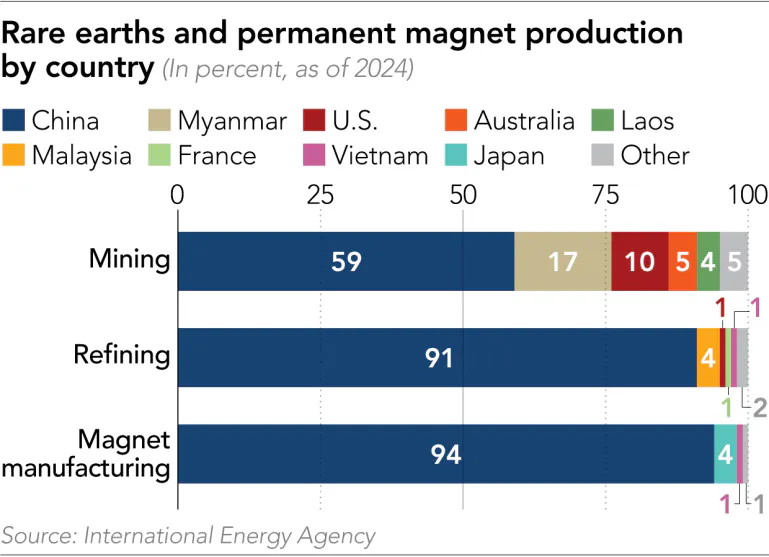

In 1992, former Chinese chairman Deng Xiaoping said, “The Middle East has oil, China has rare earths.” Today, China controls most of the rare earth supply chain, from mining to manufacturing. This has given it leverage over a crucial chokepoint of the global economy. As of 2025, China produced 70% of global rare earth mining output, compared to 13% from the US. Its dominance in processing and manufacturing is even more stark: in 2024, China accounted for 91% of global rare earth processing and 99% of heavy rare earth processing, while producing 94% of the world’s permanent magnets. Such magnets, and their rare earth components, are only increasing in importance as the global economy continues to electrify.

This creates a critical and escalating vulnerability for the global economy, and for the US in particular. In April 2025, China imposed export restrictions on seven rare earth elements and magnets in response to US tariffs, disrupting worldwide supply chains. These restrictions resulted in shortages of key materials critical to many modern defense, consumer, and energy technologies. US car manufacturers were forced to reduce magnet usage or temporarily shut down factories, while Western rare earth prices climbed to levels six times higher than domestic Chinese prices. These disruptions demonstrated the extent of China’s leverage over the global rare earth market, revealed vulnerabilities in the US rare earth supply chain, and reinforced the need to reduce reliance on Chinese production.

As a result, there is increasing urgency around rebuilding the rare earth supply chain outside of China. Achieving this formidable goal will require prioritizing the stages of the supply chain where China’s control is most concentrated: heavy rare earth production, rare earth processing capacity, and magnet manufacturing. This piece outlines why control of rare earth supply chain is so critical, how the current supply chain became so dominated by China, and how the US can rebuild a mine-to-magnet supply chain to reduce its dependence on Chinese rare earths.

Why Rare Earths Are So Important

Rare earth elements (REEs) or rare earths are a group of 17 metallic elements (15 lanthanides plus scandium and yttrium) that are critical for a wide range of modern technologies, from wind turbines to car motors to consumer electronics.

Their importance stems from unique magnetic properties that arise from their electron structure. Unlike electromagnets, they can generate and sustain powerful magnetic fields even in the presence of demagnetizing forces such as heat and competing magnetic fields. As a result, rare earths are used to shift missile trajectories, generate sound waves in headphones, pass signals through fiber-optic cables, capture neutrons in nuclear reactors, and even develop quantum computers.

They are also essential components in military defense systems: one F-35 jet alone contains over 900 pounds of REEs, while a Virginia-class submarine requires about 9.2K pounds as of July 2025. Rare earths also play a significant role in the AI supply chain through their use in semiconductor manufacturing, data centers, robots, and drones. Due to their importance in the energy transition and modern defense capabilities, all 17 rare earth elements are included on the United States’ 2022 list of 50 critical minerals considered essential to national security and economic stability.

Source: United States Geological Survey

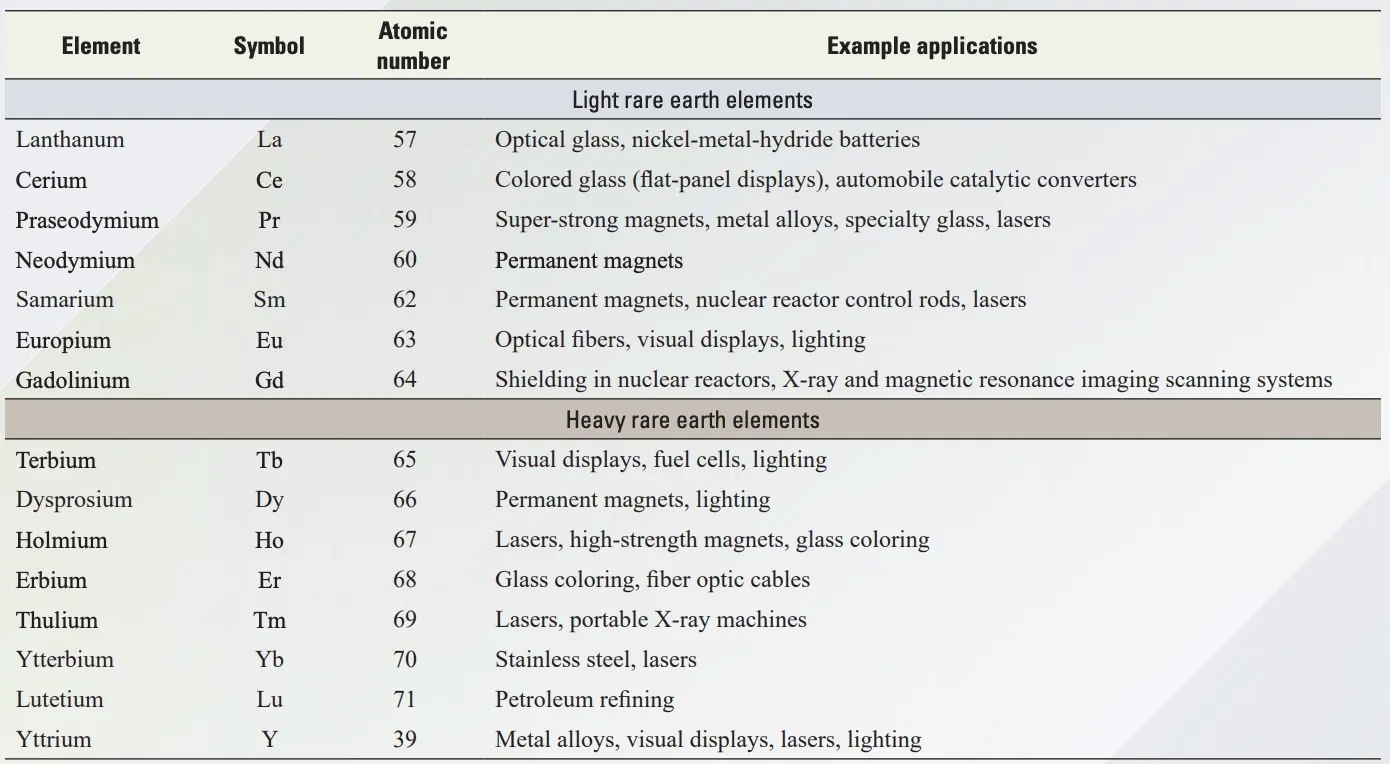

Globally, the leading use of rare earths is for permanent magnets, which are some of the world’s strongest and most reliable magnets. There are four rare earths that are most commonly used in these magnets: neodymium (Nd), praseodymium (Pr), dysprosium (Dy), and terbium (Tb). As of July 2025, these four rare earths accounted for about 30% of global rare earth volume but over 80% of total market value. This disproportionately high economic value is reflected in the pricing of those four rare earths: in 2025, terbium oxide had an average price of $810/kg, while cerium oxide had an average price of just $1/kg.

The reason these rare earths in particular command such a premium is that the permanent magnets that they are used to produce are essential for electric vehicles, industrial motors, data centers, and military defense systems, and thus represent one of the most economically and strategically significant uses of rare earths. Understanding the composition of these magnets requires distinguishing between different types of rare earth elements.

Rare earths are often divided into two categories based on atomic weight: light rare earth elements (LREEs) and heavy rare earths (HREEs). Both types of rare earth elements are used for permanent magnets; while light rare earths like neodymium and praseodymium make up a larger share of the material in these magnets, heavy rare earths like dysprosium are needed to keep magnets from weakening or being destroyed at high temperatures. In 2025, 95% of all electric vehicles used permanent magnet traction motors that contain NdFeB (neodymium-iron-boron) magnets, which are the most commonly used permanent magnets in the world.

Source: United States Geological Survey

Growth in electric vehicles and wind power has driven global demand for rare earths used in permanent magnets, which is expected to triple from 59 kilotons (kt) in 2022 to 176 kt in 2035. However, it is estimated that global rare earth production could fall short of global demand by about 30% in 2035, highlighting the growing need to increase future rare earth supply and production.

Despite their strategic importance, rare earth markets remain structurally opaque. Unlike traditional commodities such as copper or oil, rare earth elements are not traded on major exchanges and lack standardized pricing benchmarks. Instead, prices vary widely depending on the specific element, product form, purity, and delivery location, and are typically determined through bilateral negotiations rather than transparent market mechanisms. As of 2023, the majority of rare earth materials are sold through long-term contracts, and a small portion is traded on spot markets. As a result, rare earth pricing remains difficult to hedge or predict, leaving downstream industries more exposed to supply shocks. This opacity and volatility make it strategically important to control reliable sources of production.

Where Rare Earths Are Found

Despite their name, rare earths are relatively abundant in the Earth’s crust. In fact, rare earth elements can be found in very low concentrations in most massive rock formations. However, unlike most commercially mined metals, rare earths are rarely found in highly concentrated mineable deposits (known as ores) and are dispersed throughout rocks at extremely small levels. Even though rare earths are found on every continent, they are not always present in large enough concentrations to make mining worthwhile.

Source: REIA

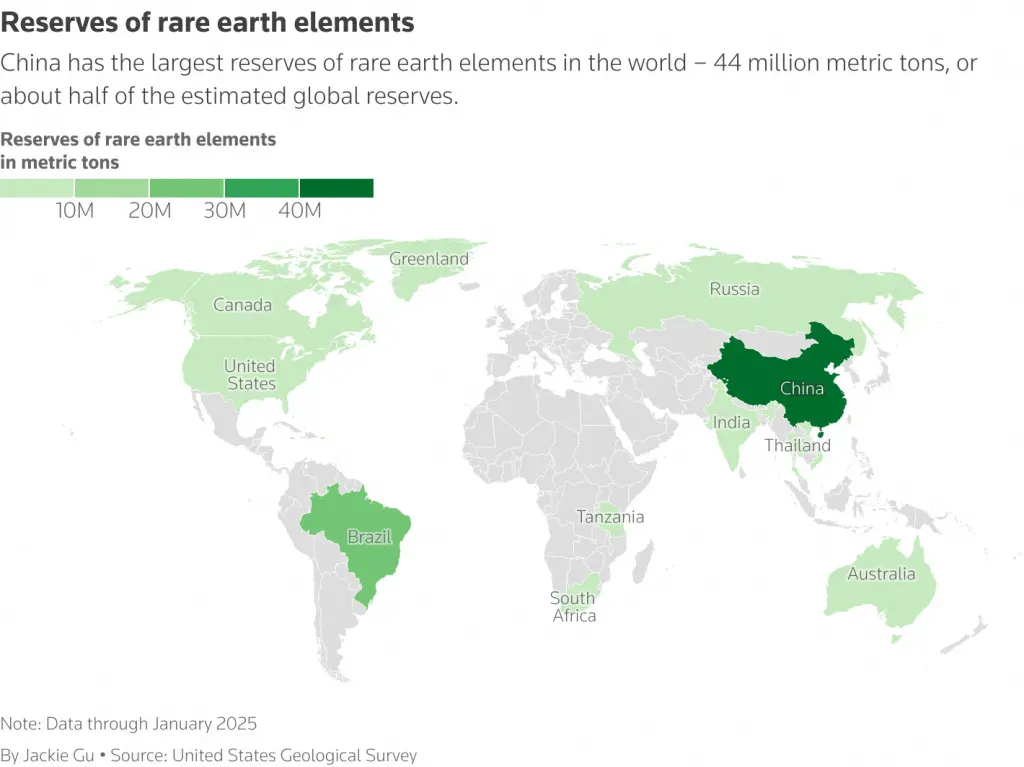

As of February 2026, China has the world’s largest reserves of rare earths at 44 million metric tons, which is about half of the estimated global reserves. However, new deposits continue to be identified worldwide as mining companies invest in geologically promising regions. In April 2025, a rare earth deposit said to be the third-largest on Earth was discovered in Kazakhstan with potential rare earth reserves of 20 million tons. Additional discoveries have also been made in regions with existing reserves: a new rare earth clay deposit was discovered in Utah in December 2025, and China announced the discovery of an additional 9.7 million tons of rare earth oxides in March 2026. Similar exploration activity is ongoing across Africa and other underexplored regions, where significant mineral wealth may lie undiscovered due to limited geological surveying and investment.

Despite this expanding resource base, translating deposit discoveries into production can be a slow and uncertain process. As of 2025, only one of every 100 mineral exploration projects leads to the development of a new mine, and it can take an average of 10 years for a mine to go from discovery to production. As a result, growing global reserves do not necessarily translate into increased rare earth supply because of the high complexity and time needed to bring new projects online.

The Challenges of Rare Earth Production

Finding rare earth reserves is only one part of the equation. The real challenge lies in extracting the rare earths from these reserves and transforming them into usable components for technology products.

The rare earth supply chain consists of three key stages:

Mining: extracting rare earth ore from REE deposits

Processing: separating the ore into rare earth oxides and refining those oxides into metals

Manufacturing: forming alloys from metals and transforming them into industrial components such as permanent magnets

Mining

Opening and sustaining a rare earth mine is inherently challenging due to the economic inefficiency of rare earth mining. Due to the naturally low concentration of rare earth elements in ore, rare earth metals typically make up only 0.5-6% of rare earth ores by weight, which is significantly lower than the 25-65% metal content of more common ores like aluminum or iron. As a result, large volumes of raw ore need to be mined in order to extract usable quantities of REEs.

Rare earths are typically extracted from minerals, which are naturally occurring inorganic solids that are made of chemical compounds (like quartz) or of a single element (like gold). Mineral deposits containing rare earth elements are found throughout the Earth’s crust, but they are only considered rare earth ores when REEs are present in high enough concentrations to be worth extracting in an economically viable manner.

Most rare earth mining has historically involved mining three different ore minerals that contain higher concentrations of REEs: monazite, bastnaesite, and ion-adsorption clays.

From the 1890s until the 1950s, monazite was the primary mineral mined for REEs, but it became less popular due to concerns about the high percentage of thorium, a radioactive material, in monazite and the environmental and logistical challenges of storing radioactive waste.

Starting around 1960, bastnaesite, which primarily contains light rare earths, became the dominant rare-earth-bearing mineral. It is found in China’s Bayan Obo mine, which is the world’s largest rare earth deposit as of October 2025, and is the primary product of the US’s only active rare earth mine in Mountain Pass, California.

In 1970, ion-adsorption clays, which contain an extremely high proportion of heavy rare earth elements, were discovered in southern China. Ion-adsorption clay deposits (IACDs) consist of rare earths that are loosely attached to the surface of clay minerals such as kaolinite and halloysite. About 80% of global HREEs were sourced from ion-adsorption clay deposits as of November 2025.

Traditional rare earth mining methods like open-pit mining and ion exchange leaching also generate large amounts of waste. Hard rock deposits like those of monazite and bastnaesite rely on open-pit mining, a method used to mine 70% of all minerals globally. Open-pit mining involves removing layers of soil and rock to reveal the underlying ore before drilling holes to fill with explosives to break apart the rock. Extracting rare earths from IACDs requires ion exchange leaching, a method that involves injecting a solution of water or ammonium salt into clay layers to trigger an ion exchange process that dislodges rare earths from clay particles. Both methods produce a large amount of toxic waste that can be harmful to both the environment and human health.

Processing

Processing rare earths is very expensive due to the difficulty of separating and purifying them. While there are many steps in this stage, the largest bottleneck and most difficult step is separating rare earth elements from one another.

Because rare earths share a similar atomic structure, they exhibit very similar physical and chemical properties that make it difficult to distinguish them from one another during separation. For this reason, refineries often use solvent extraction for commercial separation. In this process, rare earth elements are dissolved at different concentrations in two liquids that do not naturally mix (like oil and water). Acids that have affinities to different rare earth elements are then added, causing the rare earths to move from one liquid to the other. By repeating this process hundreds or thousands of times, the concentration of rare earth elements can be increased until a purity of 99% or greater is achieved.

Although solvent extraction is very effective at purifying rare earths, it is slow, energy-intensive, and extremely difficult to calibrate. Because every geological deposit contains a slightly different mix of rare earths, the separation process can be highly specific to the ore source. As a result, rare earth producers that have been processing the same deposits for a long time have a significant advantage because they have already optimized their separation process for the ore found in these deposits.

Manufacturing

The main challenge of magnet manufacturing lies in the high precision and resource availability needed to produce high-performance magnets. Because magnets are critical inputs for downstream industries such as electric vehicles and defense systems, they must meet strict standards for quality and reliability at scale. Producing permanent magnets such as neodymium-iron-boron (NdFeB) magnets involves carefully balancing the composition of component elements, as small variations can significantly affect magnetic strength, thermal stability, and durability. These magnets are typically produced through powder metallurgy and sintering, which are complex processes that depend on highly specialized expertise and equipment. As a result, manufacturing capacity is difficult to scale quickly without deep technical know-how and reliable access to upstream inputs.

China’s Supply Chain Dominance

Despite the many challenges of rare earth production, China dominates the entire supply chain of rare earths from mine to magnet as of April 2026, giving it massive leverage over global rare earth supply.

Mining: In 2025, China produced roughly 70% of global mining output, while the United States produced about 13%, almost all of which came from the US’s only active rare earth mine in Mountain Pass, California.

Processing: In 2024, China accounted for approximately 91% of global separation and refining capacity. Even though the United States is the world’s second-largest rare earths producer as of 2025, it has historically shipped most of its output to China for separation and refining up until 2024 due to a lack of domestic processing infrastructure. China has an even greater monopoly in heavy rare earth processing: as of April 2025, China accounted for about 99% of global HREE processing.

Manufacturing: In 2024, China produced 94% of the world’s permanent magnets.

While China accounts for a significant share of rare earth mining, its greatest control lies further downstream in processing and manufacturing. This gives China outsized leverage over the entire supply chain because even rare earths that are mined outside of China must pass through these later stages before they can be used in industrial applications. Unlike mining, which produces relatively undifferentiated commodities, downstream processing and magnet manufacturing transform these materials into specialized, high-value components that are essential for end-use industries and more difficult to replace.

How the US Lost the Rare Earths Race

China has not always been the dominant player in the rare earth space. In fact, the US was the world’s largest producer and refiner of rare earths throughout the 1970s and early 1980s. During this time, the United States operated the world’s largest rare earth mine in Mountain Pass, California. The arms race of the Cold War led to huge increases in government-funded rare earths research and the development of cutting-edge rare earth separation technologies, such as solvent extraction, which is still the most common way to commercially separate rare earths as of April 2026.

China’s rise was the result of a deliberate and long-term strategy to build technological and industrial capabilities across the entire rare earth supply chain. The development of China’s rare earths industry stemmed from China’s goal to develop its manufacturing and global trade capabilities with the aim of restoring political stability and domestic prosperity.

Starting in the 1960s, Chinese executives began touring the Mountain Pass mine, asking workers questions and taking pictures of production equipment and technology. After these executives brought this knowledge back to China, refineries improved their domestic rare earths technology, spawning hundreds of mining and processing firms across the country.

While the US and the Soviet Union had developed rare earth separation techniques using stainless steel vats and nitric acid during the 1950s and 1960s, Chinese engineers eventually developed a cheaper way to separate rare earths using inexpensive materials like plastic and hydrochloric acid, allowing them to produce rare earth oxides at lower costs than Western companies. By 1986, China had usurped America’s role as the world’s largest producer of rare earths.

However, the Chinese rare earth industry was still largely unregulated and chaotic at this time. Although the Chinese government set rare earth production and export quotas in the 1990s to reduce pollution and domestic price wars, up to 30% of China’s rare earth products in the mid-2000s were still illegally smuggled out of the country due to demand from Japan and the US.

Starting in 2011, the Chinese government cracked down on illegal mining operations and consolidated all domestic mining companies into the “Big Six” state-owned firms, allowing Beijing to control both supply and pricing in the global market. Recognizing the high value of downstream manufacturing, China strategically moved down the value chain, expanding from extraction and separation into magnet manufacture. In 1997, the US company Magnequench, a subsidiary of General Motors that patented and manufactured NdFeB permanent magnets, was acquired by Chinese investors. This acquisition allowed China to gain access to critical permanent magnet technology and accelerate the development of its domestic magnet industry, ending American and Japanese dominance in magnet manufacture.

While China was building out this vertically integrated ecosystem, the United States was moving in the opposite direction. Environmental regulations and rising compliance costs made rare earth mining and refining more expensive in the United States, and the industry gradually shifted to China. By the end of the 20th century, US investment in rare earth R&D had largely been deprioritized.

Compounding this, after the Cold War, the Department of Defense even sold off 99% of its national defense stockpile of rare earth materials as surplus, as it switched to just-in-time global sourcing. This stockpile had originally been created in 1939 in response to the US’s overreliance on foreign mineral imports leading up to World War II. In 2002, the Mountain Pass mine closed down due to delays in renewing its operating license and falling rare earth prices driven by Chinese oversupply; it would not open again until 2018 due to renewed interest in restoring the rare earth supply chain in the US.

China now controls most of the rare earth supply chain, from mining to manufacturing. This position did not emerge simply from its possession of the world’s largest rare earth deposits. Rather, it was the result of decades of coordinated policy, technological investment, and deliberate expansion into the highest-value stages of rare earth production.

Rebuilding an American Mine-to-Magnet Supply Chain

If the United States aims to meaningfully reduce its dependence on China for rare earth materials, it must begin rebuilding an independent mine-to-magnet supply chain outside of China. In 2024, the US government set a goal of creating a mine-to-magnet supply chain capable of meeting all US defense needs by 2027 and instituted a ban on the Department of Defense sourcing rare earths from China, Russia, Iran, or North Korea starting in 2027. Achieving this ambitious target will require prioritization of the most concentrated parts of the supply chain: heavy rare earth production, rare earth processing capacity, and magnet manufacturing.

Expanding Heavy Rare Earth Production

The first priority should be ramping up HREE production. HREEs play a critical role in Neodymium-Iron-Boron (NdFeB) permanent magnets, which were used in 95% of all electric vehicles in 2025. While light rare earth elements such as neodymium and praseodymium make up the larger part of these magnets, heavy rare earths such as dysprosium are required for their unique ability to retain magnetism at high temperatures.

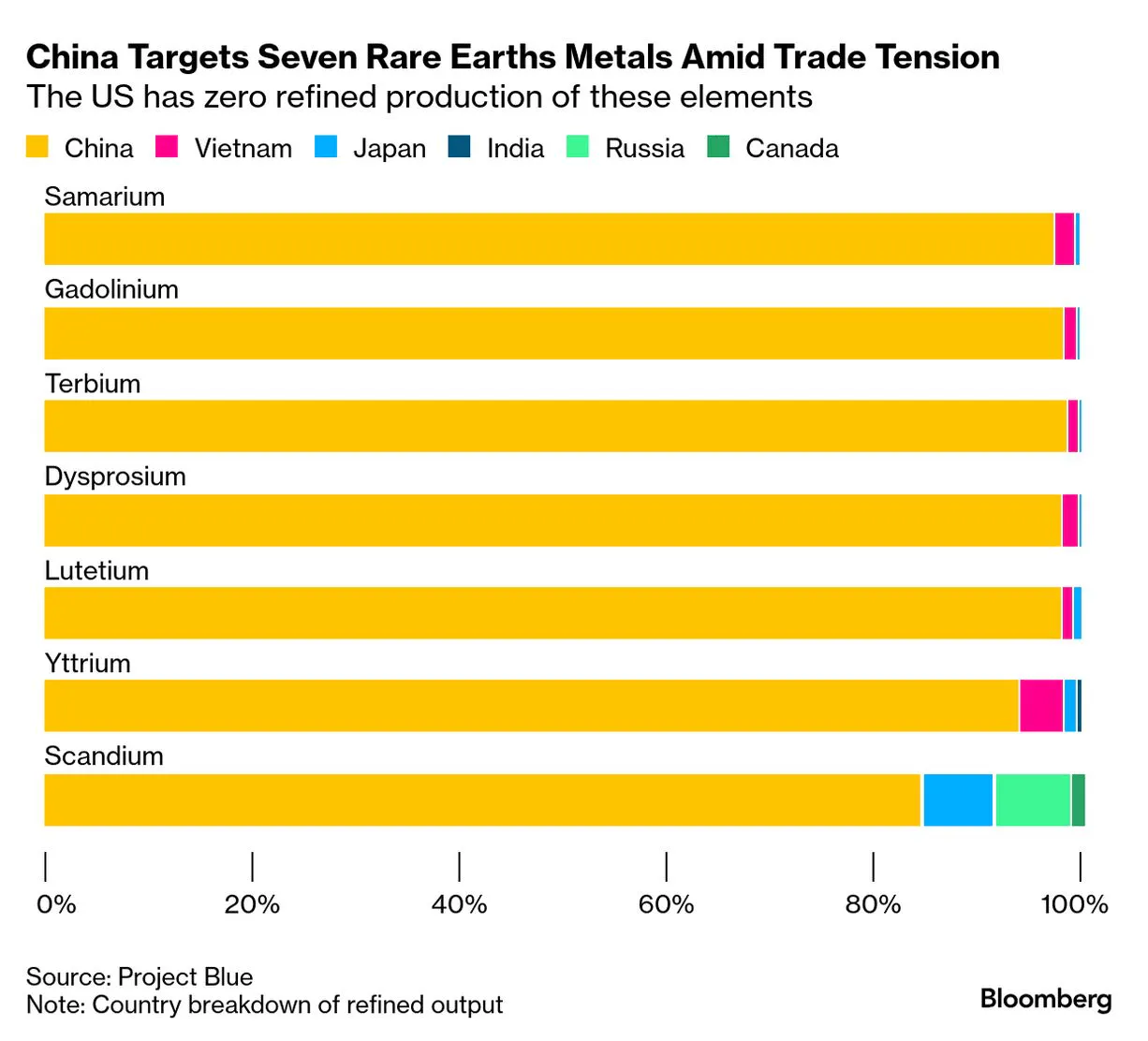

Despite their critical role in clean energy and defense system technologies, heavy rare earths are less abundant, more difficult to source, and thus more expensive than light rare earths. The global supply of heavy rare earths is highly concentrated. While light rare earths are found and processed by a geographically diverse set of countries, nearly all commercial deposits of HREEs are found in China and Myanmar. Myanmar alone accounted for about 45% of global HREE supply in 2024, yet most of that material is refined in China. As a result, China accounted for 99% of global HREE processing up until 2023, and the city of Wuxi, China, is home to the world’s only facility capable of refining dysprosium as of 2025.

This concentration creates a major vulnerability for the United States. As of April 2026, the country’s only active rare earth mine, Mountain Pass in California, primarily produces light rare earths, leaving the US with little to no domestic supply of heavy rare earths. As of April 2025, no commercial separation of heavy rare earths has been done in the United States. In order to truly build independence from China, the US will not only need an alternative supply of HREEs but also processing infrastructure that is sophisticated enough to refine these rare earths at scale outside of China.

Brazil’s Serra Verde project demonstrates the difficulty in building new production infrastructure and the importance of developing beyond the mining stage. Brazil has the world’s second-largest rare earth reserves but largely lacks the capital and expertise to extract them in an economically viable way. Brazil’s minerals licensing process also makes it difficult to develop its rare earths sector and takes an average of 16 years. Serra Verde is the country’s first large-scale rare earths producer and the only mine outside Asia currently producing both light and heavy rare earths. It finally opened in 2024 after 14 years of development. However, at the time of its opening, all of its output through at least 2027 had already been contracted to go to China because no one else in the world had the capacity to extract and separate these elements.

The story of Serra Verde clearly shows the necessity of building HREE processing capacity. The United States has begun taking steps to do so domestically, though progress is slow. In 2022, the Pentagon granted $35 million to MP Materials, the owner of Mountain Pass, to build an HREE processing facility, and in January 2025, USA Rare Earths produced its first sample of dysprosium oxide purified to 99.1%. However, because the United States lacks heavy rare earth deposits and processing infrastructure, collaboration with allied producers will likely remain necessary. In November 2025, the US government, MP Materials, and the Saudi Arabian Mining Company (Maaden) announced a joint venture to build a refinery at Saudi Arabia’s Jabal Sayid mine, which is estimated to have significant deposits of HREEs. In 2022, the Pentagon also granted $120 million to Australia’s mining company Lynas to build an HREE processing facility in Texas. In May 2025, Lynas made a significant breakthrough by becoming the first company outside of China to produce commercial quantities of dysprosium oxide in its Malaysian facility, demonstrating that heavy rare earth processing capacity can be developed outside China with sufficient investment and technical expertise.

Rebuilding Processing Capacity

The second priority should be rebuilding processing capacity because these midstream stages are where mining outputs actually turn into valuable industrial inputs. China has been successful in controlling the processing stages of rare earth production for two reasons: (1) they have a cost advantage due to state support and domestic demand, and (2) they have a technical advantage built over decades of sustained investment.

Source: Bloomberg, Project Blue

Rare earth processing is often less economically attractive than mining due to its high costs and low margins. As of 2023, separation and refining can make up to 50-75% of total operating costs in the mine-to-metal supply chain due to energy expenses and environmental regulations. China’s state subsidies allow Chinese processors to stay in business despite slim margins, but Western rare earth producers have increasingly focused on mining over processing due to its greater profitability. As of 2025, a new Western processing plant must contend with costs that are three to four times higher than those of its Chinese counterparts, largely due to China’s decades of investment in infrastructure, labor, and state capital. Additionally, China is the world's largest consumer of rare earths, meaning that its domestic electric vehicle and wind turbine industries can generate enough demand for processing output to keep Chinese processors in business.

The US will need government support and financial tooling to compete with China’s cost advantage in processing. Without long-term demand commitments and price support, onshore processing projects may never reach durable commercial scale. The Department of Defense’s 10-year agreement with MP Materials is exactly the kind of support that is needed for nascent projects. The deal provides funding for a new domestic magnet manufacturing facility known as the “10X Facility,” establishes a price floor of $110/kg for MP Materials’ output of NdPr oxide, and ensures that 100% of magnets produced will be purchased. Given that it has historically taken an average of 29 years to develop a new mining project in the US and another 7-10 years to license a new refining facility, this kind of risk-sharing strategy is crucial for the long-term survival of domestic rare earth production facilities.

Rebuilding processing capacity also requires rebuilding technical knowledge. China has spent decades building a workforce, process expertise, and intellectual property base that the US no longer has. China also has more trained technicians and researchers for rare earths than any other country in the world. As of January 2026, it offers rare earth programs at 39 of its universities; meanwhile, none are offered in the US or Europe. Even though the rare earth refinement process originated in the US, Chinese engineers were the ones who actually perfected the solvent extraction process. China has also filed over 25K rare earth patents from 1950 to 2018, compared to 10K rare earth patents in the US.

The US government must not only subsidize the development of new facilities but also the human capital and technical ecosystem behind them. In August 2025, the US Department of Energy announced its plans to launch a “Critical Minerals and Materials Accelerator” to develop new processing technologies for critical minerals like rare earths. This is an important first step, but it will take significant investment to recover the capabilities that China has been refining for decades.

Scaling Magnet Manufacturing

The third priority should be reviving magnet manufacturing. Even after rare earths are mined, separated, and refined, they become most valuable economically when they are incorporated into industrial components. The leading use of rare earths is for permanent magnets, which are critical for electric motors, consumer electronics, data centers, and defense systems.

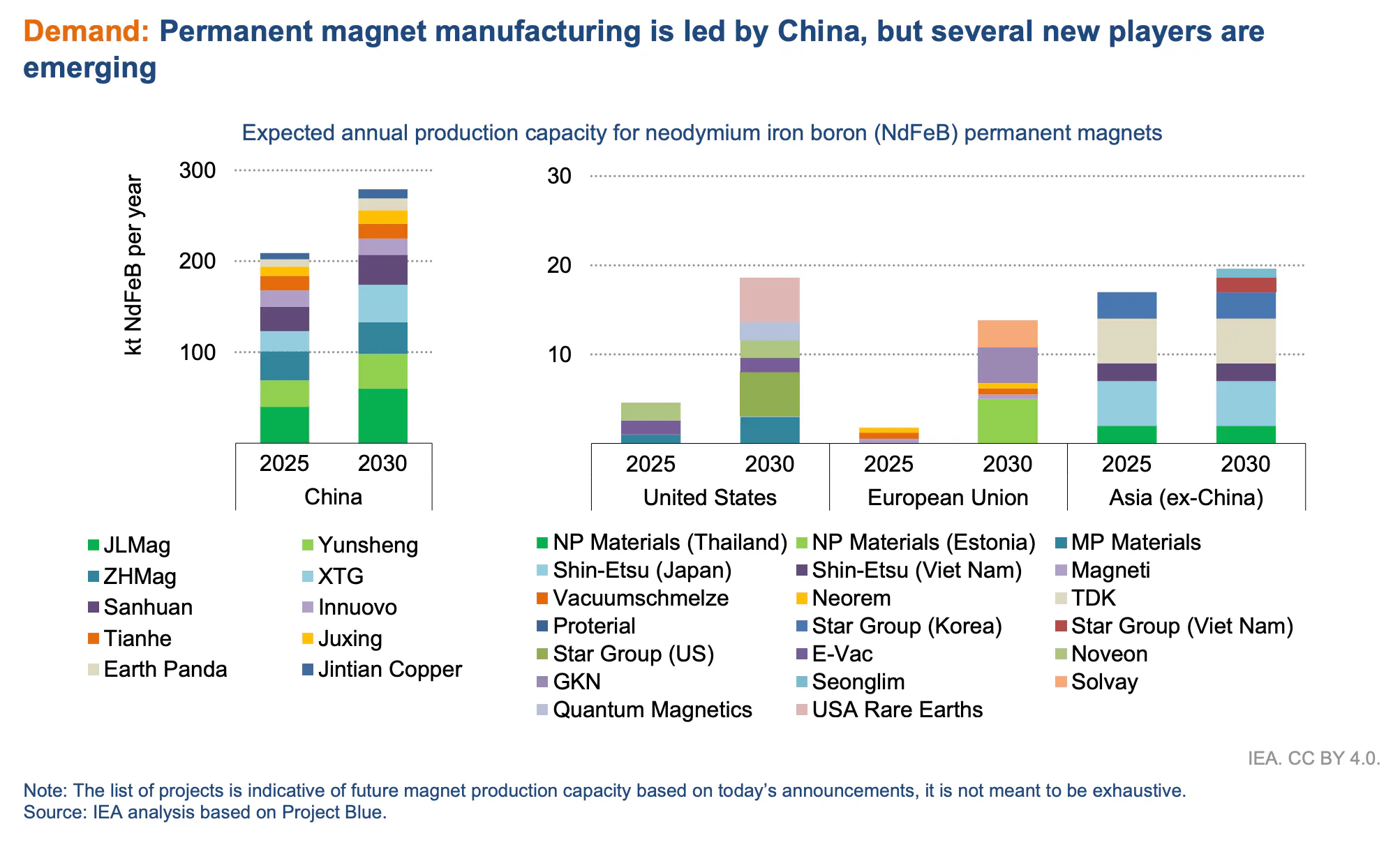

Source: International Energy Agency

In 2024, China manufactured 94% of the world’s rare-earth permanent magnets. This high concentration leaves global supply chains in critical sectors such as energy, defense, and AI data centers highly vulnerable to potential disruptions. This kind of disruption already happened in April 2025 when China imposed export controls on its exports of rare earth metals and magnets in response to Trump’s tariffs, resulting in magnet shortages and manufacturing interruptions. After adding more export controls in October 2025, China later reached an agreement with the US to suspend rare earth export controls for one year in exchange for US trade concessions, including the withdrawal of a US national security measure that restricted Chinese access to advanced technology. China’s dominance in magnet production comes with great negotiating power against the US, demonstrating the importance and urgency of diversifying sources of magnet manufacturing.

The US has begun building onshore magnet manufacturing facilities as well as domestic demand for American-made magnets. MP Materials first began producing magnets in 2025 and received additional funding from the Department of Defense later that year to build a second magnet manufacturing plant in Texas. In July 2025, Apple entered into a $500 million deal with MP Materials to produce magnets for its iPhones, indicating a willingness for US OEMs (original equipment manufacturers) to switch to American-made magnets as uncertainty around Chinese export controls continues to rise. However, as of October 2025, planned global capacity for permanent magnet manufacturing outside China remains much lower than for mining and refining, reflecting the difficulty of building downstream infrastructure in the rare earth supply chain.

Building a Secondary REE Supply

Even if the United States focuses on the right bottlenecks, rebuilding a non-China mine-to-magnet ecosystem will take time. In 2024, MP Materials produced 1.3K tons of neodymium-praseodymium (NdPr) oxide and only began trial production of NdFeB magnets, while China produced over 95K tons of NdPr oxide and 300K tons of NdFeB magnets in the same year. It will take a long time for the US to close this gap, given the long time horizon to develop and ramp up new mining or refining facilities. Recycling and stockpiling can reduce price and supply vulnerability in the meantime, but they should be viewed as supplementary strategies rather than substitutes for rebuilding the US rare earth stockpile.

Stockpiling

After the Cold War, the US Department of Defense had a large strategic stockpile of $42 billion worth of critical minerals and rare earths; as of early 2023, that stockpile had fallen to just $912 million worth of minerals, which is barely enough to meet half of the Pentagon’s mineral needs and one tenth of critical civilian infrastructure needs, with a total shortfall of $13.5 billion.

China has already shown it is willing to use export controls to exercise leverage over the market, making stockpiling an essential buffer against supply shocks.

Recycling

Recycling rare earth elements typically involves recovering materials from end-of-life products such as electronics, electric vehicle motors, and wind turbine magnets. It offers a promising supplemental source of rare earths because it avoids some of the permitting and development timelines associated with greenfield mining. By 2050, demand for neodymium and dysprosium is projected to exceed extraction volumes by 9 and 35 times, respectively. A secondary supply from recycling could therefore help offset part of the gap between mining output and future demand.

However, recycling has its limits. Traditional recycling methods often rely on chemical treatments that use strong acids or solvents to separate and extract individual rare earth elements, which can create environmentally hazardous waste. There is also a lack of established infrastructure to collect end-of-life products that contain REEs. In 2019, only 15% of electronic waste was collected for recycling in the US, leaving about $57 billion of unrecovered metals in 2020. Another major challenge of rare earth recycling is its economic viability, as the costs of collecting, processing, and refining recycled rare earths often exceed the market value of recovered materials.

Recent funding and research advancements have made recycling rare earths from waste products a more attractive opportunity. In December 2025, the US Energy Department announced a $134 million grant opportunity to support projects that recover and refine REEs from waste products, including the startup Phoenix Tailings. Founded in 2019, Phoenix Tailings developed a cost-effective, carbon-free process for separating neodymium and praseodymium from mining waste, or tailings, without any toxic byproducts or carbon emissions. The company received a $1.6 million grant from the Department of Energy in 2025 and plans to produce more than 3K tons of rare earth metals and nickel by 2026. Given that the environmental impact and hazardous waste of mining processes have always been a forefront concern for expanding rare earth facilities, the US must continue to facilitate new technologies that tackle the difficulties of recycling and create additional sources of rare earths over time. Although current recycling methods cannot generate enough rare earths to replace the output of new mines and facilities, it was estimated in 2024 that developing these kinds of circular economy strategies could increase global rare earth supply by 701K tons and decrease demand by 2.3 million tons over the next three decades.

Japan’s Diversification Strategy: A Case Study In Reducing Dependence

Japan’s rare earth policies provide evidence that dependence on China can be reduced over time through focused policy actions and diversification of rare earths sourcing. In 2010, China restricted rare earth exports to Japan due to a territorial dispute over the Diaoyu or Senkaku Islands, causing rare earth prices to increase by as much as ten times.

The two-month embargo motivated Japan to seek alternative sources of rare earth production, including stockpiling, recycling, alternative technologies, and investments in non-China rare-earth projects such as Lynas. As a result, Japan reduced its dependence on Chinese rare earths from over 90% in 2010 to less than 60% in June 2025, with plans to reduce it further to less than 50% by the end of the year.

Japan’s actions demonstrate that supplemental strategies like stockpiling and recycling can make a significant impact on supply chain resilience over time and provide a model for the US to emulate as we move towards supply chain independence.

The Path to Rare Earth Independence

The US did not just walk away from control of the rare earth supply chain in the 1980s; It was squeezed out by environmental pressure, undercut by Chinese state subsidies, and ultimately outmaneuvered by a rival that understood what these minerals were really worth. China’s real leverage in the rare earth market stems from its control over the most concentrated stages of the supply chain: heavy rare earth production, rare earth processing, and magnet manufacturing. But these elements of the supply chain are not geographically limited, and can be replicated elsewhere under the right financial and environmental conditions.

Late last year, Ionic Mineral Technologies confirmed a major deposit at Silicon Ridge in Utah County, a halloysite-hosted ion-adsorption clay, the same geological formation that supplies approximately 35-40% of China's total rare earth production and over 70% of the world's heavy rare earth elements, sitting quietly in the Lake Mountains an hour south of Salt Lake City. It is one discovery among several early signals that a domestic supply chain, long treated as either impossible or unnecessary, is beginning to take shape.

"We are ensuring that the minerals powering our energy, defense, and technology supply chains are mined and processed in the United States, which is becoming a mineral powerhouse once again," Interior Secretary Doug Burgum said in November 2025 in reference to steps the Trump administration is taking to bolster supply chains for elements on the USGS 2025 List of Critical Minerals. Fueled by momentum in support, the US will be best served by prioritizing rebuilding rare earth manufacturing capabilities through domestic investment, allied partnerships, and industrial policy while using stockpiling and recycling as interim tools to reduce volatility during the long process of rebuilding an independent mine-to-magnet ecosystem outside of China.