In September 1882, Thomas Edison opened Pearl Street Station in lower Manhattan, a coal-fired plant serving 85 customers within a one-square-mile radius. Prior to Pearl Street, every factory and building that required electricity ran its own generator. Samuel Insull, Edison’s 21-year-old secretary at the time, spent the next four decades consolidating those islands of private power into a national system. By 1932, electricity from Insull’s grid was available in 22 states across 5K cities and towns.

The economics of this early electric grid were simple: a central utility could average demand peaks across thousands of customers and produce power far more cheaply than any individual factory running its own generator. As a result, private generation gradually became uneconomic. The regulatory compact that emerged from this system has governed American electricity ever since: private utility companies get territorial monopolies in exchange for rate regulation and public oversight.

Source: Culture Now

A century after Insull attempted to make private generation obsolete, the economics that supported the formation of the early grid have inverted. Grid connection timelines stretch to seven years in major markets, and permitting has become a decade-long gauntlet.

For AI data centers that stand to generate $10-12 billion per gigawatt annually, this wait has become commercially unsustainable. The response has been a return to the world before Pearl Street, in which companies are once again generating their own power, privately and outside the traditional oversight mechanisms that have governed electricity since the Depression. The 56 gigawatts of announced “behind-the-meter” (BTM) power plant capacity now under construction is the largest reversal of the centralized utility model in US history.

Behind The Meter Buildout

Referred to as the “shadow power grid”, this network of at least 47 off-grid data center power sources is billed by developers as an alternative to drawing on existing grid resources. As of February 2026, this BTM grid accounted for 30% of planned US data center capacity. Nearly 90% of that capacity was announced in 2025 alone, concurrent with overall data center construction slowing relative to 2024, as permitting and grid connectivity barriers became harder to work around. What started as an improvised, potentially temporary workaround has increasingly become a standard development model. BTM systems are expected to meet roughly 25-33% of the additional electricity demand from data centers projected through 2030.

In February 2026, the White House reported that Amazon, Meta, Oracle, xAI, Google, OpenAI, and Microsoft would pledge to supply their own power for data centers. The pledge followed President Trump’s “Ratepayer Protection Pledge,” which called on AI companies to build, bring, or buy all the energy needed for their data centers; this effectively sanctioned the BTM model at the federal level and provided political cover for the state-level regulatory changes that enable it.

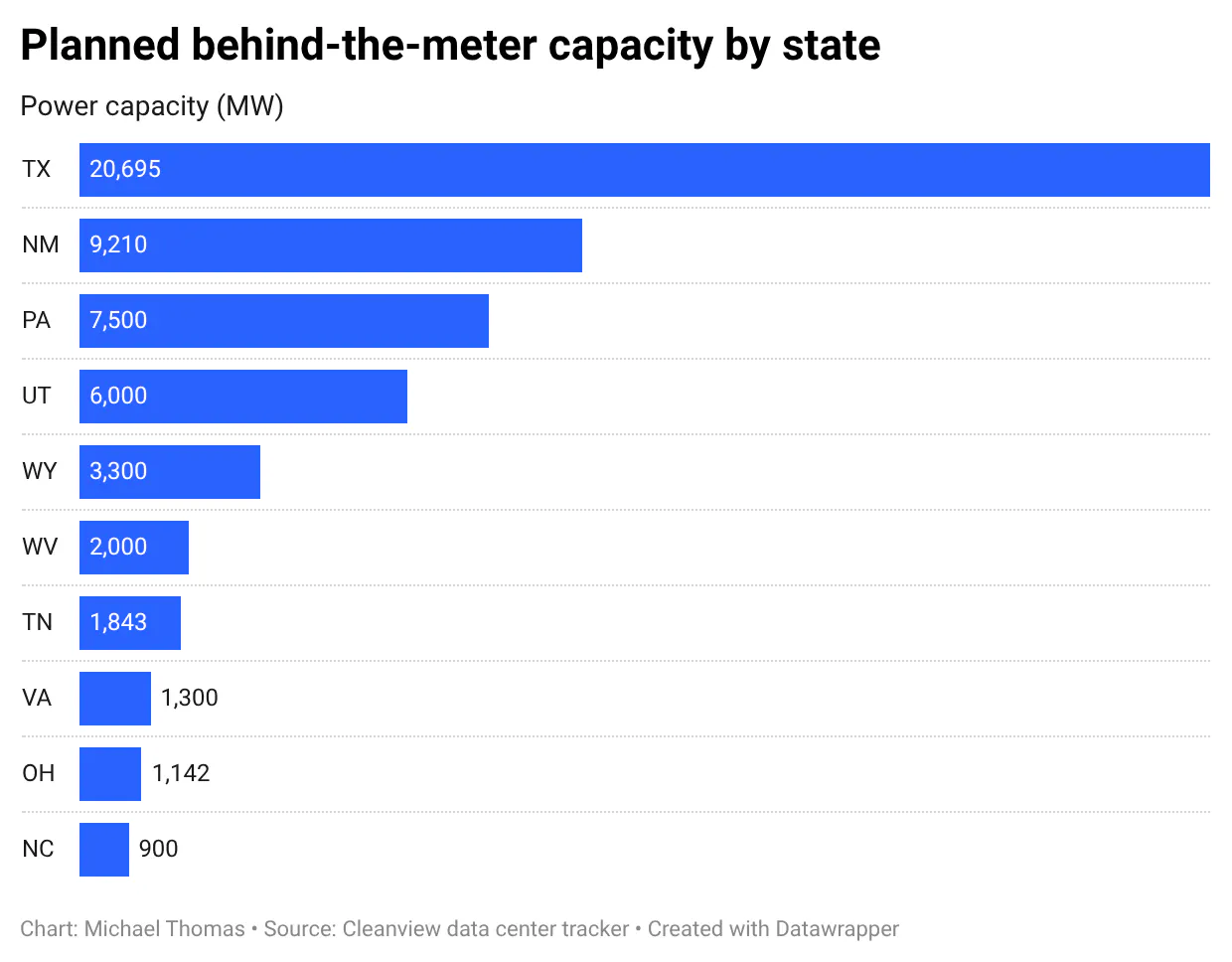

Unlike the data centers developed over the last decade (concentrated in Northern Virginia, the Pacific Northwest, and the Chicago suburbs), this new shadow grid is taking root in states with greater tolerance for private power generation and fossil fuel infrastructure. BTM deployment is extremely concentrated geographically. Five states (Texas, New Mexico, Pennsylvania, Utah, and Wyoming) account for 83% of proposed BTM capacity. Of the 190+ data center bills introduced in state legislatures in the first eleven months of 2025 (nine times the total number proposed in 2024), almost all legislation that actively encourages data center development passed through Republican-controlled chambers.

Source: Cleanview

Inherent in the question of how large this shadow grid will become are the questions of why it is emerging in these particular places, with these particular characteristics. Three forces are independently pushing development toward off-grid solutions and toward a specific set of states: (1) prohibitively long timelines for connecting large loads to existing grids; (2) cost and supply constraints that make natural gas the only fuel deployable at the required speed; and (3) a widening divergence in regulatory frameworks that has made some states easier to build BTM power plants in than others.

Grid-Connection Timelines

The most immediate driver of BTM development is that connecting a large data center to the grid simply takes too long. In high-demand regions like Northern Virginia (historically the largest data center market in the United States), queue times for grid interconnection can stretch up to seven years.

There are two types of grid-connection delays. The first is the straightforward administrative process of interconnecting to a grid with spare capacity, in which a developer submits studies, installs metering, and signs a contract. This can take several months to several years, depending on the jurisdiction and the utility's responsiveness. The second (and more pressing) bottleneck is connection to a grid that does not yet have the generating capacity to support a new load. In this case, the developer must wait not only for interconnection studies but for new transmission infrastructure and new power plants to be planned, permitted, financed, and built.

This bottleneck is geographically asymmetric in ways that explain where BTM development is concentrating. The legacy data center markets (Virginia, the Mid-Atlantic) are served by interstate grids whose interconnection queues have grown steadily for a decade; this is compounded by the retirement of baseload generation and limits on new gas pipeline capacity. For instance, projects that became operational in PJM, the interstate grid serving Virginia, Pennsylvania, and much of the Mid-Atlantic, spent an average of eight years in the interconnection queue in 2025, up from under two years in 2008. Of the 294 gigawatts that PJM studied between 2020 and 2025, 74% ultimately withdrew before reaching commercial operation.

In contrast, Texas’s ERCOT, an independent grid not subject to Federal Energy Regulatory Commission (FERC) jurisdiction, added more generating capacity in 2024 than any other grid in the country. Developers facing the worst grid-connection delays are being disproportionately pushed towards markets like Texas, and the broader interior South, where grids are expanding and permitting is faster.

This push is compounded by the fact that in most high-demand coastal and Mid-Atlantic states, BTM projects still face substantial regulatory friction, including federal environmental permitting requirements and state and local power plant regulations that can subject them to extended review processes. The result is that the same regions that are congested on the grid side are often also restrictive on the private generation side. It is this combination that explains why BTM deployment is not occurring in places like Virginia despite severe grid bottlenecks, but is instead concentrated in Texas and parts of the interior South, where developers can both secure natural gas infrastructure for their BTM power plants and move through permitting processes quickly enough to keep pace with demand growth.

Cost and Equipment

In addition to grid connection times, the equipment needed to build large-scale grid-connected generation is expensive, backordered, and increasingly scarce. This constraint has pushed developers to improvise, sourcing whatever generation equipment can be delivered within months rather than years, and has shaped the fuel mix, technology choices, and geographic footprint of the shadow grid.

Natural Gas: The Dominant Near-Term Fuel

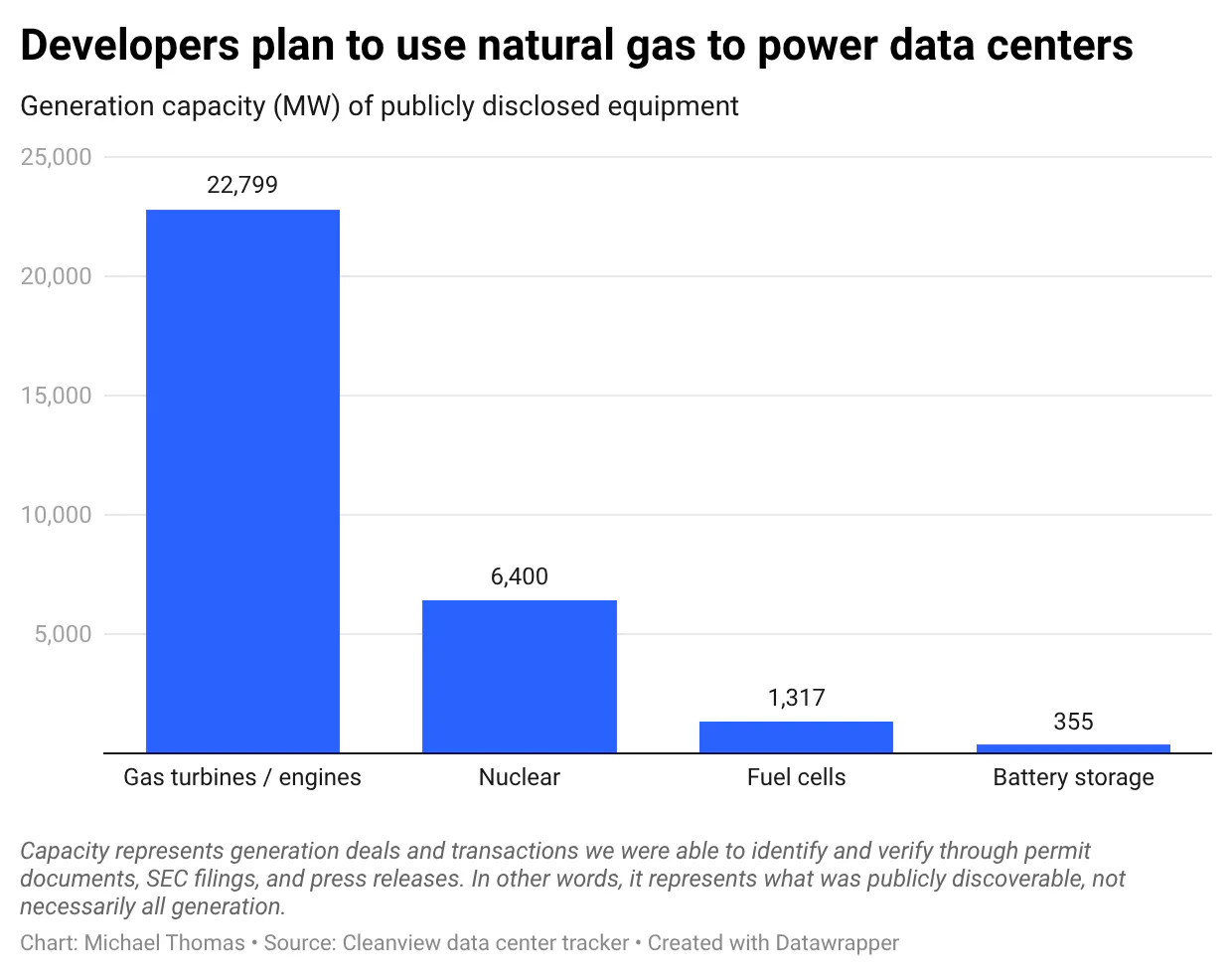

Approximately 75% of the BTM generation capacity that has been publicly identified, roughly 23 gigawatts out of 31 gigawatts, is natural gas-fired. The dominance of natural gas is likely due to its continuity, well-developed infrastructure in key markets, and the ability to source, ship, and commission alternative gas generators on timelines that match data center development schedules.

Source: Cleanview

Because large combined-cycle gas turbines face five to seven-year order backlogs (with two-thirds of gas project developers reporting they do not yet know who will manufacture the turbines their projects require), BTM developers have turned to a range of alternative equipment. Mobile gas generators mounted on semitrucks can be delivered in months and deployed without permanent site infrastructure. Aeroderivative turbines (originally designed for aircraft engines and adapted for power generation) offer higher power density and faster startup than conventional turbines. Reciprocating engines, similar in principle to large diesel generators but running on natural gas, can be deployed in modular arrays and scaled incrementally.

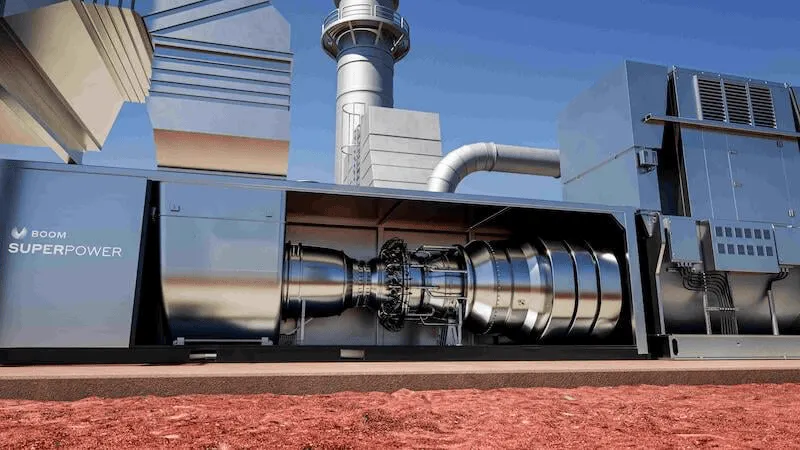

The second Stargate data center in Shackelford County, Texas, a joint venture between OpenAI and Oracle, will deploy 210 industrial gas generators in a fully off-grid microgrid, scaling to 1.4 gigawatts using Austrian Jenbacher reciprocating engines. Meta’s $1.5 billion El Paso facility includes a proposed $473 million, 366 megawatt gas plant featuring 813 modular generators. Similarly, in February 2026, Crusoe placed a $1.25 billion order with Boom Supersonic, a company developing supersonic commercial aircraft, for 29 turbines adapted from its still-in-development aircraft engines.

Source: Boom Supersonic

It is not surprising, then, that the concentration of BTM capacity in five states (Texas, New Mexico, Pennsylvania, Utah, and Wyoming) maps almost exactly onto the geography of major US natural gas production basins. Texas and New Mexico sit on the Permian Basin; Pennsylvania sits on the Marcellus Formation; and Wyoming and Utah provide access to the Rockies’ gas plays. Proximity to wellheads reduces fuel cost and transportation infrastructure requirements, and in some cases enables developers to source gas directly from producers rather than through utility distribution networks.

This geography is reinforced by regulation, since states in traditional energy-producing regions have been more willing to permit new natural gas infrastructure needed to support large-scale BTM generation. States sitting atop major gas basins tend to also be the ones without renewable portfolio standards, carbon pricing, or binding emissions caps, which allows gas to remain the path of least resistance.

Fuel Cells

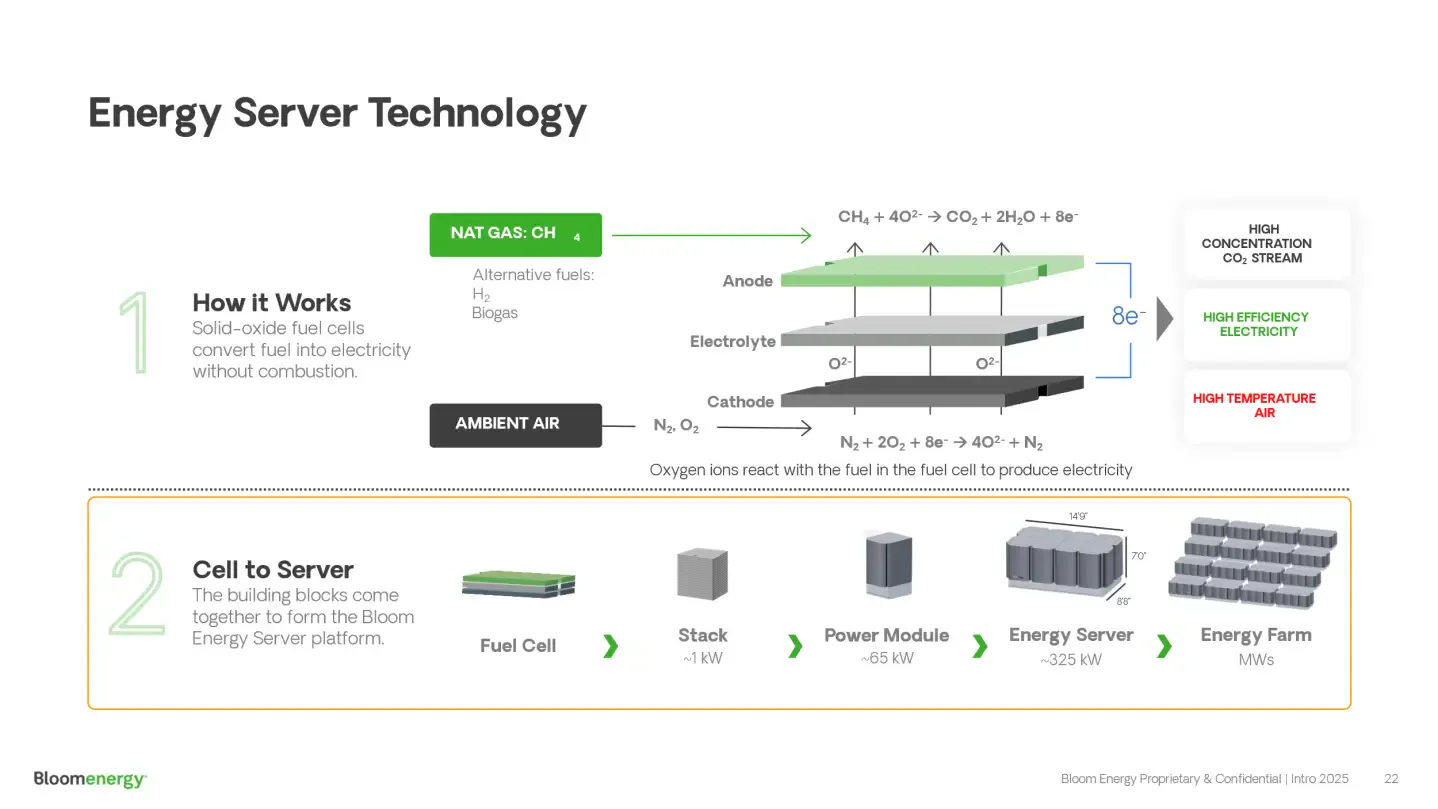

Not all BTM natural gas systems use combustion turbines. An increasing number of projects are deploying solid oxide fuel cells, which convert natural gas to electricity electrochemically rather than through combustion; this produces lower nitrogen oxide emissions and higher efficiency than conventional turbines. Bloom Energy is the leading manufacturer of this technology for data center applications. Bloom’s stock rose approximately 1000% in 2025, driven primarily by data center demand. In 2024, American Electric Power signed an agreement for up to 1 gigawatt of Bloom fuel cells for AI facilities.

Source: Fortune

The appeal of fuel cells (beyond their emissions profile) is that they are not locked into a single fuel source the way a combustion turbine is; a solid oxide fuel cell running on natural gas today could, in theory, be switched to hydrogen or biomethane later using the same hardware. This allows developers to make a near-term capital commitment now while keeping the option to decarbonize later; this is perhaps a meaningful consideration for companies with public net-zero commitments.

Solar

Solar is present in BTM project plans, but almost universally as a future addition rather than a primary power source. Clean energy additions in announced BTM projects are predominantly scheduled for 2028 or later, meaning the near-term build-out is dominated by fossil fuels. The practical constraint with solar energy is its inherent intermittency; data centers require continuous power, and solar generation alone cannot guarantee this uptime without some form of energy storage. Large battery storage systems could address this gap, but likely at a cost and footprint that make solar-plus-storage more expensive per kilowatt-hour delivered than gas generation at current prices.

The solar projects that do appear in BTM plans tend to play a supportive role (cutting daytime grid usage, hedging against gas price swings, or helping meet corporate sustainability targets) rather than replacing baseload generation. Microsoft, Google, and Amazon have all announced solar additions to their data center campuses, but these installations typically cover only a portion of total demand.

Geographically, large-scale solar installations require large, flat areas with strong sunlight. These conditions are typically found in the Southwest, but not always in the same places where natural gas production (and most BTM projects) are concentrated.

Nuclear: Small Modular Reactors

Small modular reactors (SMRs) are the most discussed long-term alternative to gas-fired BTM generation. This is because nuclear power is continuous, carbon-free, and produces enormous amounts of energy from a site small enough to sit alongside a data center campus. Companies developing data centers (including Google, Amazon, and Microsoft) have signed agreements with SMR developers like Kairos Power, X-energy, and Oklo.

However, the deployment timeline of SMRs makes it largely irrelevant to the current shadow grid buildout. No commercial SMR has yet entered operation in the US. Regulatory approval from the Nuclear Regulatory Commission for first-of-its-kind designs can take years, and nuclear construction timelines have historically run well beyond initial estimates even after approval. The most optimistic projections for commercial SMR availability in the US are in the early to mid-2030s. In this respect, SMRs are best considered a bet against long-term gas dependence rather than a near-term solution to the current power constraint.

Battery Storage

Battery storage systems are increasingly deployed alongside BTM generation, though they function differently from the primary generation sources. At data center sites, batteries primarily serve to (1) provide backup power during generator startups or maintenance windows, (2) smooth out short-term fluctuations in generation output, and (3) enable peak shaving that reduces demand charges for sites that maintain some grid connection.

Texas is the fastest-growing battery storage market in the United States, driven in part by ERCOT’s market structure, which pays battery storage owners for providing grid-stabilizing services. Several data center sites in Texas have paired large battery arrays with gas generation, creating hybrid systems that can sustain operations during brief outages without relying on the grid. As battery costs continue to decline, the economics of storage-heavy BTM systems will improve, but they are not yet competitive with gas as a primary generation source at the scale these facilities require.

Geothermal

Geothermal is perhaps the only clean, fully dispatchable power source with a credible BTM timeline before SMRs arrive. Traditional geothermal energy has been geographically limited to places where the earth’s heat vents naturally to the surface, including Iceland and parts of California and Nevada, but enhanced geothermal systems (EGS) borrow horizontal drilling and hydraulic fracturing techniques from the oil and gas industry to engineer heat exchangers in hot dry rock. This makes the resource accessible almost anywhere. Underground temperatures rise roughly 25-30°C per kilometer of depth. Drills deep enough with wells bent laterally through hot rock provide a subsurface power source that runs 24/7 regardless of weather.

EGS is predicted to economically meet up to 64% of expected data center demand growth by the early 2030s. In 2025, Google signed a 115 megawatt PPA with Fervo Energy and participated in its $462 million Series E. Geothermal also enjoys the rare distinction of bipartisan political support, and the One Big Beautiful Bill Act spared geothermal tax credits while cutting incentives for wind and solar.

However, geothermal drilling is still expensive relative to gas, first-of-kind project risk remains high, and the technology is currently most viable in the western US where hot rock sits closer to the surface. Reaching equivalent temperatures in Pennsylvania or West Virginia requires drilling considerably deeper, which pushes up cost. Geothermal also shares its workforce and supply chain with the oil and gas industry, which matters in the same interior states where BTM development is concentrating.

Regulation and Public Opposition

BTM generation occupies an unusual regulatory position because it serves a single on-site customer rather than selling power into the wholesale market. This means it largely falls outside FERC’s federal jurisdiction and is instead governed by a patchwork of state and local rules. The core problem with regulating BTM is that most state utility laws were written either for traditional utilities or for small rooftop solar installations (not hundred-megawatt private power plants serving a single customer). Without clear rules, it is unclear at what point generating one’s own power crosses the line into operating an illegal utility. Data center customers must resolve this question through case-by-case commission proceedings and uncertain timelines, which could cost years and millions of dollars in added costs.

Supportive Policy

The states capturing the BTM buildout are the ones that have resolved these ambiguities more proactively. Utah’s SB 132, for example, is the most complete BTM framework in the country. It defines any customer drawing over 100 megawatts as a special category of large-load customer, and creates a parallel category for the companies that build and operate power plants to serve them. This explicitly exempts both from the public utility regulations that would otherwise apply. A data center in Utah can contract with any one of these providers to build a fully private power plant that covers its electricity needs without needing to touch the public grid. The law also requires that any costs the data center imposes on the broader grid infrastructure (e.g., through backup capacity if their private generation goes offline) be paid by the data center itself rather than ratepayers.

Ohio’s HB 15 also gets partway there, allowing large customers to build their own private power systems without being classified as a public utility. Without that protection, a company generating its own power could be accused of violating the local utility’s legal monopoly on selling electricity in that area. The law does, however, still have two gaps. First, it only covers power plants built directly on the customer’s own property; if a developer wants to build a generator on a neighboring parcel and run a private cable to the data center next door, it’s unclear whether that arrangement gets the same legal protections. Second, Ohio has no streamlined permitting process for connecting these large power plants to the grid; developers have to use the same procedures designed for small rooftop solar installations.

Additionally, BTM-supportive states have moved to concentrate permitting authority at the state level and remove local governments’ ability to block projects. For example, West Virginia’s HB 2014 eliminated county and municipal zoning, inspection, and code enforcement authority over data centers entirely.

Regulatory Frictions

By contrast, in coastal and legacy data center markets, local governments remain the primary locus of discretionary control. Loudoun County, for instance, ended by-right zoning for data centers in March 2025, and Atlanta required special use permits in 2024. The practical consequence is that in states actively encouraging BTM development, a developer gets a predictable yes; in coastal markets, the outcome depends entirely on which community they're building in.

This asymmetry is compounded by public opinion, which itself reflects underlying economic conditions across states. A higher share of Republicans and Republican-leaning independents trust the US to regulate AI (54%) than Democrats and Democratic-leaning independents (36%). In practice, this may translate into greater political tolerance in many red-state jurisdictions for rapid infrastructure buildout.

That tolerance is reinforced by longer-run economic conditions that shape how such projects are perceived at the local level. 71% of US counties saw manufacturing employment fall between 2001 and 2015, and rural areas lost population in absolute terms for the first time in recorded history between 2010 and 2016. For communities on that trajectory, a major data center campus represents one of the few large-scale capital investments on the horizon. In communities where fossil fuel extraction has historically been the primary economic driver, concerns about the tradeoffs associated with data centers are unlikely to generate meaningful political resistance.

Source: Latitude Media

What Comes Next

The cumulative effect of these three drivers (grid interconnection constraints, fuel availability, and regulatory permissiveness) is a geography of AI infrastructure that maps with striking precision onto the political map of the United States. Red states are essentially reprising their historical role as resource colonies in the AI economy, trading natural gas, land, and regulatory permissiveness for capital investment that may inadvertently lock them into dependence on AI infrastructure spending.

There is an inherent long-term vulnerability in this model. States that restructure their regulatory frameworks, strip local governments of permitting authority, and provide extensive tax abatements to attract data center investment are making a long-term bet on the continued growth of AI infrastructure spending. If that spending slows, or the economics of BTM generation change, or federal policy makes gas-fired data centers more expensive to operate, then the same jurisdictions that encouraged rapid BTM deployment may be left with underutilized infrastructure and not much to show for the concessions they made.

The more optimistic read, however, is that the fossil-fueled shadow grid is a genuinely transitional bridge to SMRs and next-generation solar. The compute colonies taking shape in Texas, New Mexico, and Wyoming may simply be where a new energy infrastructure starts (one that begins with gas because gas is what’s available), but then migrates toward cleaner sources as the technology matures. Whether that turns out to be true depends entirely on whether the long-term technology bets pay off.

In 1932, Insull’s empire collapsed, wiping out $800 million and the savings of 600K shareholders. What failed was a financial structure built on the assumption of perpetual demand, which concentrated the downside risk in the hands of the people least able to absorb it, while profits flowed elsewhere. The communities now hosting the shadow grid are making a version of the same bet, and the answer to whether they’ve made it wisely won’t be clear until long after the infrastructure is built.