Thesis

Construction, mining, and energy are critical industries within the US economy. Yet many of the core workflows in these industries still rely on human workers to perform dangerous tasks in unpredictable physical environments. Construction work alone accounted for nearly one in five worker deaths in the US in 2024. In mining, the fatal injury rate reached 14.2 per 100K workers in 2021. Oil and gas extraction, meanwhile, had a fatality rate of 9.8 per 100K, compared to a national average of 3.8 per 100K across all private industry. In each case, the most dangerous tasks, which include inspecting confined spaces, navigating underground infrastructure, and monitoring a live energy system, require a human to be physically present in the hazardous environment.

Compounding the high fatality risks, these crucial industries are facing worsening labor shortages driven by demographic shifts and an aging workforce. The construction industry will need 2.2 million additional workers between 2024 and 2026 just to meet existing demand. Younger workers are also increasingly unwilling to enter industries like mining, with 71% of employers reporting difficulty hiring, and 70% of respondents aged 15 to 30 saying in a 2023 survey that they would not consider a career in mining. As experienced workers retire and fewer younger workers replace them, operators are increasingly forced to choose between automating physical labor and leaving critical work undone.

Robots are a potential solution, but autonomous systems have historically struggled in unstructured and GPS-denied environments. Conventional robotic systems often depend on pre-mapped environments, reliable GPS connectivity, and predictable terrain for localization and navigation. These requirements limit deployment in mines, construction sites, and industrial facilities where layouts constantly change and sensor visibility is unreliable.

Advances in foundation models and multimodal perception are beginning to address these constraints. Researchers increasingly view foundation models as critical for enabling robots to operate in unstructured physical environments without environment-specific programming. The same technologies that accelerated autonomous driving are now expanding into embodied AI and industrial robotics, improving robots’ ability to navigate dynamic real-world environments with limited prior knowledge.

FieldAI is building autonomy software for robots operating in unstructured, GPS-denied environments. The company develops Field Foundation Models that enable robots to navigate, localize, and complete tasks without pre-mapped environments or environment-specific retraining. Rather than selling hardware, FieldAI sits on top of robots operators already own, making it compatible with the full range of platforms already deployed across industrial environments. This hardware-agnostic approach means each new deployment generates proprietary real-world data that, FieldAI argues, compounds its model performance over time.

Founding Story

FieldAI was founded in January 2023 by Ali Agha (CEO), Shayegan Omidshafiei (President and Chief Scientist), and David Fan (CTO), along with Justin Saeheng, a co-founder who served as COO until departing in 2024. The company’s origins trace back to MIT, where Agha and Omidshafiei first met and worked together while doing their PhDs in robotics.

After completing his doctorate, Agha began his career as a researcher at Qualcomm Research. There, he launched Qualcomm’s efforts in robotic autonomy by developing the first autonomy architectures for its autonomous drones. He then joined NASA’s Jet Propulsion Laboratory (JPL), where he served as a Principal Investigator on some of the nation’s most high-profile robotic autonomy projects over a seven-year tenure.

It was at NASA that Agha first worked with Fan, a doctoral graduate in robotics from Georgia Tech, who served as a researcher in JPL’s aerial mobility group under Agha’s leadership. Notably, Agha worked on NASA’s BRAILLE project, which achieved the first fully autonomous robotic exploration of lava tube caves. Using volcanic caves at Lava Beds National Monument as a stand-in for Martian terrain, the project developed navigation systems capable of operating without maps, GPS, or any prior knowledge of the environment.

The navigation principles Agha developed at JPL were put to a more rigorous test through DARPA’s robotics challenges. Agha led Team CoSTAR, a collaboration across NASA JPL, Caltech, and MIT, through the Subterranean Challenge, a multi-year competition requiring robots to autonomously map and navigate caves, mines, and urban underground infrastructure with no maps or GPS. Fan served as the team’s chief technologist, and together they built NeBula, an uncertainty-aware autonomy framework that powers their robots. CoSTAR placed first in the 2020 Urban Circuit, achieving the first fully autonomous coordination of 11 heterogeneous robots, including legged, wheeled, and aerial platforms, for inspection and search operations in complex environments.

Agha and Fan then carried that work into DARPA’s RACER program, this time applying the NeBula autonomy stack to passenger-sized vehicles navigating open, trail-less outdoor terrain at speed. The JPL NeBula team was one of only three teams selected nationwide for the program. In 2022, they became the first team to complete all eight off-road courses on the first attempt. NeBula, now battle-tested across both programs, became the intellectual foundation for FieldAI’s Field Foundation Models.

Throughout the team’s DARPA years, commercial demand from industrial operators for what they had built began arriving unsolicited after seeing their performance in extreme environments, such as coal mines 900 feet underground. Convinced the technology was ready for the real world, Agha and Fan left NASA to found FieldAI in 2023.

Prior to joining FieldAI, Omidshafiei worked as a leading research scientist at Google and DeepMind, where he led research on single and multi-agent deep reinforcement learning that later contributed to FieldAI’s multi-agent coordination foundation model. He joined FieldAI a year after its founding.

Since its founding, FieldAI has grown to over 180 employees as of May 2026 across engineering, sales, and growth functions. The company brought on Duncan McIntyre as chief financial officer in January 2025. McIntyre studied robotics at the University of Technology Sydney before pivoting to finance, beginning his career as a financial analyst at Macquarie Bank and later building technology companies in the financial and logistics sectors.

Product

Overview

FieldAI’s core product is an autonomy software layer that runs on top of existing robots, enabling them to navigate and operate in unstructured, GPS-denied environments without maps, prior training, or human supervision. Rather than building robots itself, FieldAI sells the intelligence that makes third-party robots deployable in conditions where factory-installed software breaks down. To understand what makes this technically distinct, it helps to consider the primary approaches that have emerged for solving the problem of autonomous robot navigation.

Autonomous Robotic Models

Building autonomous robots that can operate across any terrain and complete diverse tasks without environment-specific training has been a long-standing goal in robotics. Most autonomous robotic systems in 2026 were designed for specific tasks, trained on specific datasets, and deployed in already known environments. When deployed in real-world scenarios, such systems face significant generalization issues and struggle to remain robust to distribution shifts. Two competing approaches have emerged to address this problem.

Vision-language action (VLA) models combine visual perception and natural language understanding to generate an appropriate action for a given context. This approach provides a shortcut to learning, drawing on a vision-language model’s (VLM) internet-scale datasets that already understand images and language, and simply layering a motor command. The model is then fine-tuned on robotics-specific data to adapt it for physical tasks. However, VLA models over-rely on 2D visual inputs when performing actions in a 3D physical environment, leaving a substantial gap between visual perception and embodied action. In the field, this translates to a robot that can recognize a ditch but misjudges whether it can step over it.

Robotic foundation models (RFMs) offer a solution. They address the shortcomings of VLA models by training directly on data from real-world robot interactions rather than merely fine-tuning them. Rather than inferring physics from images, RFMs learn it directly from sensor data, force feedback, and the outcomes of past physical actions. This also allows RFMs to generalize to entirely new environments and tasks without prior training. FieldAI’s models are built on this principle.

Field Foundation Models

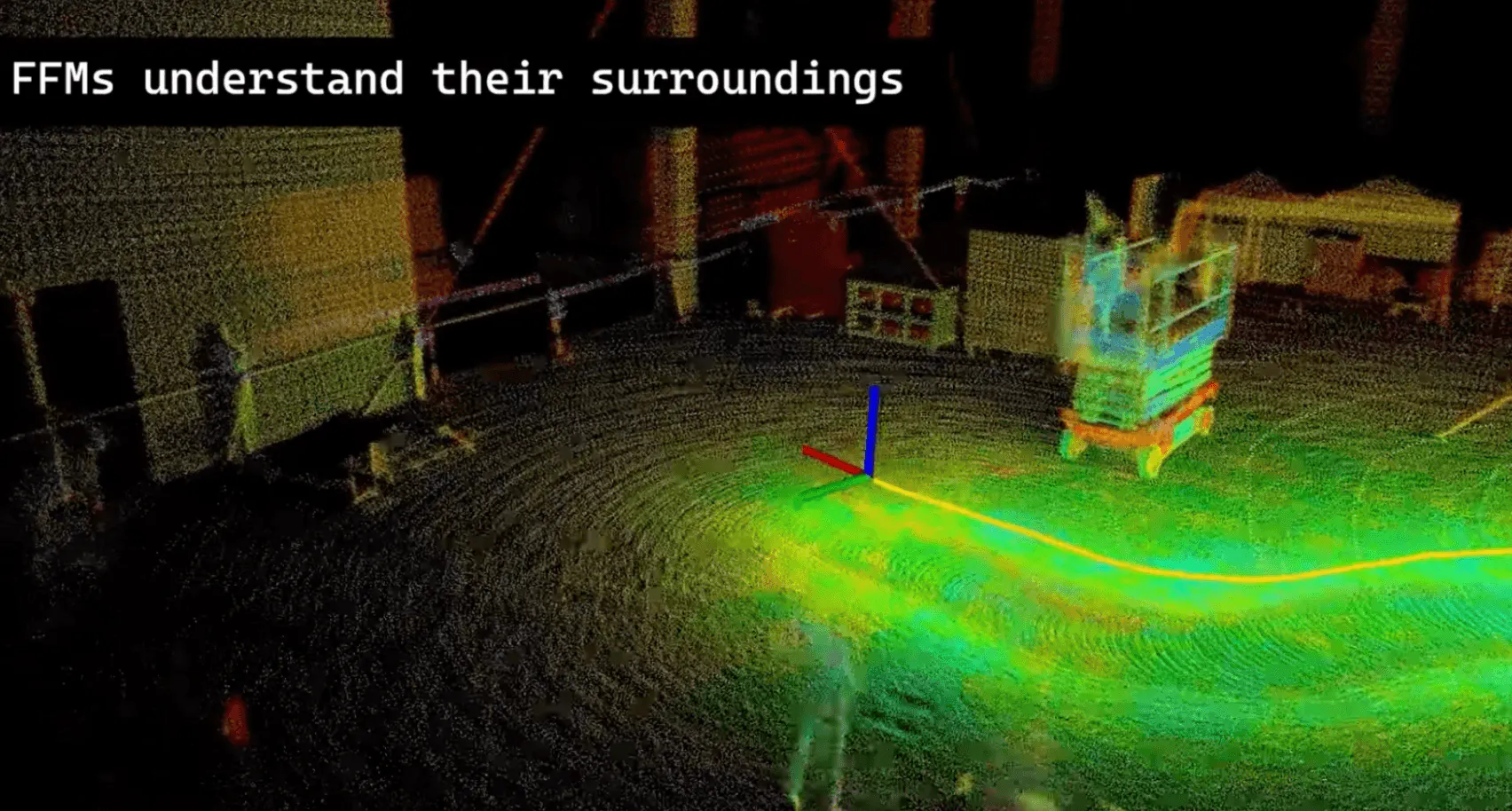

FieldAI provides embodiment-agnostic, uncertainty-aware software that enables robots to navigate unstructured environments without maps, GPS, or predefined trajectories. FieldAI’s Field Foundation Models consist of two specialized foundation models and a safety and risk-awareness layer, all of which operate through a Belief World Model that serves as the system’s predictive engine. Rather than reacting to sensor inputs, the Belief World Model continuously maintains and updates an internal representation of the robot’s environment, reasoning under uncertainty before committing to any action. Together, these components build context from real-world deployment rather than requiring vast amounts of scenario training data.

Source: FieldAI

FieldAI’s Dynamics Foundation Model determines motion feasibility. The model combines real-world physics principles (e.g., terrain resistance) and the robot’s mechanical specs (e.g., joint motion) to make precise, physically realistic decisions. Meanwhile, FieldAI’s Multiagent Foundation Model (MFM) coordinates behavior across multiple robots. Through this, robots in a fleet autonomously share situational awareness and divide tasks without human intervention.

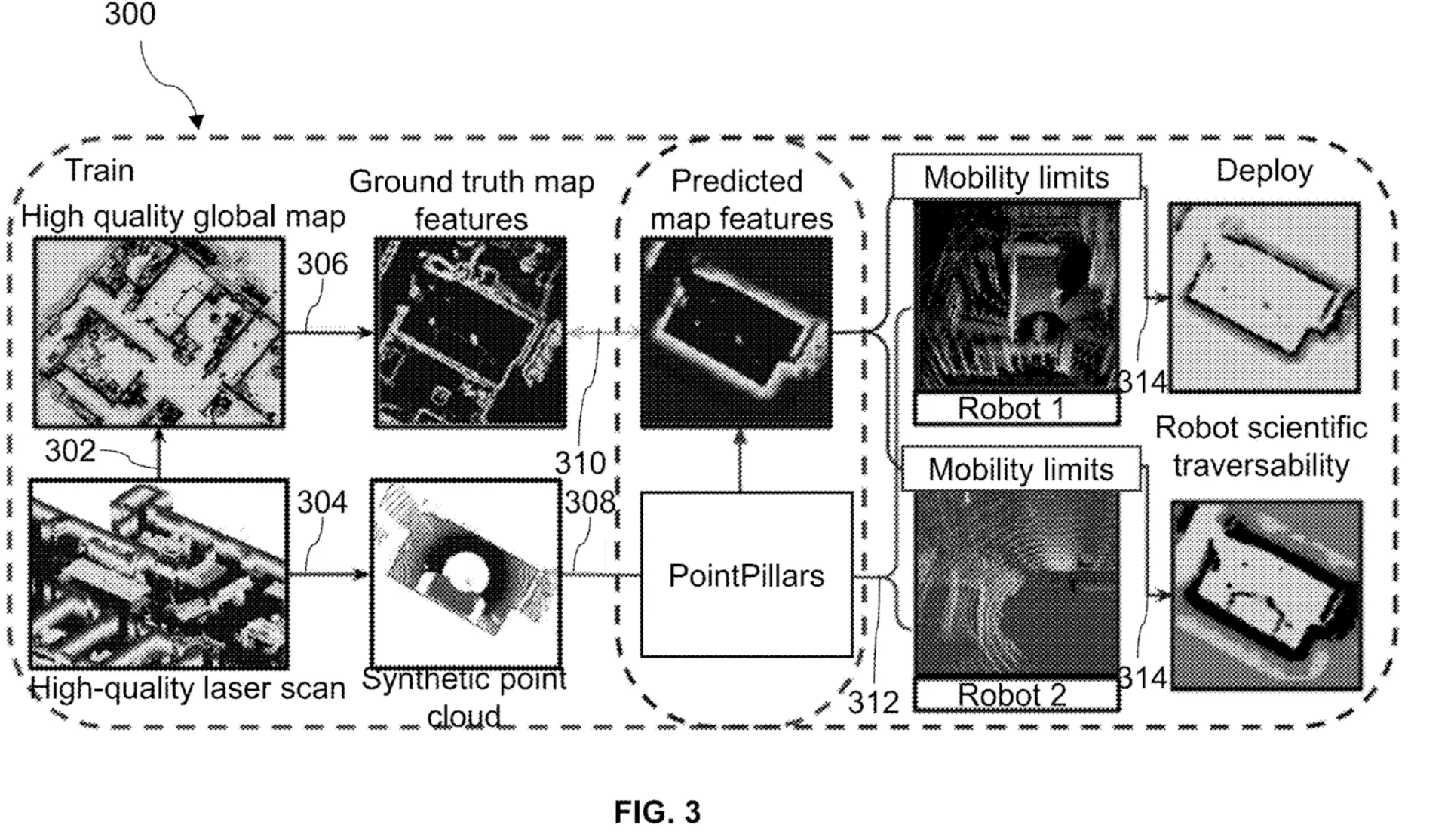

The safety and risk awareness layer evaluates and filters action commands generated by the two foundation models by modeling uncertainty before committing to an action. FieldAI describes this as the first uncertainty-aware capability built into a robotic foundation model. In rugged industrial environments, dynamic conditions and sensor noise make it difficult for robots to assess whether the terrain is safe to traverse. To address this problem, FieldAI uses a machine learning framework trained on degraded scans that simulate the output of low-resolution field sensors. The model’s training dataset consists of the original, optimum-fidelity scan data and synthetic point clouds, which it then adds noise to. Using these inputs, the system predicts terrain features (slope, step height) and expresses traversability as probability distributions.

Source: FieldAI Patent Application

The safety and risk-awareness layer is what separates this architecture from most general-purpose autonomy models. In industrial environments, software failures are not minor inconveniences. A missed chatbot response or failed object pick can usually be retried. A mistake made by a 5K-pound machine operating around workers, scaffolding, or heavy infrastructure can have real physical consequences. As Agha explains, these systems cannot operate at the reliability standards acceptable in consumer AI. He argues that industrial autonomy must operate at a reliability closer to 99.999% because there is often no safe margin for error.

Deployment

FieldAI’s product has two delivery layers: a sensor-compute payload that attaches to existing robots, and EDGE, FieldAI’s on-device software runtime that packages and deploys the Field Foundation Models directly onto the robot’s onboard hardware.

Rather than relying on a cloud connection to process decisions, EDGE runs the FFMs locally on the payload, enabling sub-100-millisecond latency and full offline functionality in GPS-denied or connectivity-limited environments, such as underground mines. The data collected by deployed robots then gets uploaded to FieldAI’s cloud platform for analytics, feeding a federated learning process in which individual robots learn from the collective fleet across a decentralized network, continuously improving the foundation models without sharing raw data. In a talk delivered at Emerson Collective’s 2026 Demo Day, Agha explained:

“If a robot in Japan steps on wet concrete, learns a new skill, tomorrow, the robot in San Diego will learn from that skill, and that core learning makes the pace of evolution of these autonomy and AI models exponentially fast.”

Deployed robots perform tasks including progress and object tracking, high-precision inspection and equipment readings, object manipulation and transportation, and surveillance of dynamic environments.

Source: FieldAI

Market

Customer

FieldAI customers operate in dirty, dull, and dangerous conditions. The ideal customer profile for FieldAI is an industrial operator who needs a fleet of robots to work reliably in environments that are too dynamic, hazardous, or GPS-denied for a robot’s factory-installed software to handle. FieldAI’s software layer sits atop existing hardware, replacing the OEM autonomy stack while remaining embodiment-agnostic, enabling a single deployment of FFMs to coordinate a mixed fleet in a shared environment.

Across the industrial sectors FieldAI targets, the status quo remains the same: either a human enters a dangerous environment, or the task doesn’t get done. That status quo holds across FieldAI’s core verticals (construction, mining, energy and utilities, and security), where human labor is both costly and dangerous. FieldAI Federal, a standalone division, serves federal defense and government customers through a business-to-government sales motion distinct from the company’s commercial go-to-market strategy.

DPR Construction is a notable customer of FieldAI, which began its partnership with the company in 2024. According to a DPR superintendent, the initial primary use for the FieldAI system was “tracking of construction through photography.” According to FieldAI, its deployment with DPR as of November 2025 included 45K+ photos captured for documentation and analysis, four full floors mapped, 125K square feet of documented roofing, and 500K square feet of scanned interiors. As the DPR superintendent reported, FieldAI’s impact was substantial:

“The FieldAI system makes us better at what we do. Giving us greater efficiency, helping us document items more effectively, and taking some of the more mundane tasks off our plate, letting us focus on the more detailed, critical tasks. As the FieldAI system develops, I think it will allow our teams to focus on building safer and higher-quality projects.”

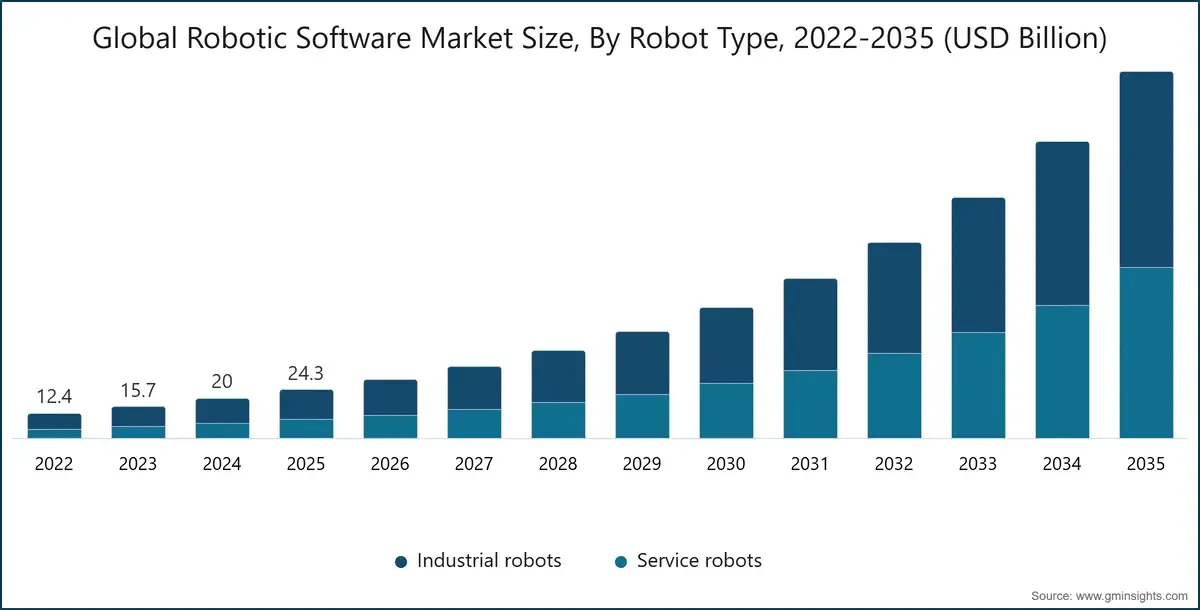

Market Size

The robotic autonomy software market was valued at $24.3 billion in 2025 and is expected to grow to $185 billion by 2035, representing a 22.6% CAGR. Within that, the embodied AI segment, which represents FieldAI’s foundation model approach, was valued at $4.4 billion in 2025 and is projected to reach $23.1 billion by 2030, growing at a 39% CAGR.

Both figures may understate FieldAI’s addressable market. Because its software retrofits existing robots rather than being embedded in new hardware, FieldAI’s addressable base includes every industrial robot already in the field. Industrial robots commanded 67.3% of the AI-in-robotics market in 2025, with an installed base surpassing 4.3 million units in factories worldwide, each a potential retrofit opportunity. That installed base is the theoretical ceiling; FieldAI’s near-term wedge is the harsher, GPS-denied subset of environments where factory-installed software breaks down. The number of deployed robots is expected to grow significantly, with projections indicating that over 2.5 billion robots will operate globally by 2035.

The segments FieldAI targets sit at the higher end of that demand curve, with customers in mining, energy, and construction among the most willing to pay a premium for autonomous robotics, given the safety and labor dynamics that define their industries.

Source: Global Market Insights

Competition

Competitive Landscape

In the landscape of embodied AI, two distinct groups of competitors have emerged: 1) players who develop general-purpose foundation models and 2) specialists who focus on specific environments. General-purpose foundation model players remain largely pre-commercial, competing on benchmark performance rather than proven deployment at scale. By contrast, environment-specific specialists have spent years collecting real-world operational data in a single context, teaching their models the physical properties and edge cases of that environment in ways that simulation cannot replicate.

FieldAI positions itself between these two camps: more field-proven than lab-first foundation model players and more generalizable than environment-specific specialists. On the general-purpose side, its most relevant competitors are Physical Intelligence and Skild AI; on the specialist side, its most relevant competitors are Exyn Technologies, Gecko Robotics, and Bedrock Robotics. A separate category of indirect competitors encompasses vertically integrated robotics manufacturers. Companies like Figure, Tesla, and 1X build full-stack hardware and software for robotic autonomy. Although they are not competing for the same customers, they are competing for the same market. These companies embed intelligence directly into their robots, targeting the same industrial end markets through a closed-platform model.

Competitors

Direct Competitors

Skild AI: Skild AI was founded in 2023 by two former Carnegie Mellon computer science professors. As of June 2026, it had raised over $1.8 billion in total funding and was valued at $14 billion following its $1.4 billion round in January 2026. That round was led by SoftBank, with participation from Sequoia, NVIDIA’s NVentures, and Bezos Expeditions.

The company develops a universal robotic foundation model, called Skild Brain, that serves as an operating system for robot hardware. After mapping a robot’s joints and sensors to the software’s API, the robot can autonomously perform manipulation and navigation tasks without needing task-specific programming. The foundation model is trained on trillions of synthetic simulation episodes and millions of real-world frames, then fine-tuned on live robot deployments.

Skild AI can be seen as a competitor to FieldAI, as both companies are developing hardware-agnostic autonomy software. They differ in their target deployment environments and go-to-market strategies. Skild AI is designed primarily for structured indoor settings, such as warehouses and logistics facilities, where robots operate in predictable, mapped environments. Its April 2026 acquisition of Zebra Technologies’ robotics automation business, a platform built specifically for warehouse orchestration, reflects a deliberate push deeper into that environment. Skild AI also pursues a horizontal OEM platform strategy, embedding its software directly into hardware partners and charging a per-use license fee, rather than FieldAI’s direct enterprise sales motion targeting industrial operators.

Physical Intelligence: Physical Intelligence was founded in 2024 by a team of Google DeepMind researchers. In November 2025, only a year after its founding, Physical Intelligence raised a $600 million Series B, bringing its valuation to $5.6 billion and total funding raised to $1.1 billion. Alphabet Inc.’s independent growth fund, CapitalG, led the round. Other key investors include Sequoia, Thrive Capital, and Bezos Expeditions. As of March 2026, the company was reportedly in advanced discussions to raise $1 billion, which would nearly double its valuation to over $11 billion once closed.

Physical Intelligence launched its flagship model π0 (Pi-zero) in October 2024. The first member of its π foundation model family, π0, is pre-trained on Google’s VLM PaliGemma to develop a general semantic understanding. The model is then fine-tuned on a custom dataset collected from seven different robot forms performing 68 tasks, as well as on Google’s Open X Embodiment dataset. Each subsequent model iteration has pushed further on dexterity, task complexity, and cross-embodiment generalization. In April 2026, Physical Intelligence released π0.7, the first model capable of composing skills it already knows to attempt tasks it has never seen before.

While both companies aim to create general intelligence across robot form factors, their focuses and approaches diverge. FieldAI specializes in navigation and environment mapping, while Physical Intelligence focuses on task manipulation. Physical Intelligence has no commercialization timeline; it is explicitly research-first, with almost all raised capital allocated to compute and data collection and no commercial product deployed or revenue generated. It is betting that whoever builds the best foundation model will eventually power every robot.

Exyn Technologies: Exyn Technologies was founded in 2014 as a spinout from the University of Pennsylvania’s GRASP Lab. The company develops ExynAI, an autonomy and mapping platform designed for GPS-denied industrial environments. Exyn Technologies went public in May 2026, raising $19.4 million at a $44.3 million market cap. It reported $5.8 million in revenue in 2025, up 4.4% year over year, with a net loss of $12.2 million.

Exyn Technologies’ flagship product, Nexys, uses lidar to generate real-time 3D point clouds in underground mines, construction sites, and hazardous industrial facilities without needing GPS, prior maps, or a human operator. Nexys deploys across handheld, drone, and quadruped-mounted configurations, and its outputs are used for volumetric analysis, structural inspections, and operational planning.

Exyn Technologies shares the closest environmental overlap with FieldAI, operating in the same GPS-denied, unstructured industrial settings. The distinction is scope. Exyn Technologies’ autonomy is designed for a specific workflow: enter an environment, map it, and return survey-grade spatial data. FieldAI is building models that continuously operate across those same environments, coordinating robot fleets, executing tasks, and adapting as conditions change over time.

Gecko Robotics: Founded in 2013, Gecko Robotics builds wall-climbing inspection robots paired with an AI software platform for monitoring industrial infrastructure across energy, defense, and manufacturing. In June 2025, the company raised a $125 million Series D at a nearly $1.3 billion valuation, bringing total funding to $349 million. Its robots use magnetic wheels to crawl steel surfaces such as boiler tubes, tank walls, and pipelines, feeding sensor data into its Cantilever software to predict asset failures. Unlike FieldAI, Gecko builds proprietary hardware tuned to a specific inspection workflow rather than a hardware-agnostic intelligence layer, but it competes for the same industrial inspection budgets in overlapping verticals.

Bedrock Robotics: Bedrock Robotics, founded by a team of former Waymo engineers, emerged from stealth in July 2025 and develops an autonomy kit that retrofits construction equipment such as excavators, bulldozers, and loaders for unmanned operation. In February 2026, the company raised a $270 million Series B co-led by CapitalG and the Valor Atreides AI Fund, bringing total funding to more than $350 million. Bedrock’s retrofit-existing-hardware model and construction focus overlap directly with FieldAI’s approach, though Bedrock concentrates on operating heavy earthmoving machinery rather than coordinating mixed fleets across verticals.

Indirect Competitors

Tesla: Tesla was founded in 2003 by Martin Eberhard and Marc Tarpenning, with Elon Musk later recognized as a co-founder. Tesla is a vertically integrated electric vehicle manufacturer that develops its own proprietary autonomy software. As of June 2026, the company is publicly traded with a market cap of $1.5 trillion.

Optimus is Tesla’s general-purpose humanoid robot, designed to perform repetitive and physically demanding tasks in factory and industrial settings. The robot runs on Tesla’s in-house VLA autonomy stack, built on the same neural network and computer vision architecture developed for Full Self-Driving. Tesla’s neural world simulator is trained on data from its fleet of millions of vehicles, compounding intelligence across every car on the road in much the same way FieldAI’s federated learning model compounds across every deployed robot.

Tesla has indicated that its initial deployment strategy for Optimus focuses on internal use within its own factories. On Tesla’s Q4 2025 earnings call, Musk said Optimus remains in the R&D phase and is not yet being used in Tesla’s factories “in a material way,” with current deployment focused primarily on helping the robot learn through real-world task execution and iteration.

Figure: Figure was founded in 2022 by Brett Adcock. Figure produces general-purpose humanoid robots for task manipulation. Following a Series C round in September 2025 that exceeded $1 billion, Figure is valued at $39 billion and has raised a total of $1.9 billion as of June 2026. Its robots closely resemble the human form, with its first model standing at 5 ft 6 in and weighing 60 kg, and operate autonomously in unstructured environments while responding to verbal commands.

Figure has developed three generations of humanoid robots: Figure 01, Figure 02, and Figure 03. Figure 03, the latest model introduced in October 2025, can navigate stairs, ramps, and uneven terrain using onboard stereo cameras without any task-specific programming. On the manipulation side, it can handle household tasks such as folding clothes and loading the dishwasher. The robots are powered by their in-house VLA model, Helix, which can control up to two robots simultaneously.

Figure 02 has already been deployed on BMW’s Spartanburg assembly line to build production vehicles, while Figure 03 is being piloted in warehouses and home environments. Unlike FieldAI, which treats form factor as interchangeable and bets on owning the intelligence layer, Figure bets that the humanoid form factor will become the dominant robotic form factor and is racing to own it end-to-end.

1X: 1X was founded in 2014 by Bernt Børnich. 1X’s first robot was EVE, a wheeled humanoid for logistics and security environments. This model was followed by NEO, a bipedal humanoid, unveiled in 2024. As of May 2026, the company has raised $136.5 million in total funding. In September 2025, 1X entered talks to raise up to $1 billion, targeting a $10 billion valuation, up 12x from its $820 million valuation following its $100 million Series B in 2024 led by EQT Ventures.

NEO uses a tendon-driven system that mimics how human tendons connect muscles to bones, delivering human-like strength while making incidental contact far less dangerous. Its robots are powered by the 1X World Model, which uses internet-scale video pre-training to simulate the physical outcome of any action before executing it. This method differs from standard real-world data collection by using simulated physical outcomes derived from internet-scale video to generalize across tasks. For tasks the World Model cannot yet handle autonomously, a human “1X Expert” steps in remotely to complete the task while NEO observes and learns, feeding that interaction back into the model as training data.

In contrast to FieldAI’s real-world, data-driven moat, 1X attempts to create generalizable physical intelligence through internet-scale video pre-training. In early tests, NEO achieved a 95% success rate on tasks such as steaming a shirt and an 80% success rate on object retrieval. However, for newer tasks like scrubbing dishes, which NEO was never explicitly trained for, the success rate is 20%. If successful, this method would offer a faster, cheaper path to generalizable autonomy by circumventing the costly process of collecting real-world data.

Business Model

FieldAI operates on a software subscription model. One unverified report suggests that customers pay an initial integration fee to install sensor-compute payloads, then a recurring license fee for access to the FFM software. This makes the model relatively asset-light from a software perspective, though the hardware payload adds some capital and logistics complexity versus pure software peers.

FieldAI’s go-to-market motion positions each sale as fleet modernization rather than as capex-intensive new-robot procurement. As procurement cycles are long in the capex-intensive industries FieldAI targets, it likely uses a land-and-expand strategy to increase contract value per account. One potential future revenue source is OEM licensing: embedding the FFM software directly into partners’ hardware in exchange for per-unit or royalty-style fees that would scale with shipments rather than requiring direct customer contract wins.

Traction

As of May 2026, FieldAI has not publicly disclosed its full-year revenue figures or number of customers. However, Agha said in March 2026 that FieldAI has more than several hundred mission deployments with customers across three continents (Asia, Europe, and North America), including some of the largest construction, manufacturing, and data center firms in the world. FieldAI’s partnerships with Boston Dynamics and NVIDIA materially expand its deployment opportunities by integrating its AI stack with proven robotics hardware and high-performance computing infrastructure.

The partnership with Boston Dynamics allows FieldAI to expand deployment and collect real-world training data at scale in unpredictable industrial environments. One environment is construction, characterized by constantly evolving sites, shifting terrain, and active human workflows. Through this partnership, FieldAI reduced site inspection and documentation time by more than 90% compared to manual processes, while also reducing worker exposure to hazardous areas. As part of the partnership, FieldAI has expanded the deployment of FFM-operated Spot robots, creating one of the world’s largest third-party quadruped fleets.

By partnering with NVIDIA, FieldAI gains access to NVIDIA’s Omniverse simulation libraries, enabling it to create realistic digital twins of real environments from large volumes of on-site robot data. Among other tools, FieldAI uses NVIDIA Omniverse NuRec, a 3D reconstruction technology that converts raw sensor data into detailed 3D simulations of physical spaces. NVIDIA also supports training at scale through its Cosmos world models, which generate synthetic environments and scenarios to accelerate robot learning and improve model robustness.

Valuation

FieldAI has raised approximately $405 million in total funding as of June 2026. Its $405 million Series A funding round was announced in August 2025 and valued the company at over $2 billion. The team has indicated that the new capital would accelerate the commercial expansion of its Field Foundation models and support deployments across complex industrial environments. FieldAI also received an undisclosed strategic investment from Hyundai Motor Group in February 2026. Other investors include Khosla Ventures, NVIDIA, and Intel’s corporate venture capital arms, NVentures and Intel Capital, respectively.

Source: PitchBook

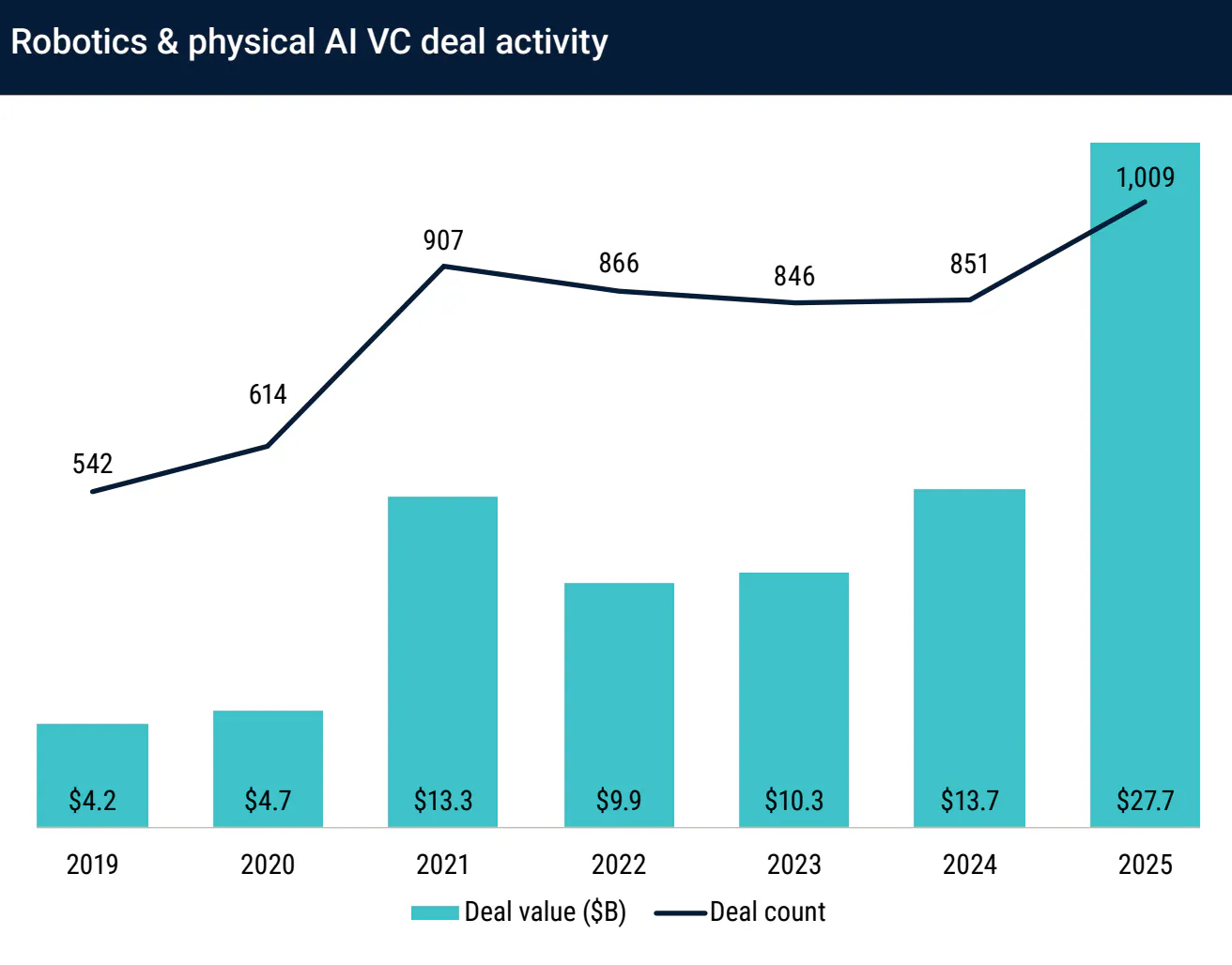

Robotics and physical AI startups attracted $27.7 billion in private capital funding in 2025, more than double the $13.7 billion raised in 2024. The segments most relevant to industrial autonomy are growing the fastest, with investment in hazardous-environment robotics across energy, mining, and heavy manufacturing growing 128% year over year. This growth represents a rapidly expanding installed base of robots for FieldAI to sell its software into.

Key Opportunities

Federated Learning Flywheel

Robotics training data remains one of the biggest bottlenecks in the robotics industry. As of May 2026, the total amount of global robot manipulation data is estimated at only 300K hours, compared to roughly 1 billion hours of internet video and hundreds of trillions of text tokens available for large language models. Collecting high-quality robotics data is slow, operationally complex, and extremely expensive. Industry-wide spending on robotics data collection is expected to surpass $3 billion over the next two years, driven by teleoperation, demonstrations, simulation generation, and human labeling efforts. The companies that most efficiently scale proprietary data collection are likely to define the next generation of embodied AI.

However, it is worth noting the bitter lesson as a caveat for this data moat. The lesson states that general methods backed by raw compute and scale have consistently outperformed, and will continue to outperform, carefully constructed domain-specific approaches. The bottleneck in robotics training data may prove less durable than it appears if general-purpose vision models trained on internet-scale visual data develop sufficient physical reasoning to generalize into industrial environments.

FieldAI creates a structural advantage by turning every robot in the field into a continuous data source using federated learning. As the fleet grows, so do the models. Since better models attract more deployments, more deployments generate more data. That data moat is difficult to replicate through other methods. Simulation through synthetic environment data can approximate physics but cannot reproduce the variability of real industrial environments at scale. Teleoperation and demonstration collection can generate real data, but at a high fixed hourly cost with limited throughput. On the other hand, FieldAI’s fleet generates data across dozens of environments simultaneously without incremental cost.

Regulation Favoring Risk-Aware Autonomy

As robots move into industrial environments, regulators are placing greater scrutiny on how autonomous systems make decisions and manage risk. Under the EU AI Act, many AI systems connected to industrial machinery and workplace operations are classified as “high-risk” systems. Those systems must meet requirements around reliability and operational transparency before deployment.

FieldAI’s architecture is built around explainability. Its Belief World Model continuously maintains an internal representation of the robot’s environment and updates it as conditions change. The system is designed to reason about physical context and uncertainty before taking action rather than simply predicting the next behavior from sensor input alone. That distinction could become increasingly important as industrial customers and regulators require more explainable and auditable autonomy systems. A robot that models decision uncertainty and behaves predictably in changing conditions is easier to certify, easier to insure, and ultimately easier for enterprises to trust in safety-critical operations.

Key Risks

OEM Platform Dependency

The robotics industry is moving toward full-stack systems where the robot hardware, training data, and autonomy models are built together from the start. A company training models directly on its own sensors, hardware, and deployment data will likely have an advantage over software designed to work across many different platforms. Many of the largest robotics companies are already moving in this direction. Tesla, Figure, and other humanoid developers have publicly emphasized vertically integrated AI stacks, where the robot, training infrastructure, and autonomy models are developed together. Boston Dynamics, FieldAI’s most prominent hardware partner, has formalized a strategic partnership with Google DeepMind to integrate Gemini Robotics foundation models directly into its Atlas humanoid robot, signaling a deliberate move to build its own in-house intelligence layer.

For FieldAI, there is a real risk that OEMs view third-party autonomy software as a temporary solution rather than a permanent dependency. A robotics company may initially partner with an external provider to accelerate deployments and shorten development timelines. But once it has enough real-world deployment data and internal model development capabilities, it has a strong incentive to bring those systems in-house. That incentive only increases as fleets scale, because data from real-world robot operations becomes one of the most valuable inputs for improving autonomy models over time. Over time, this could leave less room for independent autonomy providers altogether. If the market consolidates around a handful of vertically integrated robotics platforms, companies like FieldAI could lose access to both major OEM customers and the deployment data needed to continue improving their models.

Hardware Supply Chain Risk

FieldAI’s growth depends on how quickly its hardware partners can build and ship robots. Supply chain disruptions, component shortages, and rising hardware costs all slow that process, and when deployments slow, so does FieldAI’s revenue. That exposure is shaped heavily by international supply chain volatility. The robotics industry relies on supply chains concentrated in Asia, with critical components including sensors, microprocessors, actuators, and control systems sourced primarily from China. As tariffs have raised the cost of these parts, manufacturers have faced increased production costs that are rippling across the entire robotics value chain. Unitree, a leading Chinese robotics manufacturer, saw the US price of its G1 humanoid robot rise sharply as a direct result of tariffs.

When robot costs rise sharply, the economics behind automation start to weaken. That pressure is already showing up across the market. In 2025, tariff uncertainty had pushed manufacturers into a “wait and see” mode and was beginning to stifle capital investment across industrial automation. Industry executives have also warned that some robotics deployments are no longer economically viable under the current tariff environment. FieldAI’s structure means it absorbs the downstream consequences of all this without the tools to address them. Hardware OEMs can redesign around cheaper components, negotiate directly with suppliers, or adjust pricing strategies. FieldAI sits above that entire layer. Its revenue is a direct function of deployment volume, which is constrained by cost pressures beyond its control.

Summary

FieldAI is building an autonomy software layer designed specifically for conditions where conventional GPS-reliant systems fail: the dangerous, labor-constrained industrial work that still requires a human on-site. Its hardware-agnostic model and real-world deployment base give it a compounding data advantage that is difficult to replicate through simulation alone. The key question is whether FieldAI can scale its deployed fleet fast enough to entrench its software before hardware OEMs develop the internal capability to bring advanced autonomy in-house. If it can, the data moat becomes self-reinforcing. If it cannot, the third-party autonomy layer it is building risks being displaced by vertically integrated platforms with captive data pipelines.