In the last year, few industries have captured cultural, regulatory, and investor interest to the same degree as prediction markets. Platforms like Kalshi and Polymarket, which have millions of active users worldwide as of July 2026, facilitate peer-to-peer trading on future event outcomes for a small fee on each contract traded. These companies are now valued in the tens of billions of dollars and continue to expand across geographies and event categories, even as their regulatory status remains contested.

Such platforms are not built around fundamentally new ideas. Previous iterations of today’s prediction markets have included academic exercises, internal company markets, and commercial platform versions. All of them failed to gain traction with users and approval from regulators for decades. Understanding whether today’s prediction markets will succeed requires looking back at the history of such markets and evaluating the current evolving regulatory landscape and consumer appetite for gambling.

Specifically, it is critical to understand the differences between prediction markets and traditional sports betting, including the differences between the regulatory treatment and business model of each. Perhaps most important in this comparison is the dramatic skew in win distribution on prediction market platforms compared to sportsbooks. This skew largely governs user experience and long-term traction of the products compared to gambling-adjacent alternatives. In this piece, we break down the mechanics of prediction markets and the challenges companies face in building a product that consumers or regulators prefer over existing alternatives.

What are Prediction Markets?

Prediction markets are peer-to-peer exchanges in which users can bet on the outcome of future events by buying or selling contracts. Each contract’s pricing reflects the market’s assessment of the probability of the event resolving with a particular outcome; an event that is likely to occur may have a contract selling for $0.90 to pay out $1.00 at resolution (roughly equating to a 90% probability of occurring according to the market), whereas an unlikely event may have a contract selling for $0.10 for the same payout (~10% probability).

As of July 2026, prediction markets are not legally considered betting or gambling markets in the United States. Companies that operate prediction markets frame themselves as fairer and more transparent than sportsbooks, which use models to set odds and actively bet against customers by acting as the “house”; in contrast, prediction markets claim to simply provide a marketplace for individuals to bet against one another with no incentives for markets to resolve to particular outcomes.

Public opinion on prediction markets has been mixed. A poll issued by Kalshi itself in September 2025 found that 70% of Americans believed people should be able to "invest" in specific event outcomes such as presidential elections or agricultural yields, and 89% viewed contracts in stocks, mutual funds, and commodities as "financial investments" rather than "gambling." The survey did not mention sports among the event contracts it described, though sports contracts account for over 90% of trading on the platform. Adding further irony is the fact that the company has argued elsewhere that polls are not reliable.

Other polling from sources with less apparent bias has been far less favorable. A 2026 National Council on Problem Gambling (NCPG) survey found that nearly half of Americans consider prediction markets comparable to gambling, versus just 27% who liken them to investing. It also found broad support for guardrails: 84% believed prediction market platforms should be treated like gambling when it comes to consumer protections, and 82% said platforms where people risk money on future outcomes should be required to offer responsible-gaming tools such as deposit limits, cooling-off periods, and access to help resources.

History of Prediction Markets

While public interest in, and opinions on, prediction markets are relatively new, the concept has existed for decades in academic, corporate, and public arenas. Listed below, in chronological order, are the most significant projects in the prediction market space over the last several decades.

The Iowa Electronic Markets: Established in 1988, the Iowa Electronic Markets are collectively considered the first institutional prediction market. The IEM are a system of real-world event contracts traded for real money on an exchange operated by the University of Iowa Tippie College of Business as a non-profit academic data source. The IEM still operate today, but is not legally regulated due to the small volumes of most markets.

TradeSports / Intrade: Founded in 1999, TradeSports and Intrade were Ireland-based exchanges founded by John Delaney that specialized in sports wagering and non-sports event contracts, respectively. From 2002 onward, Intrade's political contracts, especially on US elections, made up the majority of trading activity, and Intrade users earned a reputation for uncanny accuracy, correctly anticipating the capture of Saddam Hussein, the 2005 papal succession, and the electoral result in 49 of 50 states in 2012. Tradesports itself wound down in the late 2000s after the Unlawful Internet Gambling Enforcement Act of 2006 made it nearly impossible for American users (the bulk of the Tradesports customer base) to move money to online gambling sites, leaving only Intrade in operation. The CFTC sued Intrade in late 2012 over unregistered options trading, forcing the company to bar American traders and ultimately suspend trading entirely in March 2013.

NewsFutures: Founded in May 2000, NewsFutures was another early prediction market, which ran entirely on play money rather than cash. Operational for nearly a decade, NewsFutures listed contracts on more than 120K events across politics, finance, and sports. The platform also co-branded its sports and money markets with USA Today. NewsFutures lent credibility to the play-money model that many corporations would later adopt for internal forecasting, where cash betting is often prohibited, after 2003–2004 NFL season forecasts on NewsFutures were found to be equally accurate to the real-money predictions of another platform, TradeSports. Because NewsFutures was based on play money, it could also facilitate international betting, allowing users from different countries to trade with one another.

Policy Analysis Market: The largest-scale proposed public prediction market was the Policy Analysis Market, scoped in May 2001 by DARPA's Information Awareness Office as part of the FutureMAP project. Designed with the San Diego research firm Net Exchange, it would have let regional experts trade futures contracts on political, economic, and military developments across the Middle East. Though its designers intended for the predictions to be used as a geopolitical stability gauge, several US senators denounced it as a market for betting on assassinations and terrorism, and the Pentagon scrapped it in August 2003 before a single trade was placed.

PredictIt: Founded in November 2014, PredictIt offered real-money political betting to American traders as a nonprofit educational project of New Zealand's Victoria University of Wellington. Created by John Aristotle Phillips in partnership with the university, it operated under a CFTC no-action letter that allowed it to run without registering as a formal exchange, with an $850 ceiling per contract and a cap on how many traders each market could accommodate. Like the IEM, it positioned itself as a research tool and shared data with academics. As of July 2026, PredictIt is still in operation despite a multi-year legal battle after regulators moved to revoke its operating relief in 2022, the resolution of which raised its contract ceiling to $3.5K and removed the cap on traders per market.

Augur: Built on Ethereum in 2014, prediction market Augur was one of the first genuinely decentralized applications created on the blockchain. Funded by an ICO that raised roughly $5.5 million in 2015, Augur went live on Ethereum's mainnet in July 2018. Whereas earlier platforms curated their own contracts, Augur let any user create a market on any question, a permissionless design that drew controversy over user-created "assassination markets." The platform’s traction was limited from the outset, with daily users collapsing from about 270 at launch to under 30. The platform was relaunched in 2020 to migrate trades to the DAI stablecoin and add safeguards, but traction remained limited, and the project went largely dormant after 2021. As of July 2026, the Lituus Foundation and Ethereum contributor Micah Zoltu are leading a reboot of the platform, including a new protocol for dispute resolution.

Kalshi: Founded in 2018 by MIT graduates Tarek Mansour and Luana Lopes Lara, Kalshi has spent years and tens of millions in legal fees establishing that event contracts belong under commodities law rather than gambling statutes, and in November 2020, it became the first platform licensed by the CFTC as a designated market for such contracts. As of July 2026, Kalshi has millions of users and has been valued at over $20 billion. The platform provides probability data on global events to outlets like CNN and CNBC.

Polymarket: Launched in June 2020 by Shayne Coplan, Polymarket brought the blockchain model to the mass market, settling trades in the USDC stablecoin on the Polygon network. Polymarket claims to be the world’s largest prediction market, and has made waves with real-world marketing stunts, opening The Situation Room, a Washington, D.C. pop-up bar built for "monitoring the situation" with screens streaming live X feeds, flight radar, Bloomberg terminals, and Polymarket odds, after an earlier free grocery store pop-up called The Polymarket in New York City that gave away free groceries for several days. As of July 2026, Polymarket trading is now legal in some US states under the same CFTC governance as Kalshi.

In 2024, $3.6 billion was wagered on the US election Polymarket prediction market, which correctly signaled a Trump victory ahead of most pollsters and prompted the FBI to open a probe looking into the company as a facilitator of betting on election outcomes (which is illegal in over half of US states). Federal investigators dropped their probe in July 2025, shortly after which Polymarket acquired a CFTC-licensed exchange to secure a compliant path back into the United States, returning to American users at the end of 2025 alongside a multibillion-dollar investment from Intercontinental Exchange, the parent company of the New York Stock Exchange.

In addition to dedicated prediction market companies, established players across tech, crypto, finance, and sports betting have launched their own prediction market platforms in the last two years. Meta is reportedly building Arena (first reported in June 2026), a standalone, play-money prediction app personally directed by Mark Zuckerberg. Crypto exchange Crypto.com has been a CFTC-regulated prediction-markets pioneer since December 2024 and spun up its standalone prediction-markets platform, OG, in February 2026. Gemini, another crypto exchange, released US event contracts in December 2025 following CFTC approval. Traditional financial venues such as CME Group and Interactive Brokers opened their own CFTC-regulated prediction markets in 2022 and 2024, respectively. Finally, online sportsbook (OSB) operators opened prediction markets in late 2025, including DraftKings (December 2025), Underdog (September 2025), and PrizePicks (November 2025).

How Prediction Markets Make Money

Prediction markets make money in different ways, like charging a fee on each contract (regardless of whether the contract ends up a winner or not), taking a cut of winning payouts, or collecting the spread between bid and ask prices by acting as a market maker on its own platform.

Kalshi makes money in three primary ways. The first is per-contract trading fees charged on nearly every trade, to both the contract maker (seller) and the taker (buyer). Rather than a flat rate, the fee follows a probability-weighted curve: highest on 50/50 contracts near $0.50 and shrinking toward zero as a contract approaches $0.01 or $0.99, peaking at about $0.0175 per contract, with makers paying meaningfully less (often rounded to zero on small orders), and no fee when a contract settles. Second, Kalshi also earns interest on the idle cash sitting in customer accounts, which are held in segregated regulated accounts. Finally, Kalshi offers streams of market data via API and partnerships, allowing partners like Bloomberg, the Fed, and equity analysts to access its markets’ predictions off-the-shelf.

Unlike Kalshi, Polymarket historically subsidized trading fees (which were as low as 0% on most markets) using venture funding, betting that volume growth would allow it to capture fees later. In March 2026, the company began taking fees on contract buyers, determined by a multiplier that varies across categories, from 0.07 on crypto, 0.03 on sports, 0.04 on finance/politics, 0.05 on culture / other, while geopolitics and world events stay fee-free, and makers pay zero. As of July 2026, these fees are used to compensate market makers, and Polymarket’s primary revenue source comes from investing users’ USDC collateral, paying users about 4% and keeping the marginal interest.

Polymarket also makes money selling real-time data feeds to hedge funds, news outlets like Bloomberg, and AI developers. Longer term, a planned POLY token would allow the company to force users to hold their account’s cash in such tokens and make money by taking a cut of each transaction in addition to a cut of deposit interest.

Usage & Revenue

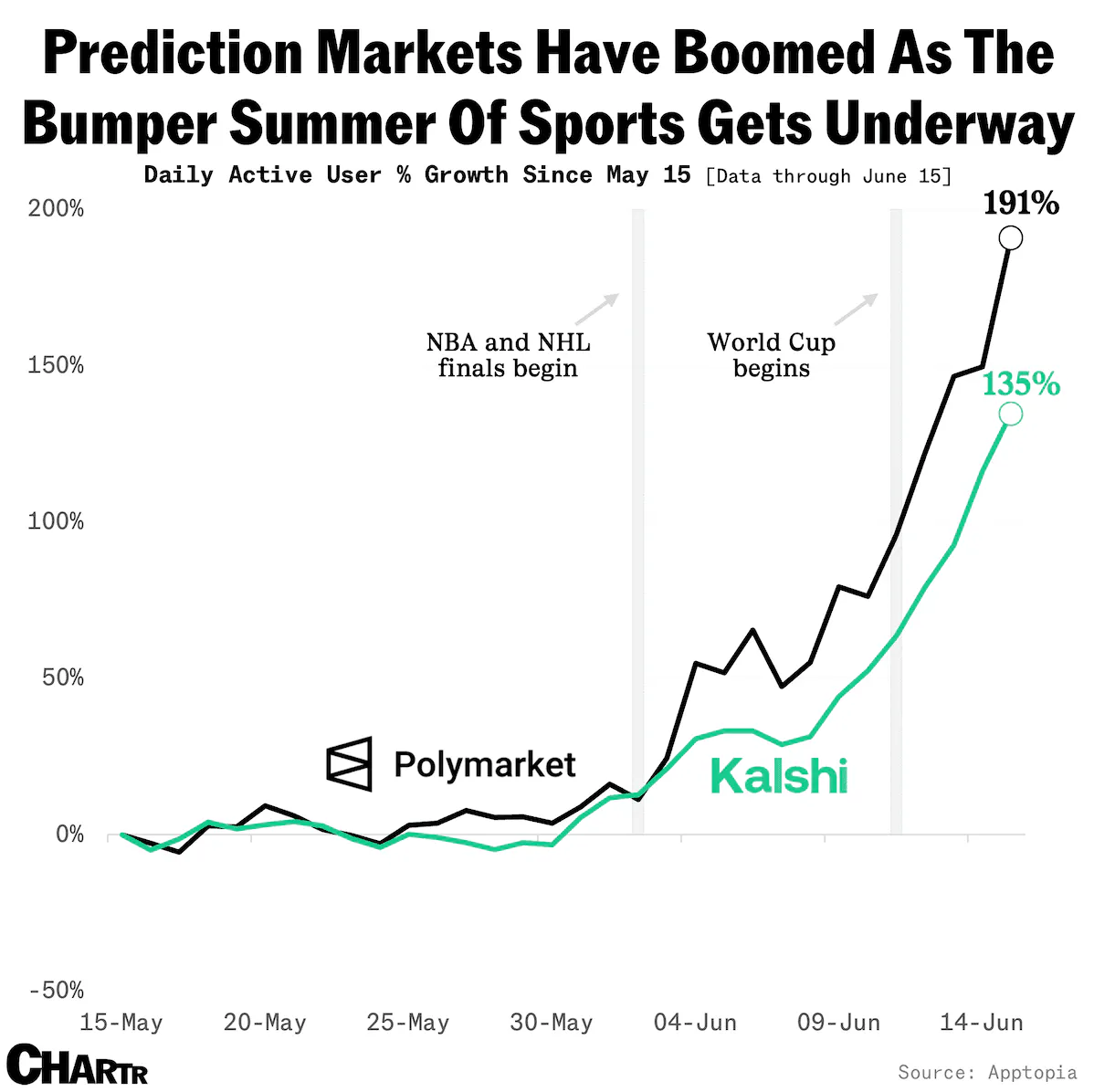

As of July 2026, Kalshi and Polymarket are the dominant prediction market platforms both in the US and globally. According to the companies, Kalshi has over 5 million active registered users, and Polymarket has 2.3 million, volumes that have more than doubled since May 15th, 2026, as NBA playoffs, NHL playoffs, and World Cup games have increased interest in wagering on sports event outcomes.

Source: Sherwood News

Analysts estimate that over 17 million individuals worldwide will use prediction markets in 2026, including prediction markets facilitated through traditional online sportsbooks. According to one study of prediction market users, 90% are male, a skew that prediction market advertisements are actively attempting to address.

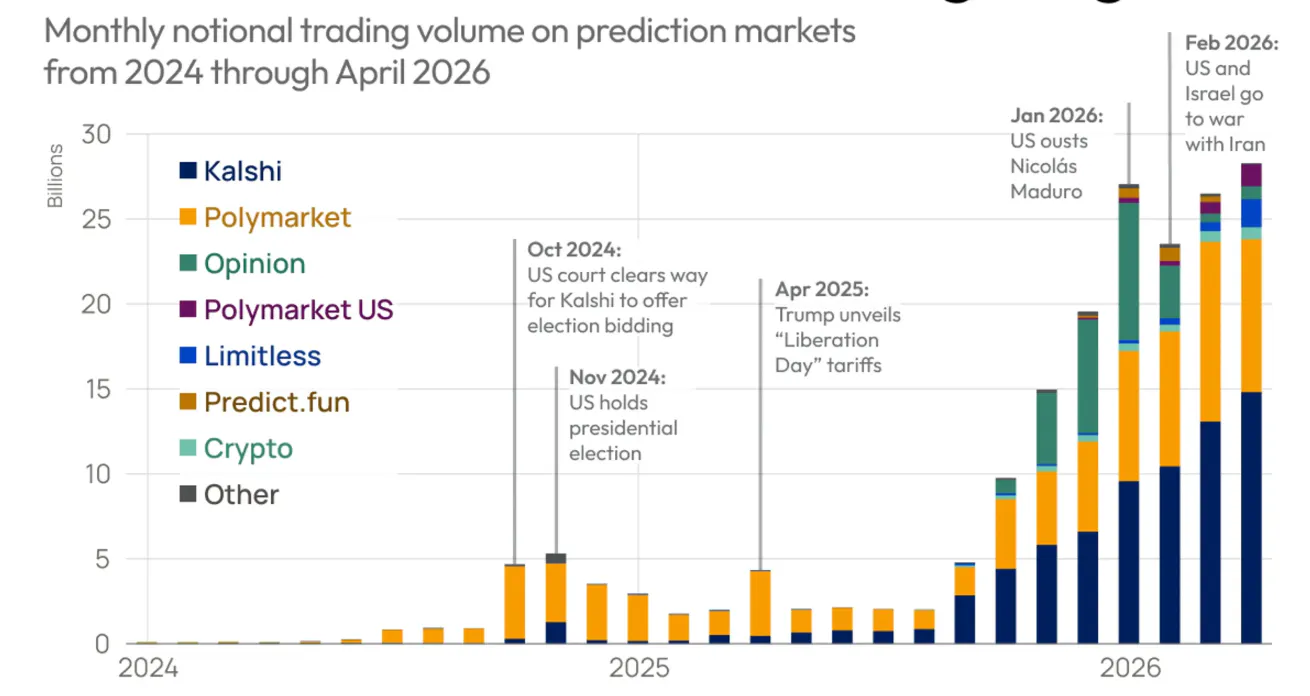

In line with a growing user population, prediction market trading volume has increased over 5x in the last year and over 10x in the last two years. Combined monthly global trading volume on Kalshi and Polymarket rose from less than $5 billion in September 2025 to $24 billion in April 2026. The global market was estimated at $31.2 billion as of May 2026. Kalshi reportedly makes up 58% of that volume, and Polymarket 28%. This global total is comparable to the handle of regulated US sports betting, which reached $167 billion during 2025, or around $14 billion a month.

"Handle" is the total amount of money wagered at a sportsbook. The sportsbook only keeps a small slice of that pool, called the hold (revenue as a percent of handle): in the US in 2025, the hold averaged about 10.15%, so books kept roughly $10 of every $100 wagered. This means $167 billion in handle translates to about $17 billion in revenue. Prediction markets keep a far thinner slice of their overall trading volume, since they charge small exchange-style fees instead of a 10% hold, which is why Kalshi and Polymarket can post comparable trading volume yet report much lower revenue (Kalshi's $2 billion ARR or Polymarket’s $1 billion ARR versus sportsbooks' $17 billion).

Comparing trading volume between Kalshi and Polymarket, and comparing either to sportsbooks’ handle, is not totally apples-to-apples. Kalshi tallies each contract at its full $1 face value, so a bet counts as $1 of "volume" even if the trader only puts down $0.40 to buy the contract. Polymarket instead counts the actual price paid (i.e., the 40 cents). A Columbia University study estimated that about 25% of Polymarket's past volume was "wash trading" (trades in which someone is essentially buying and selling with themselves to inflate activity numbers, not real betting, a behavior that was even more common in sports markets).

Source: GZERO Media

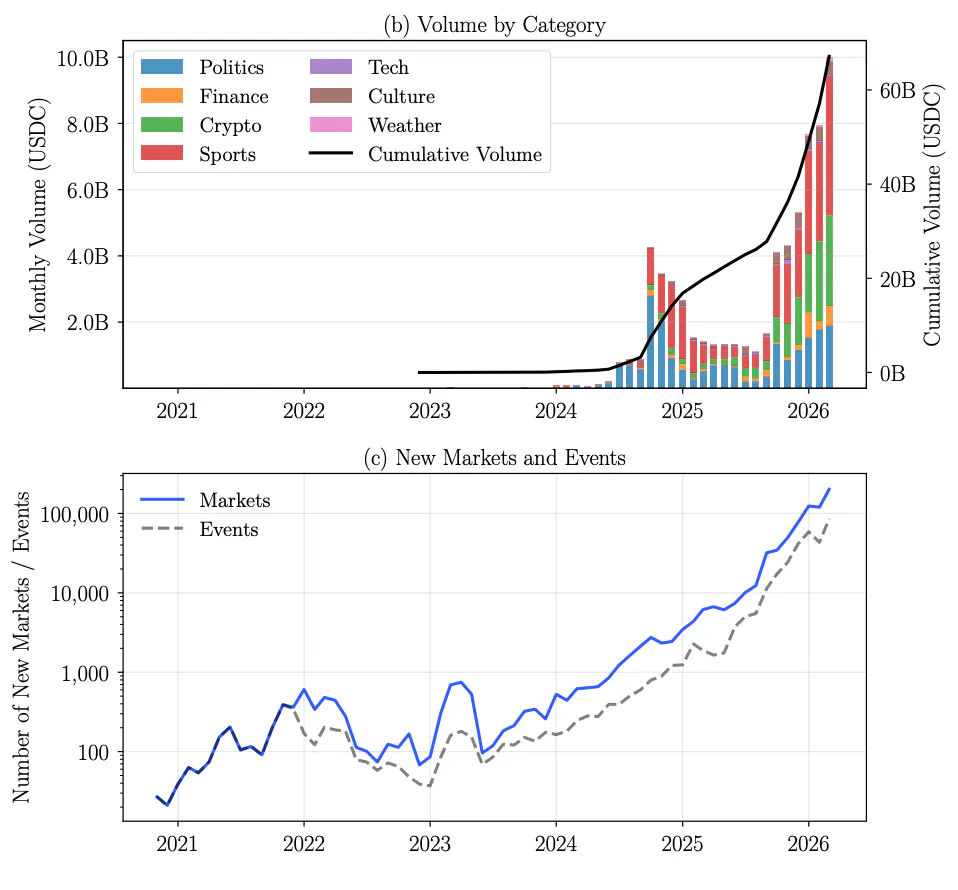

The category mix in prediction markets varies by platform, but sports contracts dominate trading volume in both the US and internationally. Sports contract trading reportedly makes up around 85% of Kalshi's notional volume and is the largest category at 39% on Polymarket. Parlays and “combos” reportedly also account for 20-25% of Kalshi's trading volume, but are almost exclusively combinations of sports events, bringing the sports share of trading on Kalshi closer to 100%.

Political events and election outcomes comprise roughly a third of Polymarket's volume, but only a small fraction of Kalshi's (elections made about $174 million on Kalshi in May 2026 versus $10.4 billion in sports, roughly 60x less). Crypto prices comprise about 18% of Polymarket’s trading; sports, politics, and crypto combined make up over 90% of volume on both platforms. Everything else is a small slice: weather and temperature markets account for less than 1% of Polymarket’s trading volume. Newer markets betting on private company performance metrics (increasingly popular as traders look for exposure to private companies before an IPO), prices of items like sneakers, Labubus, and Pokémon cards, and even keywords during speeches or corporate earnings calls are all a small share of totals.

Polymarket Trading Volume

Regulatory Challenges

Event Contracts, Futures, or Gambling?

The core legal question that will govern how prediction markets are ultimately regulated is whether the traded product is an event contract or a futures contract. As of July 2026, prediction market platforms are formally classified by the CFTC as Designated Contract Markets (DCMs), which are regulated trading platforms for exchanging event contracts as a form of swap. The CFTC has neither explicitly authorized prediction markets to operate nor asked companies to stop offering contracts as of July 2026.

A swap is a derivative in which two parties exchange payments based on the value of an underlying asset (a rate, a commodity, or the occurrence of an event) without owning the underlying asset itself. The Commodity Exchange Act defines a swap broadly to include any payment dependent on the occurrence, nonoccurrence, or extent of the occurrence of an event or contingency. The CFTC defines an event contract (also called a prediction or information contract) specifically as a derivative whose payoff is based on a specified event, occurrence, or value, which is typically structured as a form of swap.

Whether prediction markets should be regulated as event contracts has been widely discussed. One criticism is that contracts on prices, like the value of a pair of sneakers on a fixed future date, are not really "events," even though the contract expires on a set date. These critics point out that stacking yes / no markets at different price points (e.g., $100, $110, $120) amounts to little more than a poorly structured futures contract.

Source: Kalshi

Prediction markets centered on the future price of stocks or indices challenge this classification. A bet on the future value of a stock is classified as a "security-based swap," a security that is heavily regulated and that exchanges like Kalshi or Coinbase can't effectively offer to retail investors. The SEC has historically taken enforcement actions over illegal offerings of security-based swaps, which is why private company valuations aren't currently offered on prediction market platforms.

This classification remains contested: CFTC Chairman Michael Selig has repeatedly claimed that prediction markets and sports betting are “two separate things” while former CFTC chair Gary Gensler has argued sports bets aren't swaps, and are simply gambling instruments that should fall under state regulators, saying “Such contracts do not fit the CEA’s (Commodity Exchange Act) purpose or the statutory language defining swap, which focus on hedging economic risk. Sports bets are very rarely, if ever, about hedging.” Dan Berkovitz, another former CFTC chair, has opposed regulation of prediction markets as event contracts, saying, “The commodity markets are not for entertainment; they’re not to foster sports betting if there’s no economic purpose… they’re really for fundamental things that matter to the economy.”

Prediction markets themselves claim they are not gambling apps or sportsbooks, and instead consider themselves closed to financial markets. At the same time, platforms like Kalshi quote contracts in American odds and have run ad copy that includes lines like "bet on football legally" and "the first nationwide legal sports betting platform.” In May 2026, Kalshi became the first financial partner of the National Council on Problem Gambling, sponsoring a $2 million initiative on trader health and safety; the organization has been criticized as a pay-for-play membership system that does little to actually reduce harm through its policies and partnerships and in July 2026, the Michigan Gaming Control Board announced that it is withdrawing its membership from the council after its partnership with Kalshi.

Professional sports leagues like the NBA and MLB appear to support classifying the markets as gambling and have submitted letters to the CFTC voicing their concerns. The NBA said, “Without oversight and regulation tailored to the specific circumstances of sports wagering, the integrity risks posed by sports prediction markets are more significant and more difficult to manage than those presented by legal, regulated sports gambling.” The letter from the NFL asked prediction market operations not to offer trades on events that can be easily manipulated or determined in advance, like the words used by broadcasters, the draft of new players, or celebrities attending games

Cannibalization of Sports Betting

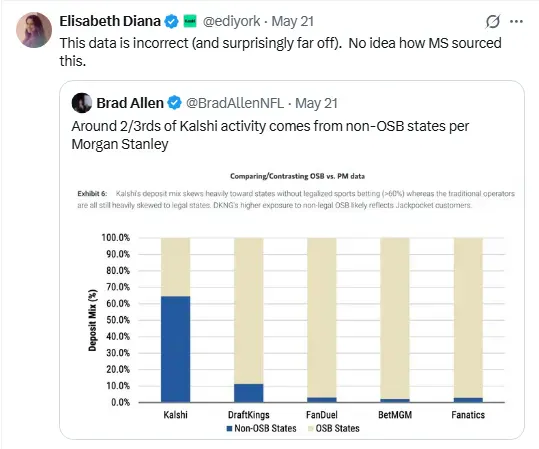

Early critics of prediction markets have argued that the popularity of sports-event contracts on these platforms threatens the existing online sportsbook (OSB) market share. Over time, however, data has shown that the opposite is true, with sportsbook market share nearly untouched in legalized-betting states, lending credence to the idea that sportsbooks provide an ultimately favorable user experience (in terms of outcome distribution) and business model for operators. Operators of OSBs, including DraftKings, MGM, Flutter/FanDuel, and Caesars, have all stated on earnings calls that cannibalization has been negligible, reporting no measurable decrease in handle in states where online sports betting is active and legal. It is worth noting that Kalshi has publicly disputed this fact without providing data to the contrary.

Source: Twitter

Prediction markets permitted in the US, such as Kalshi (and, only recently, Polymarket, for which US user data is not yet available), are legal in over 40 states as of July 2026. According to Morgan Stanley data, Kalshi is used predominantly in non-OSB states where sports betting alternatives are unavailable (compared to OSB platforms, which conduct the vast majority of their business in OSB-allowed states, as regulators intend).

Sportsbooks that also operate prediction markets (in addition to traditional odds markets) offer their sports prediction markets only in states where there is no sports gambling is not allowed (non-sports events contracts offered in all states). This is for two reasons. The first is that traditional odds-based betting is better for sportsbook bottom lines, allowing for higher margins in well-calibrated markets, where operators earn a cut between over- and under-lines on individual markets that far exceeds the cut that platforms can take on prediction markets.

The second and more important reason is that users prefer OSB betting to prediction markets for the same events and markets. OSBs can set odds based on how much they want users to win over time and calibrate betting lines to control the share of users who win and how much they win. This stands in contrast to prediction markets, where how much users win and how many users win is controlled by the players themselves.

If anything, the popularity of prediction markets has posed a potential benefit to sports betting markets, as states hesitate to raise taxes on the operations. “States are a little bit more hesitant to make a change that might inhibit their ability to be competitive against the federal product,” said Alan Ellingson, DraftKings CFO. Such a balance between federal- and state- taxed winnings will persist only if prediction markets are not ultimately regulated as gambling instruments.

State versus Federal Regulation

States, which see prediction markets as a form of gambling that should be regulated by state and tribal gaming control boards, have sued prediction markets from operating in their states without requisite approvals and taxes. As of July 2026, Kalshi has been sued by Massachusetts, Arizona, Michigan, Washington, New Mexico, and Wisconsin. The platform has itself sued New Jersey, Nevada, Montana, Maryland, Ohio, Connecticut, Tennessee, Minnesota, Iowa, Utah, and New York. Some of these states have already proposed their own taxation bills for prediction markets, predicting that prediction markets will ultimately fall under their jurisdiction. The AGA (American Gaming Association) tracks the tax revenue states are losing because prediction markets do not characterize sports contracts as betting. In July 2026, this estimate crossed $1 billion.

Part of the reason for this conviction is the sheer size of Gaming Control Board organizations relative to the CFTC, which has around 600 employees compared to the approximately 1K employed by each of the 48 states in regulating gambling activities (48K total vs 600), The Pennsylvania Gaming Control Board argued in a letter to the CFTX, “With all due respect to this body, it would take years for the CFTC to create the regulatory system and oversight that state gaming authorities have in place, and, were you to do that, it would create a redundancy to something that already exists and works exceptionally well.” Similar letters have been issued by other states.

Native American tribes, which regulate and profit from gambling on tribal lands, have also pushed for prediction markets to be regulated in the same manner as sports betting. In November 2025, tribes in California were denied the right to block access to Kalshi on tribal lands, a ruling that tribes have argued is a violation of the tribal-state compacts in place, giving tribes control over gambling activities on tribal land. As of July 2026, tribes in three states have sued Kalshi.

The CFTC, on the other hand, is still contending with whether prediction markets are a form of swap. The organization proposed the first set of official rules governing prediction markets in June 2026, which only placed regulations on contracts related to “War, Terrorism, Assassination, and Gaming.” And even those contracts can be permitted if they are not “against public interest” (all other contracts are default permitted). The agency has sued Arizona, Connecticut, Illinois, New York, Wisconsin, and Minnesota; all six states with a democratic attorney general. Though 16 states have sued prediction markets in total, the CFTC did not go after any of those with a Republican AG.

Prediction markets themselves prefer to be regulated by the CFTC, in the face of potentially lower taxes and less oversight. Kalshi co-founder and CEO Tarek Mansour has said “we're not necessarily very concerned” with state lawsuits against the platform, adding “The core of why… is we are regulated at the federal level…” and that “state law doesn't really apply” to the product. Some prediction market employees have also changed their views in line with the platforms. Sara Slane, the head of Corporate Development at Kalshi, said in 2018 that “states and sovereign tribal nations - not the federal government - are best positioned to regulate and oversee legal sports betting markets,” but now supports CFTC regulation of the products.

The Kalshi-commissioned poll from September 2025 reported that 79% of those surveyed (all Americans) believed event contracts should be regulated at the federal rather than state level. In May 2026, Kalshi backed the launch of Americans for Fair Markets (AFM), a "well-capitalized" advocacy group built to shape federal policy on prediction markets and push back against what Kalshi called a gaming-industry campaign of "seeding lies" to protect casino and sportsbook monopolies. AFM's policy agenda includes keeping prediction markets under exclusive CFTC federal oversight and backing consumer protections with identity verification and insider-trading bans. The group was announced several days after the House Oversight Committee opened an insider-trading probe into Kalshi and Polymarket, and launched opposite the gaming lobby's own new lobbying group, FairPredicts.

Profitability

Prediction markets have yet to turn meaningful profit, especially relative to their valuations, as they are not presently subject to gambling taxes and have used minimum-fee structures to bring in customers. Even beyond these factors, however, fundamental characteristics of prediction market structure make it difficult for these companies to profit from the same volume of players and betting activity as sportsbooks, and even more challenging to incentivize continued activity given limited liquidity and a deeply skewed distribution of winners.

Liquidity & Slippage

Liquidity is among the major differences between prediction markets and traditional financial markets, despite the comparisons drawn between them. DraftKings co-founder Matt Kalish has pointed out that the analogy to equities is significantly weakened by prediction markets' lack of liquidity. Because many markets are thin, it can be relatively cheap to meaningfully move the implied odds, so a buyer pushing size through a shallow order book faces significant slippage.

Source: Twitter

If prediction markets become regulated in the same way as sportsbooks, liquidity cannot be pooled across states, fragmenting depth that would otherwise concentrate; the 1961 Wire Act requires all bets to be offered within the boundaries of the state where the licensed sportsbook takes the bet. Compared to most sportsbooks, turnover is far lower in prediction markets, where long-dated markets lock up funds until resolution.

Lack of liquidity in prediction markets also reduces the extent to which the markets can be trusted to reflect the “wisdom of crowds.” In a thin market, a well-funded participant can purchase a large volume of shares to distort the price and create a false narrative about an event's likelihood. The empirical support for prediction-market accuracy comes largely from platforms like the Iowa Electronic Markets and PredictIt that imposed strict per-trader position limits (e.g., $3.5K on PredictIt), caps that newer venues have relaxed into the multi-million-dollar range.

Inefficient Pricing

In an October 2025 paper, NYU and Vanguard researchers documented that retail investors routinely overpay for binary options even when a strictly better alternative is available (as is the case for event contracts governing stock markets, cryptocurrencies, and other continuously traded assets). A binary option pays a fixed amount if some condition is met (i.e., $100 if an index closes above 1,000) and nothing otherwise. A bull spread (which can be assembled from multiple options) can be constructed to pay at least as much as the binary in every possible outcome, yet trades for less.

The paper provides a behavioral explanation for why traders still buy strictly sub-optimal binary options (which are constructed both via prediction markets and in other financial derivatives): people pay a premium for simplicity. Prediction markets effectively overcompensate for this premium with different tax treatment for the largest bets: under current prediction markets for a Kalshi contract on the S&P 500 finishing the year between 8,000 and 8,200, a $2,190 stake could pay out nearly $44,000. A user could instead buy the economically comparable 8,000/8,200 call spread in the options market, but the gains would be capped lower (around $20,000).

The Role of Market Makers

Because prediction markets need someone to quote both sides of each contract, Kalshi has built out a market-making layer that includes institutions like SIG and Jump Trading, individual liquidity providers, and an in-house desk, Kalshi Trading LLC. As Kalshi’s market maker program advertises, “In exchange for meeting defined quoting and volume requirements, market makers may receive reduced fees and certain adjusted position limits.

Kalshi’s in-house desk reportedly accounts for less than 6% of trading. And the company has said that it loses money. Analysts have speculated that this arm may be operating as a loss leader to seed liquidity, but even profit-maximizing market making in prediction markets is challenging. Unlike highly correlated financial markets in which market makers can hedge any open exposure in a related instrument, event contracts have no underlying spot market and often no correlated market to hedge with, so any inventory carried into resolution is fully exposed.

Distribution of Winners

Prediction market returns are extremely concentrated. On Kalshi, the top 0.1% of accounts capture 67% of profits; on Polymarket, the top 1% capture 76%. One April 2026 study attributed the accuracy of prediction markets in forecasting to these winners, with roughly 3% of Polymarket users driving price discovery in these markets. Those who consistently profit tend to be specialists who study particular markets, like speeches or earnings calls.

Prediction market ads have been found to misrepresent the retail experience in ways that invert the actual distribution of outcomes. One investigation found that Polymarket paid online creators several thousand dollars a month to stage winning bets on replica platform sites rather than the real exchanges. Of over 1K videos created, 70% showed a wager (none of which were real) and over 10% showed fabricated winnings, totaling nearly $900K; the same positions placed on the actual market would have lost more than $166,000. Because CFTC regulation bars deceptive marketing, the findings carry regulatory weight as Polymarket seeks to move its exchange onshore; the company said it would conduct a comprehensive audit of its promotional content.

This differs meaningfully from sportsbooks, which can set odds specifically to calibrate the share of bettors that win or lose. Peer-traded event contracts are zero-sum (net of fees), so skilled traders' gains come from others' losses. Retail participants are net losers relative to market makers on products like parlays, where they can only take contracts at odds market makers set rather than issue their own. This poses a fundamental challenge to the prediction market business model because retail traders who consistently lose are less likely to continue using the product, drying up liquidity for expert traders.

Prediction market platforms should be indifferent to any individual market's outcome because they earn fees on traded volume regardless. However, because most revenue comes from a few high-volume winners, platforms are incentivized to keep them. While sportsbooks limit scraping and automated trading, largely don’t offer API access, and cut off individual winners, prediction markets routinely offer API access for automated trading and rely on market mechanics to determine how much individual traders can win.

Insider Trading & Market Manipulation

Cases of insider trading on prediction markets have made the news in recent months, fueling public skepticism about the markets (such stories included a Google employee who made over $1.2 million on Polymarket, former congressman George Santos being accused of betting on his own State of the Union attendance, a US Army special forces soldier who made more than $400K betting on the capture of Maduro, and a man who manipulated a temperature detector at a French airport).

Insider betting, or using material nonpublic information to make bets, is more of a legal gray area than insider trading on the stock market. Some have argued that insider betting is a form of wire fraud (by analogy to insider trading as securities fraud), while others have defended the position that it is not (for the same reason that a firm may trade on its own proprietary information, but its employees can't front-run the firm's trades in their personal accounts). Insider trading on prediction markets is a similarly gray area; the CFTC has said commodities insider trading is illegal only where it involves “misappropriated confidential information in breach of a pre-existing duty of trust and confidence to the source,” not any use of material nonpublic information.

Kalshi and Polymarket explicitly ban insider trading. In June 2026, Kalshi announced security measures, including employment verification for betting on certain markets, as well as whistleblower features and risk scoring for higher-risk markets.

On X, investors and employees at both Kalshi and Polymarket have accused one another of enabling insider trading. Gambling and prediction markets analyst Steve Ruddock: “When the shots are coming from inside the house, one has to wonder what the future holds for prediction markets. We’ve seen this same self-defeating pattern play out repeatedly in sports-betting and online-casino legalization debates, where ‘allies’ push for broader legalization while lobbying for self-serving policies that inevitably fracture coalitions and ultimately derail broader legislation. I suspect the same will happen when the Commodity Futures Trading Commission (CFTC) starts laying out its prediction market rules.”

Source: Twitter

Wisdom of the Crowd

Comparison to Polling

Advocates of prediction markets tout their accuracy compared to polls as evidence of their merits as academic instruments. For example, Polymarket CEO Shayne Coplan told Anderson Cooper on 60 Minutes that prediction markets are the "most accurate thing we have," and the supporting record spans elections, macroeconomics, and corporate forecasting. Prediction markets have called election outcomes correctly even while contradicting the polls; a Fed / Northwestern / Johns Hopkins working paper found Kalshi to be at least as good as Wall Street analysts at forecasting Fed moves, inflation, and unemployment; and research on corporate prediction markets found employees betting real money beat experts on company forecasts, as seen in Google's internal markets Prophit and Gleangen.

In addition, prediction market data is increasingly being used for real-world applications, with platforms collecting API revenue for access. Institutional traders, including Goldman Sachs, reportedly use this data, and some oil traders have said that prediction-market forecasts of geopolitical events are driving the oil market, with "widespread" use in oil futures. The Intercontinental Exchange, which is the parent company of the NYSE, has launched a data-feed tool piping Polymarket probabilities to traders as "market signals." The potential usefulness of this data, however, is not separate from its potential as a tool for insider trading: “We’ve seen very large bets going on minutes before a major announcement comes up. The speculation is that someone on the inside has loaded up their crypto account to make some quick money on a bet,” one trader said.

Prediction market-derived odds also have limitations. Markets assign implausibly high odds to events like a UFO disclosure or the return of Christ, leading to a website tracking Nothing Ever Happens (betting against any events tracked on Polymarket occurring). Independent forecasters like Nate Silver have said they do not use prediction markets in their own predictive models, to avoid "pre-dilut[ing]" views and defeating the purpose of an independent perspective, and to avoid the risk of recursivity (if the markets are themselves shaped by Silver Bulletin forecasts).

Event Resolution Challenges

The “resolution” of prediction-market contracts refers to determining whether a "yes" or "no" position correctly describes the contract outcome. Resolution disputes pose a challenge for non-sports markets, for which contract wording and official data can be ambiguous. In the market concerning the potential removal of Venezuela's Maduro, for example, official state reporting directly contradicted credible independent journalism, compelling voters to arbitrate between competing accounts of events. Because event contracts are constrained by rules governing permissible outcomes, such as the prohibition on resolution by an individual's death, a Kalshi market on the removal of Iran's leader also generated substantial confusion as to which conditions would satisfy settlement.

On Polymarket, contested outcomes are adjudicated not by the platform itself but by holders of an independent cryptocurrency called UMA who vote to certify the result; in practice, however, the mechanism is considerably less decentralized than its design implies, as a majority of voting power is concentrated among only nine individual wallets, which have reportedly voted as a bloc in nearly every resolution. In response, a proposal gaining traction within the field would delegate resolution to large language models functioning as adjudicators, with the designated model and prompt inscribed onto the blockchain at the moment of a contract's creation, thereby fixing the settlement standard in a transparent and immutable form from inception.

Predicting the Future of Prediction Markets

The positive outlook for prediction markets as of July 2026 is likely peaking. On the dimensions that matter most, prediction markets appear poised to lose to sportsbooks: user experience, business model, and regulatory footing all favor incumbents. While sports contracts have offered an early foothold for prediction markets in non-OSB states, non-sports markets are more challenging to scale, hampered by thinner interest, longer resolution timelines, and persistent ambiguity over how contracts resolve.

Prediction markets have yet to generate meaningful revenue, particularly in light of their lofty valuations, even as they remain outside the gambling tax regimes that burden sportsbooks. Even if prediction markets increase fees and remain regulated by the CFTC, structural challenges will persist because peer-to-peer markets make it hard to monetize the same volume of players and betting activity that sportsbooks can, and harder still to sustain engagement when limited liquidity and a heavily skewed distribution of winners leave the average user with little reason to keep playing.