Thesis

The COVID-19 pandemic further entrenched the dominance of Britain’s biggest banks — Barclays, HSBC, NatWest, and Lloyds. These top four held over 50% of UK deposits in 2020 and supplied over 80% of government-backed loans to SMBs during the pandemic. The largest banks also hold 43% of the UK mortgage market, significantly more than in other countries where insurance companies and non-bank lenders have a larger role.

The 2010s saw the rise of neobanks, also known as digital banks or challenger banks. Neobanks offer various financial services, from checking and savings accounts to loans and debit cards. Neobanks often have lower fees and minimum balance requirements than traditional banks, making them more accessible to more people. Moreover, neobanks typically aim to make banking simple and convenient for customers with easy-to-use apps. The COVID-19 pandemic also accelerated the transition to digital banking, forcing many people to use digital banking products for the first time. A 2021 survey showed that only 34% of banked adults think that there are clear differences between the digital offerings from the big banks, and 28% agree that digital-only banks are the most innovative providers. In 2022, 14 million adults in the UK held at least one account with a digital-only bank.

Monzo is a London-based challenger bank that aspires to change how banking is provided in the UK by addressing the poor service, low trust, and onerous fees frequently experienced with traditional banks. It wants to build a mobile-based financial hub for its customers. Originally the company offered financial products through bank partnerships, but as of 2017, Monzo received its banking license and became a fully regulated UK bank.

Founding Story

Monzo was founded in London in 2015 by Tom Blomfield (ex-CEO), Gary Dolman (ex-CFO), Jason Bates (ex-CCO), Jonas Templestein (CTO), and Paul Rippon (ex-CRO).

Before founding Monzo, ex-CEO Blomfield had an early interest in tech and entrepreneurship. He began building websites as a teenager, then started his first company Boso when he was a 21-year-old at Oxford Law School. Although that business failed to raise any money, his second venture GoCardless was accepted to Y Combinator and remained in business even after Blomfield’s departure. After a brief stint at Grouper, a dating startup based in New York, Blomfield joined the team at Starling Bank as the Chief Technical Officer before moving on to start his own challenger bank with the help of Passion Capital and Y Combinator.

The founding team met while working at Starling Bank, another London-based neobank founded in 2014. Blomfield was the founding CEO of Monzo and served as CEO until he became President in 2020 before departing the company entirely in January 2021, citing mental health struggles. Dolman was the CFO of Startling Bank. Gates was the co-founder and Chief Customer Officer of Starling Bank and later held the same title at Monzo until his departure in 2016, just one year after the company was founded. Templestein was an engineer at Starling Bank and returned to being Monza's CTO in 2020 after leaving the role in 2018. Rippon was the co-founder and Chief Risk Office at Starling Bank and later held the same title at Monzo until becoming the deputy CEO and departing in 2019.

Monzo launched with 500 alpha users in October 2015. The founding team hosted community events to create an enthusiastic customer base and convey how Monzo differed from traditional banks. Customers were invited to invest in the company. Additionally, Monzo ran hackathons that allowed early adopters to utilize the app's API. User-generated ideas, such as rounding up spare change, were incorporated into the product. The team’s first product was a prepaid bank card used to gather customers and build the infrastructure necessary to eventually obtain its banking license, which it did two years after its founding. Originally called Mondo Bank, the company was renamed in 2016 due to a copyright issue. The new name resulted from a naming suggestion contest organized by the founding team that received more than 10K user suggestions, six of which were “Monzo Bank.”

The founding team launched its digital finance platform with the slogan “Make Money Work For Everyone” and the belief that it could solve what traditional banking couldn’t by bringing convenience and transparency to banking. The team built an app-based experience where its customers could do all of their financial tasks from a phone, including storing money, sending and receiving payments, budgeting, and accessing capital through loan products and buy-now-pay-later (BNPL) options. Eventually, Monzo added several business banking products and began expansion into the US in 2021.

Product

Monzo Current Accounts

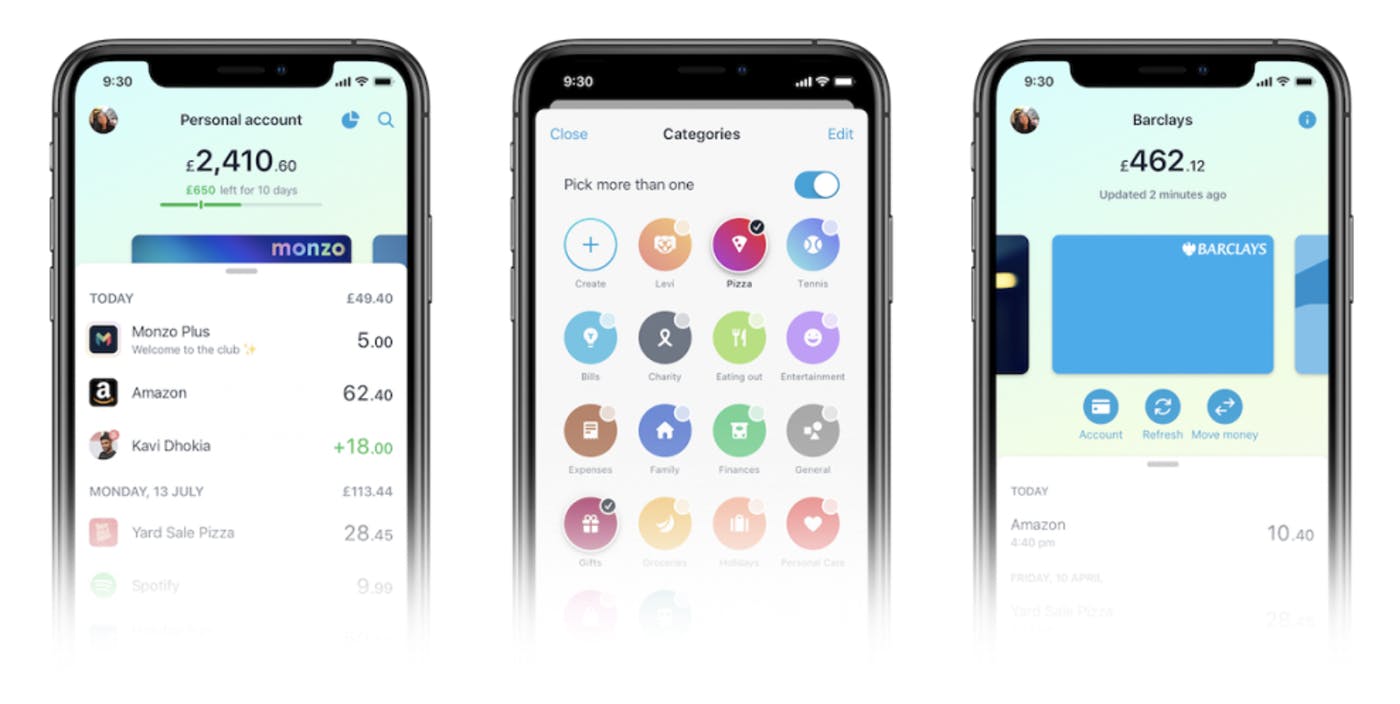

Monzo offers free current accounts that let users spend, save and manage their money. The Financial Services Compensation Scheme (FSCS) protects eligible deposits up to £85K per person. Users can move their existing bank accounts to Monzo in seven days with its Current Account Switch Service. It also offers fee-free bank transfers within the UK and supports Apple Pay and Google Pay. The offering also lets users get a detailed view of their spending.

Monzo Pots

The offering lets users get a detailed view of their spending. “Pots” is a feature that allows customers to put aside money from their primary checking account balance for specific items (for example, customers can use Pots labeled for travel or buying a car). When users spend more than £1, Monzo will round up the change to the nearest pound and add it to their “savings pot”. Monzo thus helps users build a saving habit by putting money aside automatically every time they spend. Account holders can earn up to 3.46% interest on savings on a 12-month “fixed pot” with a £500 minimum deposit to open. This locks the deposited money away for a period of 12 months while users earn interest on it.

Monzo Flex

Monzo Flex is a buy-now-pay-later solution that allows customers to purchase items on credit and repay the purchase over installments. It's interest-free if users pay in full on their next monthly payment or over 3 monthly payments. Users can pay over 6-12 monthly payments along with interest. Arranged overdrafts can help customers by adding extra money up to a limit to their accounts if they overspend their balance. It is paid back at a 19%, 29%, or 39% equivalent annual rate (EAR), depending on the credit limit approved for that specific customer.

Source: Monzo

Monzo Plus Accounts

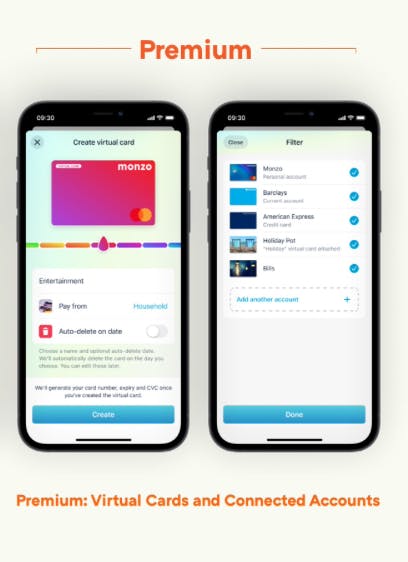

Monzo Plus provides the same free features as “current accounts”, plus the ability to add other bank accounts and credit cards into the Monzo app to see all financial accounts in one place. A Monzo Plus account costs £5 monthly. Users can see their balances and transaction history for up to three years and move money around with bank transfers. Monzo Plus allows users to personalize their cards by giving them names and picking from various colors. Users can create custom categories to group spending and earn interest on up to £2K in their account balance. Users can take out up to £400 cash abroad for free every 30 days. Other features include a holographic card, virtual cards for online spending, and a credit tracker.

Source: Monzo

Monzo Premium Accounts

Monzo Premium costs £15 per month and includes all “plus” features, along with a signature white metal card. It also offers phone insurance that covers theft, loss, accidental damage, and cracked screens. Users can automatically put aside two, five, or 10 times as much spare change every time they spend. Account holders can earn 1.50%/1.49% annual equivalent rate (AER) /gross (variable) interest on up to £2K in their current account and pots. Users can take out up to £600 cash abroad for free every 30 days, get discounted airport lounge access, and make five free monthly cash deposits.

Source: Y Combinator

Monzo Joint Accounts

Monzo offers joint accounts for partners, friends, and roommates. With joint accounts, spending shows up in a single transaction feed. Each transaction is automatically tagged with a profile photo of the holder, so holders can know who paid for what. Users can instantly move money from their personal Monzo account into a joint account. They can also connect an external account and transfer money. The joint account co-owner won’t see the accounts that are connected but will see the money that is added.

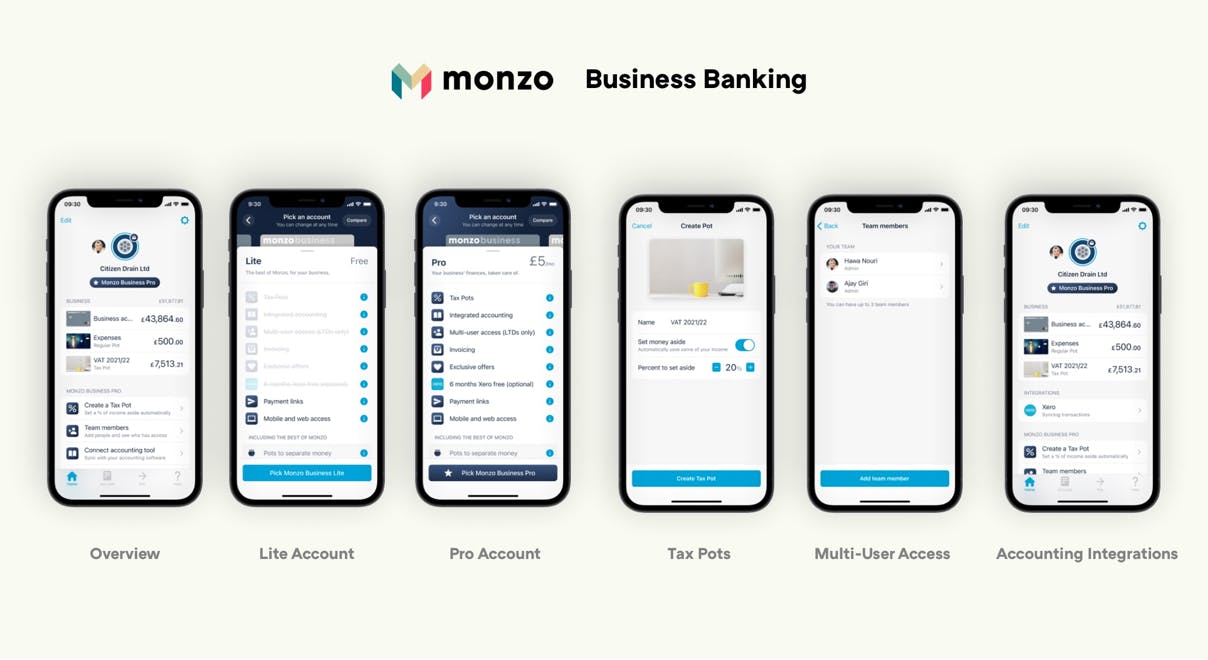

Monzo Business Accounts

Monzo’s business offering helps small businesses stay on top of their finances. It can be opened by phone and allows businesses to give customers simple ways to pay online. Businesses can connect accounting tools to the account and use separate virtual cards for each pot they create, helping them control where they spend from.

Monzo offers two business accounts. The free “Lite” account serves basic banking needs, including pots, budget and spending categorizations, digital receipt recording, payment links, mobile access, and scheduled payments. The “Pro” account adds dedicated pots for tax purposes, integrated accounting, multi-user access, invoicing, virtual cards, and auto-export of transactions. Business accounts are currently only available in the UK.

Source: Y Combinator

Market

Customer

Monzo has attracted young people between the ages of 18-34. They will most likely consider switching from traditional banks and adopting a digital-only bank. Monzo's target users are individuals and businesses looking for digitally native banks. The majority of Monzo's users are in the UK. Users under 34 comprise 72% of Monzo's total user base in 2021. In the US, over half of the users live in urban areas, like Los Angeles, San Francisco, Miami, and Seattle in 2022.

Market Size

The global neobanking market was valued at $66.8 billion in 2022 and is expected to grow at a CAGR of 54.8% from 2023 to 2030. The European neobanking market would grow 45.9% CAGR during 2020-2026. An estimated 400 neobanks worldwide serve one billion clients. By 2025, the UK cohort of digital-only banks will capture more than half of the UK’s digital banking users and almost 40% of UK adults.

Competition

Starling Bank: Starling Bank is a London-based challenger bank founded in 2014. Like Monzo, Starling is a fully regulated UK bank offering individual and business products. Unlike Monzo, Starling Bank does not offer accounts in the US. Starling has raised $1.1 billion to date. In May 2023, it reported customer deposits increased 17% to £10.6 billion, lending amounted to £4.9 billion, and revenue was £453 million for the year in March 2023. Unlike the vast majority of challenger banks worldwide, it is profitable. Like Monzo, it offers personal, joint, and business accounts.

Revolut: Revolut is a neobank founded in 2015. In addition to checking and savings account similar to those offered by Monzo, Revolut offers early and on-demand pay for individuals who want to access a portion of their paycheck in advance and a starter account for users under 18 with supervision by a parent or guardian. Unlike Monzo, it offers investing products like stock trading. Revolut has raised $1.7 billion. As of November 2022, Revolut had over 25 million retail customers worldwide and it said it was expanding its presence across new markets across LATAM, Asia, and the Middle East. Unlike Monzo, Revolut operates in the US.

N26: N26 is a Berlin-based challenger bank company founded in 2013. Like Monzo, it offers personal and business accounts. Unlike Monzo, it offers cryptocurrency trading products. It launched in the US in 2019, partnering with Axos Bank, but in November 2021, it withdrew from the US to focus on Europe. As of January 2023, it had over 7 million users across 24 countries. It has raised $1.7 billion in funding.

Monzo continues competing with incumbent banks like HSBC, Royal Bank of Scotland, and Standard Chartered. The pandemic further entrenched the dominance of Britain’s biggest banks — Barclays, HSBC, NatWest, and Lloyds—the top 4 held over 50% of deposits. They offer many of the same services as neobanks but with a larger and more stable deposit base and often an international customer set. These banks all have physical branch locations, which neobanks don't.

Business Model

Monzo offers its basic accounts for free, with options to receive additional features on accounts for a subscription fee. Monzo also earns interchange, a per-swipe fee charged to merchants who accept credit or debit cards, a portion of which is paid to the bank. Additionally, it earns interest from loans, overdraft protection, and deposits.

Traction

As of May 2023, Monzo had 7.4 million customers, and deposits grew to £6 billion. Monzo generated £440 million in revenue in 2022, an 185% increase for 2021. In May 2023, it disclosed its net operating income was £214.5 million or $266.1 million in the year ending February 2023. The revenue increase was driven by lending, with net interest income increasing 382% to £164.2 million. Monzo’s lending volume reached £759.7 million in May 2023. Lending growth was supplemented by rising usage of overdrafts, personal loans, and the Monzo Flex buy now, pay later service. Monzo had 350K paid accounts as of May 2023.

Valuation

Monzo announced a $500 million round at a $4.5 billion valuation, led by the Abu Dhabi Growth Fund in December 2021. Monzo has raised a total of $1.1 billion in funding from investors like Tencent, General Catalyst, Accel, and Coatue.

For comparison, in 2021, Revolut generated $769 million in revenue, valued at $33 billion. That gave it a ~43x revenue multiple. In 2021, Monzo was valued at $4.5 billion and had a revenue multiple of 24x. In April 2023, an investor in Revolut cut the value of its stake by 46% to $18 billion. That makes its new multiple 23x on 2021 revenues. In 2022, Monzo generated $546 million in revenue. Assuming a 23x multiple based on Revolut's new valuation, Monzo would be valued at or less than its valuation in 2021.

Key Opportunities

Growing Demand for Digital Banking

Increasing digital penetration has already pushed many people towards digital banking, and this trend was further accelerated by the COVID-19 pandemic when bank branches were largely inaccessible. Monzo can use riding this tailwind in the post-pandemic period to extend user growth and adopt new services. Even as the pandemic subsides, multiple studies show consumers plan to continue using digital banking services. And in the UK, where the financial services market remains highly fragmented, Monzo has an opportunity to aggregate demand on its platform by continuing to partner with others and distribute financial products through its app, building toward the company’s ultimate vision of being a financial super app.

Product Expansion

Monzo could benefit from new product offerings similar to those offered by other neobanks, like early wage access, crypto trading and storage, and additional budgeting and financial education services. Monzo has over 250K retail customers who own small businesses but only offers limited business products thus far. A more robust business offering would be one way to grow market share without increasing customer count.

Key Risks

Competition in a Crowded Market

With traditional and challenger banks competing for UK and international consumers, Monzo is operating in a heavily crowded market with incumbents building new products and startups emerging frequently. While Monzo is mitigating some of these threats by positioning itself as a partner to other fintechs who can connect their product to the Monzo app via API to provide consumers an “all-in-one” view of their financial health, this alone may not be enough to allow Monzo to remain competitive. The company must continue to innovate and focus on profitability if it hopes to surpass other UK-focused banks and fintechs.

Regulatory Risks

In 2021 the Financial Conduct Authority (FCA), the UK’s financial watchdog, launched an investigation into Monzo over potential anti-money laundering and financial crime breaches. In that same year, hundreds of Monzo customers complained that their accounts had been frozen or closed without explanation. As a result, Monzo was required to overhaul its financial crime controls and compliance systems. This was a near-detrimental setback for the bank, and any other regulatory issues could put the future success of Monzo in extreme jeopardy.

Slowing Customer Growth

New accounts at Monzo increased just 16% in 2022, compared to 150% in 2020 and 167% in 2019, and business accounts are on a similarly slow growth trajectory. This could be a critical issue for a neobank that relies on acquiring new customers to achieve scale versus traditional banks that generate more revenue per customer through higher fees. Also, because Monzo’s banking license is only for the UK, its geographic expansion is constrained.

Summary

Monzo is a UK-based and fully regulated digital bank offering customers a user-friendly and transparent banking experience. While Monzo positions itself as a socially responsible company that prioritizes its customers over its profits, it has been criticized for its financial performance, as the company has reported significant losses for several years. While Monzo is still the fastest-growing digital bank in the UK, its expansion into the US has been slow and its unclear whether further regulatory scrutiny will hinder its ability to move into new geographical or product areas.