYC/KYB tooling; and scalability for smaller fintechs that cannot manage direct bank relationships. Smaller community banks looking to grow revenue without the resources to build out a BaaS division can use middleware providers to match with fintech partners. While middleware providers have a very different product from tech-first banks like Lead Bank, the two compete for the same customer.

Larger banks have also taken notice of the space and expanded their offerings accordingly to preserve their full-service, one-stop-shop nature. These embedded finance products, however, are often more general than direct BaaS sponsorship; they are targeted toward larger companies and overlap only briefly with the startup-focused traditional BaaS sponsors. An early adopter was JPMorgan, which provided payments APIs and end-to-end embedded finance solutions to companies like Walmart to power marketplace payouts.

Tech-focused sponsors like Lead Bank have the advantage of controlling their own technology. This allows them to eliminate the middleware provider’s cut of partnership fees. They can also offer clients full-service banking solutions, unlike middleware providers, allowing both business and consumer finances to be managed by the same bank.

Sponsor Banks

Cross River Bank: Cross River, founded in 2008, is a New Jersey-chartered bank that provides a technology-focused BaaS platform with API integrations. Similar to Lead Bank, Cross River provides comprehensive banking services encompassing everything from lending and payments to card issuance and digital-asset solutions.

Cross River raised a $620 million Series D in March 2022, co-led by Andreessen Horowitz and Eldridge Industries at a post-money valuation of over $3 billion. As of May 2026, the company had raised $908 million in total funding from investors including KKR, Shefa Capital, and VCI Global. Cross River and Lead Bank share similar technology-driven API platforms and target customers, both focusing on large fintechs and cryptocurrency firms, but differ in scale: Cross River is better-established, with more capital and a larger balance sheet.

Celtic Bank: Celtic Bank, founded in 2001, is a Utah-based chartered bank known for providing lending infrastructure to partners. Celtic handles loan origination, underwriting, and compliance, while its fintech partners offer the loan to the end user. Celtic has not raised outside funding and is privately held. The difference between Lead Bank and Celtic is in their products: Celtic specializes in lending, one of Lead Bank’s four BaaS platform offerings, while Lead Bank offers a more comprehensive product that lets fintechs partner with a single sponsor. Celtic also relies on middleware providers and does not run its own technology integrations.

Evolve Bank & Trust: Evolve, established in 1925, is a long-standing community bank that emerged as a major BaaS player in the early 2020s. It launched its Evolve Open Banking division in 2017, providing partners with regulatory infrastructure to offer banking services. Evolve relies on middleware partners to provide integrations to fintech partners and can offer a multi-partner approach through them.

Known for its card-issuing offerings, it works with companies like Mercury, Stripe, and Marqeta. The bank is privately owned and has not raised outside capital. In April 2024, Evolve’s middleware provider Synapse filed for bankruptcy, leading Evolve to freeze customer accounts and the eventual reported disappearance of funds, a clear example of the risks of middleware-provider reliance for BaaS sponsors. The key differences between Evolve and Lead Bank are Evolve’s reliance on middleware providers and card specialization.

Middleware Providers

Unit: Unit, founded in 2019, is a banking-as-a-service middleware provider. Its platform provides APIs and software modules that non-financial companies can embed in their products to offer financial services. Unit handles compliance and partner-bank integrations. The company raised a $100 million Series C in May 2022, led by Insight Partners, at a post-money valuation of $1.2 billion. That round brought its total funding to $169.6 million, where it remained as of May 2026, with backers including Accel and Better Tomorrow Ventures. Similar to other middleware players, Unit differentiates itself from competitors like Lead Bank by the depth of its banking-partner network, which allows for greater flexibility.

Synctera: Synctera, founded in 2020, is a middleware provider with a platform that connects fintech companies with community banks, providing the software infrastructure for fintech banking products. Synctera raised a $15 million Series A extension in March 2025, co-led by Fin Capital and Diagram Ventures. This brought the company’s total funding to $94 million, where it remains as of May 2026. As a middleware provider, Synctera offers a broad platform with many community bank partners and primarily targets early-stage startups.

Treasury Prime: Founded in 2017, Treasury Prime is a banking-as-a-service software platform that connects fintech companies to a network of chartered banking partners via APIs. The platform provides a single API that lets developers open bank accounts, issue cards, and move money on their own platforms, while Treasury Prime handles compliance and connections to partner banks. Treasury Prime raised a $40 million Series C in February 2023, its latest round as of May 2026, led by BAM Elevate, bringing total funding to $71.5 million, with investors including QED Investors and Y Combinator. While Lead Bank offers a platform with itself as the sole partner bank, Treasury Prime offers connections to a network of partner banks, allowing fintechs to choose the optimal geographic, regulatory, and product mix for their platform.

Legacy Banks

JPMorgan: JPMorgan Chase, founded in 1799, is a global financial services provider offering consumer and commercial banking, investment banking, asset management, principal investing, and more. While not a traditional BaaS provider, JPMorgan has in-house capabilities that compete with BaaS offerings, such as transaction banking APIs. The company is among the world’s largest and had a market cap of approximately $798 billion as of May 2026. Unlike the fintech disruptors Lead Bank works with, JPMorgan focuses on larger corporate clients.

Goldman Sachs: Goldman Sachs, founded in 1869, is a leading global investment banking and financial services company. Goldman has expanded into consumer and transaction banking, but targets banking-as-a-service with a small number of consumer-brand partnerships. One example was the Apple Card, Apple’s credit card, launched in 2019, with Goldman as the banking provider. In 2020, Goldman formally announced a BaaS strategy, offering APIs to corporate clients to deliver banking solutions through its Marcus platform. Goldman had a market cap of approximately $279.2 billion as of May 2026. Its approach differs from Lead Bank’s in target customer: Goldman prefers consumer-facing brand partnerships at scale rather than serving the long tail of fintech companies.

Business Model

According to an unverified estimate, Lead Bank primarily earns revenue through its BaaS Partner Platform. While its exact monetization strategy is not disclosed, revenue is likely a combination of recurring sponsorship fee income tied to user counts, transaction-volume fees on payments and card interchange, and net interest income earned on deposits held for partners. Lead Bank also earns revenue from its business and personal banking offerings. Many of these products are structured with a premium tier that carries higher fees and a basic tier with limited features and fees for additional uses.

An unverified estimate put Lead Bank’s adjusted revenue at $124 million in 2025, up 65% from $75 million in 2024, with non-interest income roughly doubling to $56 million as the platform business scaled. According to the same estimate, non-interest income had grown to roughly 45% of total adjusted revenue, up from 35% in 2023, consistent with the platform’s stated emphasis on sponsor-fee and interchange income.

Traction

Lead Bank grew quickly following its re-founding in 2022, reaching $37 million in revenue and $5 million in net income in the third quarter of 2023. The company’s net income of $11.8 million in the first three quarters of 2023 represented an 86% increase from pre-acquisition metrics two years prior, and total assets reached $951 million. One unverified estimate of Lead Bank’s 2025 performance put adjusted revenue at $124 million, up 65% year over year, and total consolidated assets at roughly $2.6 billion as of December 2025.

The company has also continued to announce material new fintech partnerships. In April 2025, Lead Bank was named the card-issuing provider for Bridge and Visa’s stablecoin-linked card product. In July 2025, Lead Bank added a partnership with workforce-payments platform Branch (whose customers include Uber and Instacart) to power Branch’s financial solutions, including the Branch app, debit card, and white-label products. In March 2026, the Bridge and Visa partnership expanded toward a 100-country rollout, with Lead Bank also acting as the participating bank for Visa’s on-chain stablecoin settlement pilot.

Valuation

Lead Bank announced a $70 million Series B in September 2025, co-led by ICONIQ Capital and Greycroft. The round valued the company at $1.5 billion, with existing investors Ribbit Capital, Coatue, Khosla Ventures, Andreessen Horowitz, and Zeev Ventures participating. For comparison, the Reses-led iteration of Lead Bank was acquired in August 2022 for $56 million; its Series B represented a 26x growth in the company’s valuation in three years. Lead Bank noted that the Series B proceeds would be used to bolster its balance sheet and expand its technology stack.

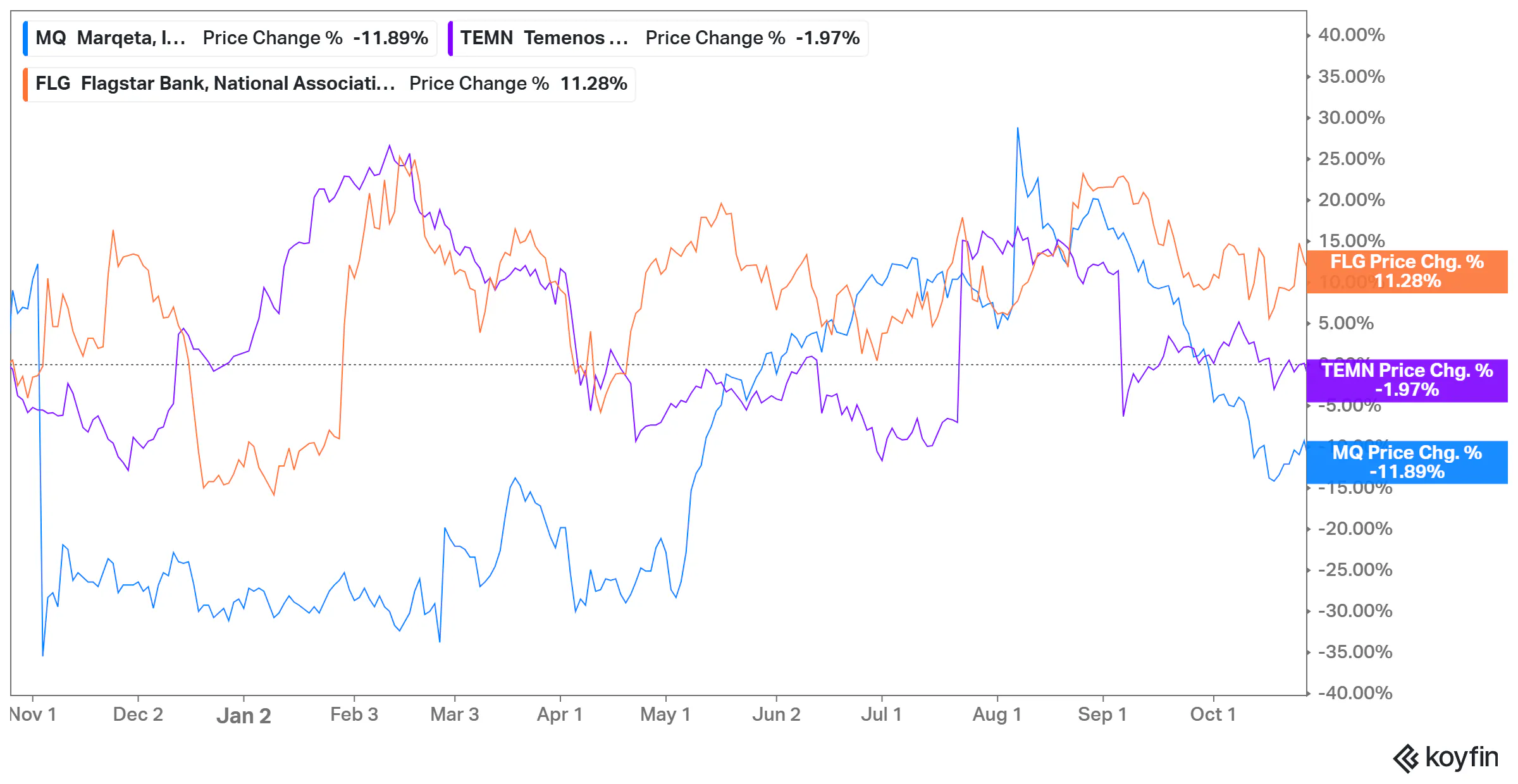

Because BaaS sponsor banks are typically smaller community banks, there is no clean publicly traded comparable to Lead Bank. The closest candidates are Marqeta, Temenos AG, and Flagstar Financial. Marqeta is known for payment processing services, but identifies its Marqeta for Banking BaaS platform as a growth area. Temenos AG is a Swiss publicly traded software company that provides embedded-finance solutions, weighted more toward software than a pure-play BaaS operator like Lead Bank. Flagstar Financial is a mid-size regional bank whose BaaS offerings are an insignificant share of its overall financials but is the closest publicly traded company to a sponsor-bank business.

Marqeta and Temenos have tracked general public market sentiment toward the fintech sector over the past year, while Flagstar Financial has been somewhat insulated as a regional bank. Following the reset phase in fintech valuations in 2022 and 2023, investors are showing renewed confidence in fintech companies in 2025 and 2026, focusing on path to profitability and quality of business model rather than the growth-at-any-cost framing of 2020 and 2021. Sub-sectors that generate sticky revenue and face high barriers to competition, such as BaaS, remain favored but are subject to industry volatility.

Source: Koyfin

Key Opportunities

Product Expansion

One disadvantage of Lead Bank as a sponsor bank is the lack of product depth relative to middleware providers, which offer a network of partner banks for customers to mix and match products from. As Lead Bank continues to expand its BaaS Partner Platform, it will appeal more to clients seeking specific services. One opportunity Lead Bank identifies on its website as coming soon is the ability to offer international wires. This would attract companies with a primary international client base, expanding payment volume processed by Lead Bank. Lead Bank noted that its Series B funding round would be used to bolster its balance sheet and expand its technology stack, suggesting further product investment.

Vertical Specialization in Digital Assets

Lead Bank is one of the few sponsor banks willing to take on regulatory-complex cryptocurrency clients. As digital-asset companies continue to expand, fueled by legislation like the GENIUS Act (which President Trump signed into law in July 2025, with full effect expected within 18 months) and shifting consumer sentiment, Lead Bank’s positioning as a go-to banking-infrastructure provider for the industry is a real growth lever. The Bridge and Visa stablecoin-card partnership expanded in March 2026 toward a 100-country rollout, with Lead Bank participating in Visa’s onchain stablecoin settlement pilot. Lead Bank’s technology focus lets digital-asset customers form close relationships with their sponsor bank without sacrificing developer experience.

Cross-Selling Full-Service Banking

An advantage of Lead Bank is its business and personal banking services. As a chartered bank, Lead Bank can upsell its fintech BaaS partners on its business banking offerings, allowing fintechs to bank for themselves and their customers with the same institution. This would expand lifetime value per customer without inflating already front-loaded customer acquisition costs. With a larger balance sheet following its September 2025 Series B, Lead Bank can provide lending and deposit products to its biggest customers.

Key Risks

Compliance Risk

While fintech partners are responsible for executing financial services with their end-customers, chartered banking sponsors handle the regulatory accountability for customer laws and protections, since the government views the fintech end-consumer as the bank’s customer relationship. With Lead Bank’s willingness to take on the challenging regulatory environment of digital-asset companies, this risk is material to its business model. Competitors have been burned by it: in June 2024, the Federal Reserve penalized Evolve Bank for failing to monitor and manage the risks of its relationship with Synapse. Further back, in March 2023, Cross River Bank entered a consent order with the FDIC for unsafe practices that required it to strengthen its lending program and third-party oversight. Lead Bank has taken steps to address this, including a September 2025 collaboration with blockchain data provider Chainalysis to enhance its compliance capabilities.

Customer Concentration Risk

Lead Bank’s large fintech partners are also a concentration risk. Affirm, the largest disclosed customer, relies on a small group of originating bank partners (Lead Bank, Cross River, and Celtic), and facilitated $21.5 billion in total loan originations across that group in fiscal year 2024. Lead Bank’s share of that volume is not disclosed, but the dependency runs in both directions, and a loss or migration of any single anchor customer like Affirm, Ramp, or Bridge would materially affect Lead Bank’s revenue trajectory. The company’s strategy of partnering with category-leading fintechs concentrates its book in a small number of names. The trade-off is real: each named partnership accelerates the platform’s flywheel, but the same partnerships compress diversification.

Technology Risk

Lead Bank has developed its own partner platform rather than relying on middleware providers, leading to higher technology investment costs. This has been a recurring use of investor capital. As the regulatory landscape of the fintech and cryptocurrency industries continues to change, Lead Bank’s platform will need to change with it. That requires continued high-tech investment and exposes the company in challenging macroeconomic environments that hinder capital raising.

Competitor Risk

With only a handful of companies positioned to offer BaaS capabilities, Lead Bank has operated with limited competition and grown quickly. However, as the industry gets more attention, competition is increasing. As of 2026, Lead Bank competes directly with peers like Cross River Bank, which targets the same big-name fintech clients. Smaller community-bank sponsors also pose competition, as they can move faster through middleware providers than Lead Bank, which develops its technology in-house. Lead Bank’s advantage is the opportunity to develop a direct, unintermediated relationship between fintech partners and a single sponsor bank.

Summary

With the shift to digital banking and online consumer commerce, embedded financial services have become increasingly ubiquitous. Changing consumer expectations have created an opportunity for sponsor banks like Lead Bank that combine a chartered balance sheet with a tech-forward API platform. Led by an executive team of experienced fintech operators and backed by full-service banking capabilities alongside its BaaS platform, Lead Bank is looking to capitalize on that opportunity.

*Contrary is an investor in Ramp through one or more affiliates.