Thesis

Global mobile data traffic is expected to grow at a 23% CAGR from 2025 to 2030, driven by video, AI, 5G, and fixed wireless access. Yet the physical infrastructure layer is struggling to scale alongside demand. As a result, communications infrastructure is shifting from primarily terrestrial, fixed-network architectures toward increasingly software-defined, non-terrestrial, and multi-orbit systems.

Fiber deployment outside dense urban corridors remains prohibitively expensive, averaging $60K to $80K per mile, while traditional geostationary (GEO) satellites face unavoidable latency constraints due to orbital physics. GEO satellites orbit at roughly 36K kilometers above Earth, resulting in round-trip signal delays of approximately 500 milliseconds. In comparison, terrestrial fiber networks typically operate in the low single-digit milliseconds domestically, while even transatlantic fiber connections between New York and London maintain latency floors near 70 milliseconds. This makes GEO systems poorly suited for modern latency-sensitive, interactive workloads where latency thresholds are often below 20-50 milliseconds.

These infrastructure limitations are rapidly accelerating investment into non-terrestrial communications architectures designed for lower latency, higher throughput, and broader geographic coverage. Satellite operators, telecom providers, and defense agencies are increasingly deploying low Earth orbit (LEO) constellations, high-altitude platform systems, and multi-orbit networks that deliver faster, more adaptive connectivity than traditional terrestrial or geostationary systems.

The scale of this transition is already visible in deployment and capital flows. Active satellites have grown from roughly 1K in 2014 to nearly 10K by 2024, with more than 43K projected to be in orbit by 2032. Investment into LEO infrastructure has accelerated sharply, with global investment in LEO satellite systems reaching nearly $25 billion in 2024 and surpassing $45 billion in 2025. Meanwhile, the global LEO satellite market, valued at approximately $12.6 billion in 2024, is projected to grow to more than $41 billion by 2033, at a 14% CAGR.

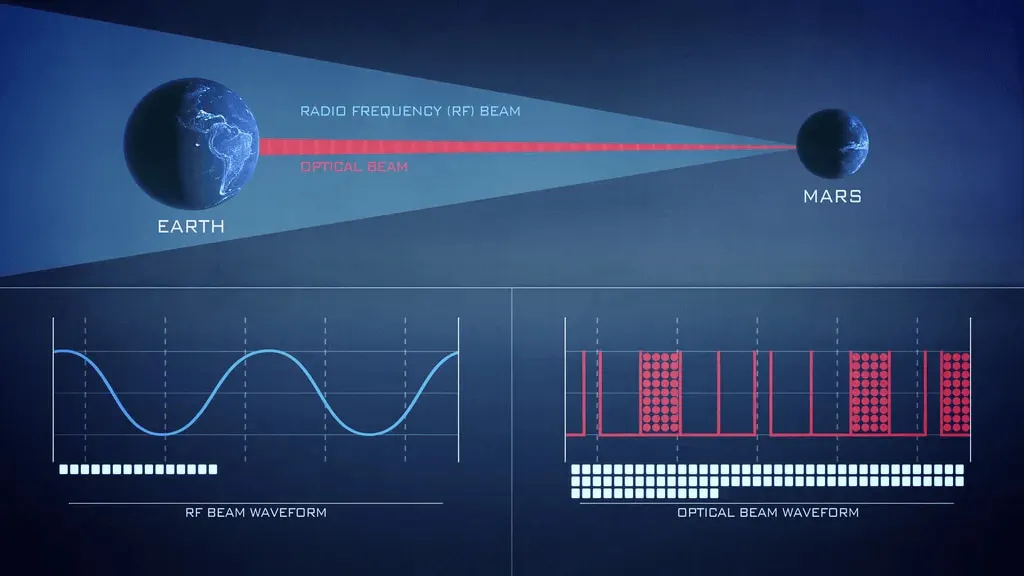

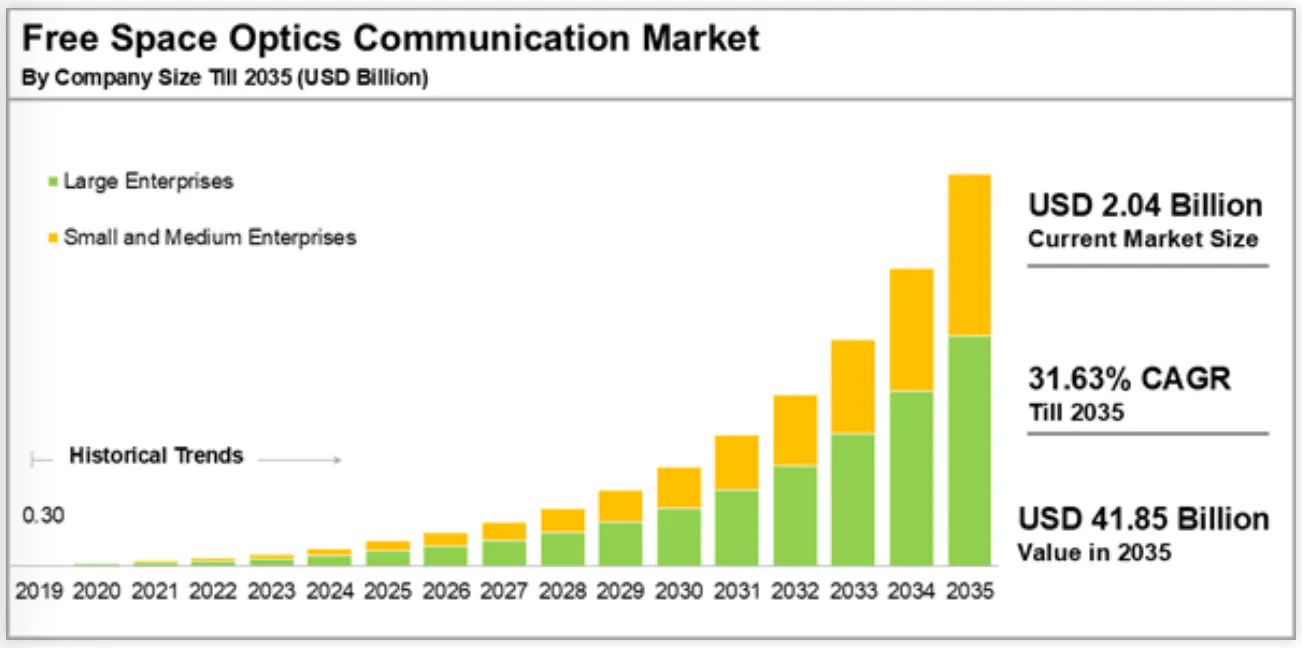

At the same time, the radio frequency (RF) spectrum, the traditional backbone of wireless communications, is becoming a binding constraint as constellation proliferation has congested RF bands, and projections suggest that spectrum shortages could leave networks unable to meet nearly a quarter of peak traffic demand in high-traffic areas by 2027. As a result, operators and defense agencies are increasingly shifting toward directional and optical communications, with the free-space optics market projected to grow from $2 billion in 2025 to $41.9 billion by 2035. Optical links are increasingly displacing RF for high-capacity, license-free, low-intercept data transport.

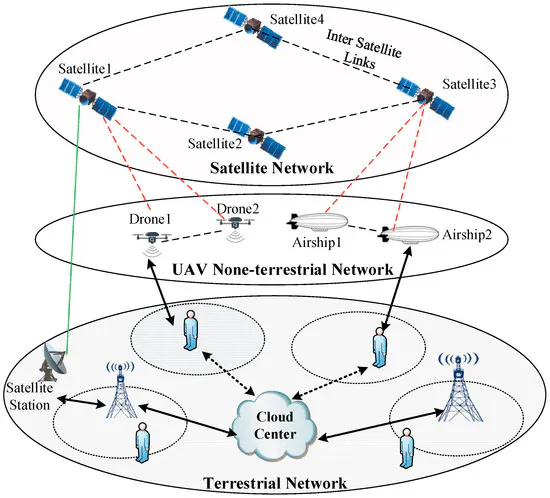

Unlike legacy terrestrial systems built around fixed infrastructure and stable routing paths, these networks feature constantly moving nodes, uneven demand patterns, and a continuously changing topology. The bottleneck is no longer simply deploying infrastructure, but coordinating it in real time across independently operated systems that were never designed to communicate with one another.

Aalyria is building the software and hardware communications infrastructure needed to coordinate the next generation of terrestrial, airborne, maritime, and space-based networks. Its Spacetime platform continuously optimizes routing, scheduling, and link allocation across various networks, while Tightbeam provides high-throughput optical connectivity engineered for secure, directional communications. As communications infrastructure becomes increasingly dynamic, heterogeneous, and optical, the orchestration layer that enables disparate networks to function as a unified system becomes increasingly valuable.

Founding Story

Aalyria was founded in 2021 by Chris Taylor (CEO), Dr. Brian Barritt (CTO), and Nathan Wolfe (Engineering Vice President and CTO) as a spinout from Google X, Google’s advanced research and development division.

In the 2010s, Google’s broader ambition was to expand global internet access and “connect the unconnected.” At the time, Google was already deeply embedded in the daily lives of billions of users. The company increasingly viewed internet access as both a long-term commercial opportunity and a foundational infrastructure problem, particularly in regions where terrestrial networks remained economically impractical to deploy. This belief drove a series of ambitious “moonshot” connectivity projects, most notably Project Loon, which aimed to provide internet access through high-altitude balloons operating in the stratosphere.

As these projects evolved, Google encountered a major technical problem: traditional communication networks had largely been designed around fixed infrastructure such as cell towers, fiber routes, and geostationary satellites, in which routing decisions could be made over relatively stable topologies. The challenge expanded further as Google pursued multiple connectivity initiatives simultaneously, including balloons, drones, and various satellite projects. Balloons drifted continuously, satellite positions changed dynamically, and airborne systems introduced constantly shifting network conditions. Existing networking systems struggled to coordinate traffic across moving assets whose connectivity, positioning, and environmental conditions changed in real time.

Initially, these systems were pursued as separate connectivity initiatives. Over time, however, the broader challenge shifted toward how heterogeneous airborne, terrestrial, and space-based networks could interoperate within a unified communications architecture.

To address this, Google engineers developed an internal routing and orchestration engine, Minkowski, designed to dynamically route traffic across continuously moving assets. Unlike traditional networking systems that optimized around relatively static infrastructure, Minkowski incorporated mobility and scalability directly into network decision-making. The system became the foundation for what would later evolve into Aalyria’s flagship software platform, Spacetime.

However, orchestration solved only part of the problem. As Google scaled these systems internally, another bottleneck emerged: transporting large volumes of data across distributed environments at “Google-scale” speeds. Traditional radio-frequency (RF) communication systems faced increasing spectrum congestion and bandwidth limitations, particularly as network density and data generation continued to grow.

To address this transport problem, Google turned to free-space optical (FSO) communications technology originally developed by researchers at Lawrence Livermore National Laboratory in the early 2000s. Unlike RF systems, FSO communication uses highly directional laser beams to transmit data through air and space, enabling faster communication over longer distances. Members of that research effort spun out into a company called Sierra Photonics, a company Google acquired around 2014 to support its broader connectivity initiatives, including Loon.

Internally, Google increasingly realized that intelligent orchestration alone would not be sufficient without a high-capacity transport layer. While what would become Spacetime could intelligently connect distributed assets, the system still required a scalable method for moving large volumes of data between them. This led to the parallel development of what would later become Aalyria’s Tightbeam optical communications platform.

Both Spacetime and Tightbeam were developed inside Google over roughly seven to eight years during the lifespan of Project Loon. When Google eventually began winding down several capital-intensive moonshot projects, including Loon, leadership decided to spin out the underlying technologies into an independent company.

Taylor became involved after learning the technologies might become available as Google scaled back the program. Prior to Aalyria, Taylor spent 14 years in the US Marine Corps as a Force Recon Marine, then moved into leadership roles in defense-focused technology and government services. His background included helping scale Mission Essential Personnel, an intelligence contractor, from approximately $185 million to nearly $730 million in revenue, founding veteran-focused startup Novitas, and later serving as CEO of Govini, a defense operations company, where he worked closely with Accel cofounder Arthur Patterson, who would later help facilitate Aalyria’s spinout from Google.

At the same time, Barritt had transitioned to Meta Connectivity following the wind-down of Loon, while many members of the original Google connectivity teams dispersed across organizations such as Amazon Kuiper, Meta, and other internal Google projects. Despite this dispersion, conviction around the underlying technology reportedly remained strong within the group. After learning that Taylor and Patterson were pursuing a spinout of the technology through venture backing, Barritt rejoined the effort as a co-founder. Several former members of the Loon and connectivity organizations who had also left rejoined their roles to reunite around the unfinished technical conviction.

Lastly, Wolfe, who leads the Tightbeam system, began his career in the U.S. Air Force as an air traffic controller before joining Google in 2016, where he became a Product Area Director and Technical Director leading advanced hardware efforts, including the development of optical communication systems that would evolve into Tightbeam.

Google formally spun out Aalyria in 2021, transferring intellectual property, patents, physical assets, and core systems. As a result, Aalyria launched with a decade of prior research, engineering development, and real-world deployment experience. The company also assembled a notable advisory group that included Vint Cerf, widely regarded as one of the fathers of the internet, as well as former Deputy Secretary of Defense Robert O. Work and former Space Force Chief Innovation Officer Major General Kim Crider.

Product

Product Philosophy

Aalyria is built around a fundamental reframing of what a network is. Traditional communications infrastructure, fiber routes, cell towers, and geostationary satellites assume the network is static and treat routing as the problem of finding the best path through a fixed topology.

Aalyria’s premise is that modern networks are not fixed, and LEO constellations, airborne platforms, maritime systems, and mobile terminals are becoming part of a single infrastructure that constantly changes position, coverage, and capacity. The question is no longer how to route data across a network, but how to continuously build and maintain the best network in real time.

To answer this question, Aalyria developed two core products: Spacetime and Tightbeam. Spacetime functions as the orchestration and decision-making layer of the network, while Tightbeam provides the high-capacity optical transport links that physically move data between nodes. Together, they form a software-defined communications architecture designed for highly dynamic environments.

Spacetime

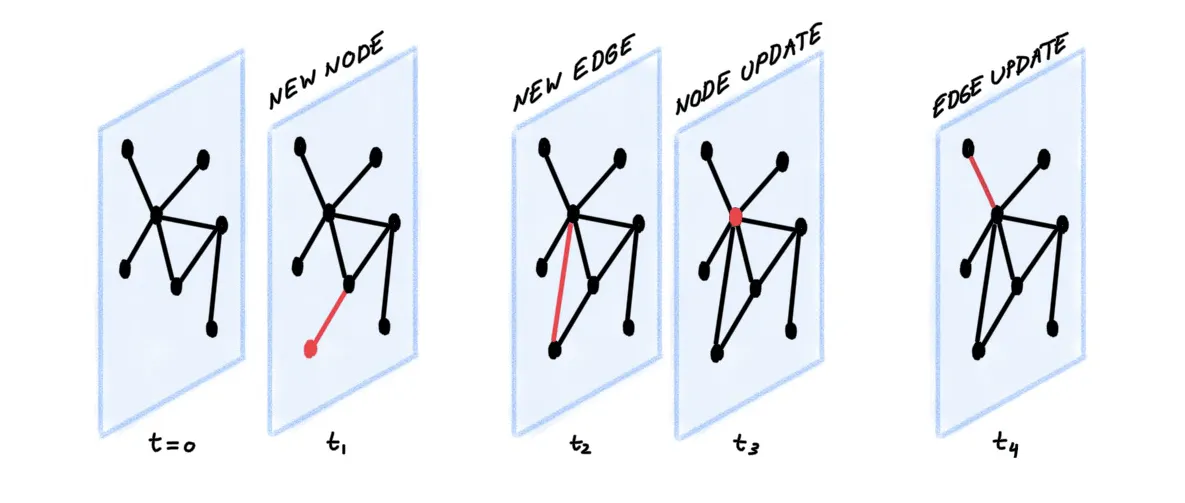

Spacetime is Aalyria's core software platform: a temporospatial software-defined networking (TS-SDN) system designed to orchestrate communications networks composed of moving assets.

In traditional networks, each router independently decides where to send traffic, with decisions distributed and reactive. Software-defined networking (SDN) improves on this by introducing a centralized controller with a full network view, enabling global optimization and dynamic reconfiguration. But traditional SDN still assumes the underlying topology is static and responds to failures only after they occur.

Temporospatial SDN incorporates time and physical space into every decision, accounting for nodes' positions, velocities, and orientations, their predicted motion, and real-time environmental conditions, including weather, interference, and occlusion. The result is a system that tries not to find the best route right now but instead maps out what the network will look like in the future, and how to prepare for it.

Spacetime represents the network as a time-evolving graph. Nodes are any networked terminal satellites, aircraft, ships, ground stations, or user devices; edges are not fixed links but potential connections, constrained by line-of-sight geometry, hardware capabilities, and environmental conditions.

Source: X Engineering

Spacetime continuously evaluates which of those potential connections should exist at any given moment and solves an optimization problem over how traffic should flow across them, simultaneously designing the network topology and routing traffic through it, rather than treating these as sequential steps.

Alongside this, it maintains a planetary-scale digital twin that continuously simulates all network assets, their motion, and their communications capabilities, fed by orbital mechanics data, flight paths, weather forecasts, terrain, and RF environment signals. This allows Spacetime to predict link performance before links exist, estimating latency, throughput, and signal quality to anticipate failures such as rain fade or physical occlusion and reroute traffic proactively rather than reactively.

Where traditional networking systems operate primarily at the routing layer, Spacetime operates simultaneously across the physical layer (establishing wireless and optical links), the link layer (configuring transceivers and interfaces), and the network layer (routing traffic). This cross-layer control enables sub-second reconfiguration timescales, critical in environments where topology changes faster than any reactive system can handle.

The critical use cases are precisely the environments where traditional networking breaks down: LEO constellations with thousands of fast-moving nodes and rapidly shifting topology; defense communications in contested environments with jamming and electronic warfare; airborne and maritime platforms with frequent occlusions; and hybrid non-terrestrial networking architectures integrating terrestrial 5G with space-based systems.

Tightbeam

Modern communication networks face a gap between data generation and data transport capacity. Satellite constellations, airborne platforms, and sensing systems generate enormous volumes of data, high-resolution imagery, real-time telemetry, and communications traffic, but the infrastructure used to move that data has not scaled at the same pace.

RF systems, which have historically carried that load, face constrained spectrum availability, lower peak bandwidth relative to optical systems, and increasing congestion as more assets come online. Fiber provides higher capacity but requires fixed physical infrastructure, making it impractical for dynamic, remote, or space-based environments. Tightbeam is Aalyria's solution to this transport problem, utilizing laser-based free-space optical (FSO) communications systems designed to provide high-throughput point-to-point links between satellites, aircraft, ships, and ground systems without requiring physical infrastructure.

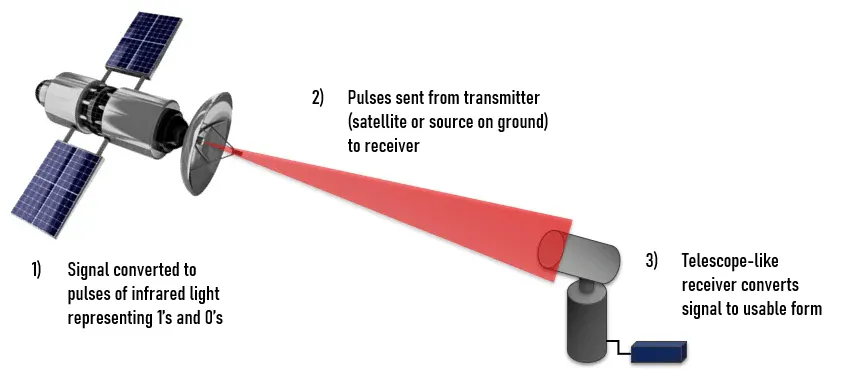

Free-space optical communication applies the principles of fiber optics to open-air or vacuum environments. Where fiber guides light through glass, FSO systems transmit light directly through air or space.

Source: Edmund Optics

This enables high-speed data transfer across links that would be impractical to serve with physical cable, inter-satellite links, airborne connectivity, ground-to-space connections, and communication in remote or infrastructure-limited regions. In satellite constellations where data generation frequently exceeds downlink capacity, FSO links can redistribute traffic through space or air rather than funneling everything through a limited number of ground stations.

The core tradeoff relative to RF is that optical systems offer substantially higher capacity through tightly focused beams, but require precise alignment and stable link conditions. RF propagates broadly and tolerates misalignment, but is spectrum-constrained. Tightbeam occupies the higher-performance, higher-complexity end of this spectrum; optical links are used where throughput and security matter more than flexibility.

Source: NASA

Most FSO systems use intensity modulation, where data is encoded in the light signal's amplitude. This is simpler to implement but more sensitive to atmospheric distortion, since turbulence and interference directly corrupt the signal's amplitude.

Tightbeam instead uses coherent optical communication, encoding data in the phase of the light wave rather than its amplitude. Coherent detection, the standard in high-performance fiber systems, provides higher spectral efficiency, improved receiver sensitivity, and greater resilience to certain atmospheric impairments because phase information is more recoverable than amplitude in degraded conditions. The tradeoff is significantly increased system complexity: tighter requirements for alignment, mechanical stability, and signal processing.

Tightbeam operates as follows: data is encoded onto a laser signal via phase modulation; a narrow optical beam is transmitted between two nodes; precision tracking systems continuously maintain alignment as platforms move; and a coherent receiver at the far end decodes the phase-modulated signal and reconstructs the data. The system's proprietary C.O.R.E. (Computational Optical Receive Engine) technology applies real-time adaptive correction to compensate for atmospheric turbulence, the primary reliability challenge for near-Earth FSO links.

Source: Aalyria via Tectonic Defense

Tightbeam is rated at 100-400 Gbps per link, depending on configuration, which means it significantly exceeds the bandwidth ceiling of typical RF satellite links and is directionally comparable to fiber in peak throughput.

In demonstrated deployments, the system has sustained 100 Gbps continuously across a 65-kilometer atmospheric link under real-world conditions, a speed-distance combination the company describes as previously unachieved in the atmosphere, and synonymous with streaming “4000 4k videos at once on top of Mount Everest.” Performance varies with link distance, atmospheric conditions, and platform stability, so rated figures reflect achievable performance under favorable conditions rather than guaranteed throughput across all deployments.

Market

Customer

Aalyria’s ideal customer consists primarily of government and defense agencies operating complex, multi-domain communications environments, as well as large commercial satellite operators building next-generation connectivity infrastructure. Government customers include organizations such as the United States Space Force, Defense Innovation Unit, and Air Force Research Laboratory, which increasingly require resilient, secure, and interoperable networking. Commercial customers include satellite operators such as Telesat and Intelsat, as well as telecommunications and aerospace firms building LEO, multi-orbit, and 5G non-terrestrial network (NTN) infrastructure.

Modern communications networks remain highly fragmented and operationally inefficient. Most satellite networks continue to operate through siloed, point-to-point architectures managed with proprietary software stacks, manual scheduling systems, and legacy tooling. Human operators still frequently coordinate routing, beam pointing, and satellite handoffs manually, while interoperability across vendors, constellations, or operational domains remains limited. Existing systems also create inefficiencies in bandwidth allocation, latency, power usage, and security, while broader efforts to unify communications across land, sea, air, and space domains have remained difficult for decades. Aalyria positions Spacetime as a software-defined orchestration layer intended to function as an “internet routing protocol” equivalent for space-based networking, dynamically coordinating connectivity across heterogeneous systems rather than relying on static operator-managed infrastructure.

The sales process can be difficult due to the nature of the customer base. Defense customers typically involve multi-year procurement cycles, requests for proposals, and various contracting vehicles, while commercial deployments are tied to long-term, capital-intensive infrastructure buildouts. Additionally, Aalyria is effectively selling a relatively new category of autonomous network orchestration software that requires significant customer education and integration effort. However, once integrated into operational communications infrastructure, switching costs are likely to become extremely high, creating the potential for long-duration contracts and deeply embedded customer relationships.

Although the overall customer base is relatively concentrated, with only a limited number of organizations globally operating satellite constellations or multi-domain military communications networks at scale, Aalyria has increasingly diversified across the public and private sectors and international geographies. As of 2026, Aalyria’s government relationships include the US Space Force, NASA, the European Space Agency, the Naval Research Laboratory, and the Defense Innovation Unit, while commercial and strategic partners include Airbus, Rivada Space Networks, Comtech, Keysight Technologies, Google Public Sector, ALL.SPACE, Logos Space, and LeoLabs.

Market Size

Aalyria operates across three overlapping markets: satellite network orchestration software through Spacetime, free-space optical communications hardware through Tightbeam, and the broader satellite and defense communications infrastructure sector. The company’s most direct market exposure comes from satellite network orchestration software, which represents the clearest near-term TAM for Spacetime. Adjacent exposure comes from the broader satellite communications (SATCOM) market and the emerging 5G Non-Terrestrial Network (NTN) segment, both of which are being targeted through partnerships with companies such as Keysight Technologies and Airbus.

The satellite orchestration software market was estimated at approximately $1.9 billion as of June 2026 and projected to grow to roughly $5.2 billion by 2033 at an estimated 11.8% CAGR. The broader SATCOM market is projected to expand from approximately $98.3 billion in 2025 to more than $223 billion by 2033, while the 5G NTN market is expected to grow from roughly $560 million in 2025 to approximately $2.8 billion by 2030.

Competition

Competitive Landscape

Aalyria’s competitive landscape spans multiple layers of the communications stack, including satellite operators, optical communications hardware providers, defense contractors, and emerging network orchestration platforms. The infrastructure layer is increasingly concentrated among vertically integrated operators such as SpaceX, Amazon, and Viasat, which control end-to-end systems spanning satellites, ground stations, and network software. These firms represent the largest source of scale and capital in the market, but generally operate through closed, proprietary architectures optimized for their own networks rather than interoperability with external systems.

At the same time, the broader market remains fragmented and in its early stages. Traditional defense and aerospace incumbents continue to dominate funding, procurement relationships, and large-scale deployment capabilities, while newer venture-backed entrants are driving much of the innovation in software-defined networking, free-space optical communications, and multi-domain network orchestration. Unlike more mature communications markets, the industry has not yet converged around a standardized networking stack or dominant coordination layer.

Vertically integrated operators primarily compete through ownership and scale of infrastructure assets, but also compete indirectly with Aalyria because their business models favor closed ecosystems over interoperable networking. Aalyria is differentiated by positioning itself as a neutral orchestration layer rather than an infrastructure provider. The company sits above the physical infrastructure layer, enabling interoperability across heterogeneous, multi-vendor networks without owning the underlying satellites or communications assets.

In this model, Aalyria’s software functions as a potential cross-network control plane for global communications infrastructure, coordinating connectivity across space, airborne, maritime, and terrestrial systems. Rather than competing directly with infrastructure providers on asset ownership, Aalyria’s objective is to become the orchestration and coordination layer through which increasingly heterogeneous communications networks operate.

Competitors

SpaceX Starlink: Founded in 2002, SpaceX operates Starlink, the world’s largest LEO broadband satellite constellation. Starlink represents one of Aalyria’s most significant indirect competitors because it controls the entire communications stack, including satellites, launch infrastructure, inter-satellite laser links, ground stations, and routing systems. While both companies focus on large-scale dynamic networking, Starlink’s architecture is entirely vertically integrated and optimized for its own ecosystem. Aalyria, by contrast, is infrastructure-agnostic and interoperability-focused. SpaceX competes by internalizing orchestration, effectively eliminating the need for external control layers within its network. Given Starlink’s scale, access to capital, and deployment velocity, it can also shape the standards for future satellite networking infrastructure.

Amazon Project Kuiper: Founded internally by Amazon in 2019, Project Kuiper is developing a constellation of approximately 3.2K satellites intended to deliver global broadband connectivity. Amazon has committed roughly $11 billion toward the initiative as part of its broader cloud and infrastructure strategy. Similar to Starlink, Kuiper competes indirectly with Aalyria by vertically integrating satellite communications infrastructure with cloud computing capabilities via AWS. While Aalyria positions itself as a standalone orchestration layer across heterogeneous systems, Amazon could integrate orchestration directly into its broader cloud ecosystem, turning connectivity and compute into a unified service offering. If orchestration increasingly becomes bundled within cloud infrastructure platforms, companies like Amazon could subsume parts of Aalyria’s role within larger vertically integrated ecosystems.

Lockheed Martin: Founded in 1995 through the merger of Lockheed Corporation and Martin Marietta, Lockheed Martin remains one of the largest aerospace and defense contractors globally, with a market cap of approximately $118 billion as of July 2026. The company competes with Aalyria across both orchestration software and optical communications.

On the software side, Lockheed has developed SpaceMesh Orchestrator, a platform designed to manage dynamic mesh communications networks across satellites and ground systems. Similar to Spacetime, the platform focuses on multi-domain coordination and resilient communications in highly dynamic environments. However, Lockheed’s strategy is fundamentally defense-first and tightly integrated into larger procurement programs, satellites, and military systems. Aalyria, by contrast, is building a hardware-agnostic orchestration platform capable of operating across both commercial and government networks.

Lockheed also competes with Aalyria through its investments in optical laser communications systems, such as Pony Express and GPS III-related optical technologies. Like Tightbeam, these systems focus on high-bandwidth, low-latency communication across air, ground, and space environments. The key distinction is that Lockheed’s optical capabilities are typically embedded within larger defense platforms and procurement contracts rather than offered as standalone modular networking infrastructure. As a result, Lockheed competes not only through its technology but also through its longstanding relationships with government customers, procurement channels, and integrated defense ecosystems.

Rivada Space Networks: Founded in 2022, Rivada Space Networks **is developing the “Outernet,” a global low Earth orbit (LEO) satellite constellation designed to provide secure, low-latency communications through laser inter-satellite links. Rivada shares similarities with Aalyria in its emphasis on dynamically routed, mesh-style communications architectures across space networks. However, the company approaches the problem from an infrastructure-first perspective by owning and operating its constellation, whereas Aalyria focuses on orchestration software that coordinates third-party systems.

Rivada therefore competes by embedding networking intelligence directly within vertically integrated infrastructure. If this model proves sufficient, it could reduce demand for independent orchestration layers such as Spacetime. At the same time, Rivada has also partnered with Aalyria, suggesting that the relationship may evolve toward collaboration rather than direct competition.

Mynaric: Founded in 2009, Mynaric develops laser communication terminals that enable high-speed optical links between satellites, aircraft, and ground systems. The company was acquired by Rocket Lab in a transaction valued at approximately $155.3 million in April 2026. Mynaric overlaps most directly with Aalyria’s Tightbeam product in the free-space optical communications layer.

However, Mynaric has historically focused primarily on hardware manufacturing, while Aalyria combines optical communications with orchestration software by integrating Tightbeam and Spacetime. Mynaric competes on the scalability, manufacturability, and performance of its optical communication terminals, whereas Aalyria’s broader differentiation depends on integrating transport hardware with dynamic network coordination. The Rocket Lab acquisition also highlights a broader trend toward vertically integrated optical communications stacks that could pressure standalone hardware providers over time.

Business Model

Aalyria operates a hybrid software-and-hardware business model in which software is the primary value driver, while hardware primarily serves as a deployment and ecosystem-enabling mechanism. Its core product, Spacetime, operates as a Platform-as-a-Service (PaaS) orchestration platform that enables customers to connect communications assets into the network, positioning Aalyria as a software-defined coordination layer for increasingly heterogeneous communications systems across space, air, maritime, and terrestrial domains.

Tightbeam consists of laser communication terminals designed to integrate directly with Spacetime as a plug-and-play access and distribution system. Rather than functioning as an independent hardware business, Tightbeam primarily expands the reach and utility of the broader “software-first” Spacetime ecosystem. Pricing is not publicly disclosed because the company primarily sells through deployment-specific enterprise and government contracts, where integration, security, and operational requirements vary significantly by customer.

The company’s highest costs are concentrated in specialized engineering talent, manufacturing, and government compliance. Laser communications hardware remains expensive due to radiation-hardened optics, precision tracking systems, and advanced mechanical components required for aerospace deployment, which cost three to five times as much as their ground counterparts. Furthermore, government work also introduces substantial compliance and certification costs tied to security clearances and defense contracting requirements, with audits and certifications for their multi-year Space Force indefinite-delivery, indefinite-quantity (IDIQ) contract ranging from $75K to $300K.

Despite these costs, Aalyria remains structurally more asset-light than traditional aerospace or satellite operators because it focuses on the network coordination layer rather than directly owning large communications constellations. This reflects a broader shift away from Google Loon’s asset-heavy infrastructure approach toward a more software-dominant economic model. Spacetime serves as the primary value-capture mechanism, while Tightbeam serves as enabling infrastructure. The business model ultimately centers on using hardware to seed and expand the ecosystem while monetizing through higher-margin, long-term recurring software revenue.

Traction

Aalyria has gained traction across both government and commercial markets through a growing set of defense contracts, satellite constellation agreements, and strategic industry partnerships. The company’s traction reflects increasing demand for networking infrastructure capable of coordinating communications across dynamic, multi-domain systems spanning space, air, maritime, and terrestrial environments.

Government Contracts

Aalyria’s early traction has been driven heavily by government and defense-related contracts. In 2023, the Office of Naval Research and the Naval Research Laboratory awarded Aalyria a $7 million contract for the first phase of the Navy’s Secure Optical Aerial Relay (SOAR) program, focused on developing over-the-horizon connectivity across naval sea, air, and land assets.

Building on this momentum, Aalyria expanded internationally in 2023 through a contract with the European Space Agency, funded by the UK Space Agency, to develop an orchestration system connecting space-based, airborne, maritime, and terrestrial nodes. In conjunction with the program, the company also established a London-based European headquarters.

In 2024, Aalyria secured one of its largest government awards through a $1 billion Indefinite-Delivery/Indefinite-Quantity (IDIQ) contract with the Space Rapid Capabilities Office to support dynamic satellite operations and end-to-end space mission ground systems. The contract further validated the need for software-defined network orchestration in modern military space operations.

That same year, NASA’s Space Communications and Navigation (SCaN) Program selected Aalyria for contracts focused on lunar communication infrastructure, including dual-purpose navigation and communications terminals and network orchestration systems that integrate services across multiple networks for the lunar and deep-space communications architecture.

Government traction continued into 2025, when the Defense Innovation Unit selected Aalyria for the ORIENT contract to advance resilient command-and-control networking for autonomous defense systems supporting the Replicator Initiative in countering mass weaponry by scaling autonomous systems across various domains.

In January 2026, the US Air Force Research Laboratory selected Aalyria for the Space Data Network Experimentation (SDNX) program through the STAR-FISH initiative to evaluate how Spacetime could integrate diverse satellite systems into a hybrid “network of networks” spanning government, allied, and commercial infrastructure.

Following this, in June 2026, NASA expanded its relationship with Aalyria through the Polylingual Experimental Terminal (PExT) program, selecting Spacetime for enterprise service operations within the agency's operational cloud environment. Under the program, Spacetime will provide network planning, scheduling, and resource management capabilities designed to coordinate communications services across government and commercial relay networks.

Commercial Customers

Alongside government adoption, Aalyria has established early commercial traction with satellite network operators seeking more dynamic and interoperable communications infrastructure. In 2023, Rivada Space Networks selected Aalyria’s Spacetime platform to orchestrate routing across Rivada’s planned constellation of 600 laser-connected low Earth orbit satellites. The agreement positioned Spacetime as a core networking layer within Rivada’s architecture.

That same year, Telesat signed a 10-year agreement to use Spacetime within its Lightspeed constellation to optimize real-time routing reliability across global communications networks. The long-term agreement provided additional validation of Aalyria’s orchestration platform within next-generation commercial satellite systems.

Strategic Partnerships

To expand deployment opportunities and integrate into broader communications ecosystems, Aalyria has also developed partnerships across defense, aerospace, satellite infrastructure, and network testing markets.

In 2023, Leidos partnered with Aalyria to integrate Spacetime with Leidos’ digital modernization capabilities to improve secure and resilient communications infrastructure for government and commercial customers. That same year, Anduril partnered with Aalyria to integrate Spacetime with Anduril’s Lattice operating system to support all-domain command-and-control capabilities and autonomous defense coordination.

Aalyria also partnered with ALL.SPACE in 2023 to combine ALL.SPACE’s multi-orbit SATCOM terminals, in conjunction with Spacetime’s orchestration platform, enable autonomous connectivity across multiple satellite constellations. In parallel, LeoLabs integrated its space-tracking and debris-monitoring data into the Spacetime platform to improve communication network resiliency and orbital awareness capabilities. The company also partnered with HICO Investment Group in 2023 to deploy Tightbeam’s optical wireless communication technology across maritime and underserved terrestrial markets, expanding the technology's potential commercial applications beyond defense and satellite networking.

In 2025, Keysight Technologies partnered with Aalyria to integrate Spacetime into benchmark testing environments for non-terrestrial network constellation design and validation, supporting development workflows for future satellite operators. In 2026, Airbus selected Aalyria for its SpaceRAN demonstrator program to test standardized global 5G non-terrestrial network connectivity, further positioning the company within the emerging convergence of satellite networking and terrestrial telecommunications infrastructure.

Valuation

In February 2026, Aalyria raised $100 million in Series B led by Battery Ventures, with participation from J2 Ventures and DYNE, valuing the company at $1.3 billion. Alphabet retains a minority stake from the original Google spinout, and Arthur Patterson, co-founder of Accel Partners, has been involved since inception.

Key Opportunities

Cross-Constellation Communication and Federated Networks

The US government's posture toward satellite communications is undergoing a fundamental architectural shift, away from siloed, single-vendor constellations and toward interoperable, multi-operator federated networks, with the Space Force seeking system-agnostic networking capabilities. This posture is driven by concrete national security imperatives, as both China and Russia have developed kinetic and non-kinetic counterspace capabilities targeting US satellites across all orbital regimes, making single-constellation dependence a recognized strategic liability. A truly resilient network architecture requires multiple suppliers, orbits, frequencies, and a distributed ground architecture, precisely the kind of heterogeneous, cross-vendor environment Spacetime is designed to orchestrate.

The commercial side of the market reinforces this dynamic. By default, satellite constellations from different operators cannot communicate with one another, and modern operational frameworks lack common standards for managing these heterogeneous infrastructures. As the number of active constellations grows, the cost of that interoperability gap compounds. More assets in orbit that cannot be jointly utilized means more stranded capacity and more coordination overhead. If the industry converges on federated architectures, as both government procurement and emerging standards suggest it will, control shifts from infrastructure owners to the orchestration software layer. Spacetime is positioned as the coordination layer through which increasingly heterogeneous networks are managed. In this scenario, Spacetime becomes a critical dependency across the entire communications stack rather than a niche product within any single one.

Free-Space Optical Communications

Aalyria is also positioned to benefit from the rapid growth of the free-space optical (FSO) communications market. Industry forecasts project the market could grow from approximately $2 billion in 2025 to roughly $41.9 billion by 2035, driven by increasing demand for high-bandwidth, secure communications infrastructure.

Source: Research and Markets

Much of this growth is tied to limitations within traditional RF systems. The RF spectrum is becoming increasingly congested, with projections that a spectrum shortfall could leave networks unable to meet nearly a quarter of peak traffic demand in high-traffic areas as early as 2027, while regulatory bodies such as the Federal Communications Commission continue to tighten spectrum allocations and licensing requirements. Simultaneously, modern satellite imaging, sensing, AI, and analytics workloads are generating significantly larger volumes of data than legacy RF systems were designed to support, volumes that RF cannot efficiently handle at the scale of next-generation constellations.

FSO sidesteps the spectrum problem. Unlike RF systems, FSO offers 10 to 100 times higher bandwidth, operates without a license, and provides a low probability of intercept, properties that are especially valuable for defense, intelligence, and enterprise customers with both performance and security requirements. Aalyria’s opportunity within this market is differentiated by the fact that the company is not only developing optical communications hardware through Tightbeam, but also integrating those optical links directly into a broader orchestration environment through Spacetime. As a result, the company’s value proposition extends beyond simply transmitting data faster; it also focuses on dynamically optimizing how data moves across complex, multi-domain networks.

Non-Terrestrial Networks (NTN) and 5G/6G Standardization

The standards bodies governing global telecommunications are actively pulling satellite networks into the same open, interoperable frameworks that have defined 5G. The O-RAN Alliance, including the European Space Agency, is developing open standards for space-based connectivity and aligning new satellite networks with 5G and 6G architectures. Telecommunications standardization has introduced non-terrestrial networking (NTN) capabilities for LEO satellites, including physical-layer adaptations and the ability to host radio access functions on board, marking the first formal integration of satellite infrastructure into the cellular standards stack.

As NTNs are operated independently, creating isolation, limited scalability, and high operational costs, open standards eliminate the viability of closed, proprietary architectures, making interoperability and programmability across vendors mandatory rather than optional. In that environment, nodes of future networks will rely on open-standard interfaces and be orchestrated by AI-driven network intelligence, and the control software layer, rather than the hardware layer, will become the primary source of durable value.

Aalyria is positioning Spacetime as the equivalent of a RAN Intelligent Controller, the network optimizer for radio, for space and non-terrestrial systems: the programmable decision layer that sits above the physical infrastructure, making real-time routing, prioritization, and coordination decisions across an increasingly open, multi-vendor network. If standards converge in this direction, Spacetime's architecture is well-positioned to become the default orchestration layer for a standards-defined, interoperable NTN ecosystem.

Key Risks

Adoption Risk within the Orchestration Layer

Spacetime only creates durable value if it achieves widespread adoption as an orchestration layer across heterogeneous networks. This is structurally difficult: communications infrastructure has historically favored vertically integrated, closed systems rather than shared control planes. Dominant operators like SpaceX Starlink and Amazon Kuiper have limited incentive to enable interoperability that would erode their competitive moat. Meanwhile, fragmentation in the satellite market is rising rather than resolving; the active satellite count has grown from roughly 1K in 2010 to over 9K as of 2026, increasing coordination complexity without guaranteeing the cross-operator cooperation on which Spacetime's value proposition depends. Failure to achieve adoption among major commercial operators risks confining Spacetime to a niche or government-only role, significantly constraining Aalyria's long-term revenue ceiling.

Feasibility of Free-Space Optical (FSO) Communication

While FSO communication offers higher bandwidth than RF meaningfully, it carries an inherent physical vulnerability: link reliability degrades under atmospheric turbulence and adverse weather conditions such as fog and rain. Tightbeam’s architecture addresses this through adaptive optics and predictive routing, but the 99.999% uptime standard across a globally distributed network remains unproven at scale. The core commercial risk is that, if reliability degrades under adverse conditions, customers may treat optical links as secondary or backup infrastructure rather than primary infrastructure, fundamentally limiting the addressable market and Tightbeam’s positioning as a core communications layer.

Capital Intensity and Execution Risk

Aalyria combines deep-tech hardware for optical communications with network orchestration software, which significantly increases execution complexity relative to pure-software businesses. Telecom and space infrastructure markets have historically required billions in capital and long deployment timelines to reach commercial viability, and the graveyard of technically credible systems that failed commercially is well documented.

Iridium spent $5 billion building and launching a 66-satellite constellation, filed for Chapter 11 in August 1999 after only nine months of commercial service, and at bankruptcy had accumulated just 10K subscribers against a forecast of 500K, a failure driven not by technical inadequacy but by a highly leveraged capital structure, long deployment cycles, and a competitive landscape that had shifted by the time the system was operational. Globalstar followed a nearly identical path, entering bankruptcy in 2002 despite building a functioning constellation.

Aalyria's operational model compounds this exposure through dependencies on specialized optical and aerospace supply chains, scarce high-end technical talent, and continued access to external capital. The primary risk is that delays, cost overruns, or a tightening funding environment interrupt Aalyria's path to scale before the company reaches the deployment density and customer breadth needed to establish a durable competitive position.

Summary

Data demand is outpacing the limits of terrestrial infrastructure, driving a shift toward LEO satellite constellations and non-terrestrial networks. As communications systems evolve from fixed infrastructure into dynamic networks of moving assets across space, air, and ground, the challenge becomes coordination at scale. Aalyria is positioned around this emerging control layer through Spacetime, its network orchestration platform, and Tightbeam, its optical communications hardware. The opportunity is large but still early, with adoption dependent on proving reliable optical connectivity, interoperability across networks, and scalable deployment economics.