Thesis

For decades, space systems have served as core infrastructure for global telecommunications and national security. Geostationary (GEO) satellites historically anchored television and radio broadcasting, while low Earth orbit (LEO) constellations have grown into a primary vehicle for global broadband through systems such as Starlink and Amazon’s Kuiper. In parallel, LEO satellites play a critical role in defense and security by enabling earth observation and providing resilient communications in conflict zones.

Since 2010, the inaugural flight of the Falcon 9 rocket, SpaceX has reduced both the cost and friction of access to orbit by an order of magnitude, serving as a major catalyst for the space industry. In 2021, SpaceX introduced rideshare launches, allowing customers to purchase capacity on a shared launch rather than procure an entire rocket. Compared to dedicated small-satellite launches in the early 2010s, rideshare reduced per-satellite launch costs by more than an order of magnitude. For startups, research institutions, and commercial operators, in-orbit testing was no longer financially out of reach, unlocking applications that were previously economically infeasible.

Despite these advances in launch, satellite manufacturing remained a structural bottleneck. Legacy manufacturers frequently missed delivery schedules and imposed cost overruns that undermined customer business models. Historical data from 2009 to 2016 showed that less than 57% of small satellite missions were successful, highlighting a critical gap in satellite reliability. More recent data confirmed the gap persisted: as of 2024, 6% of all launched CubeSats were never heard from at all (e.g., dead on arrival), with a much larger share failing to complete mission objectives. Beyond reliability, the historical practice of developing proprietary satellite buses no longer constituted a durable competitive advantage, as launch standardization and falling rideshare costs decoupled satellite differentiation from custom hardware design and shifted it toward execution speed, reliability, and cost control.

The small satellite manufacturing market has also undergone significant consolidation over the past decade. A handful of small satellite manufacturers have been acquired by large defense primes and now primarily serve their parent companies’ government customers. This consolidation has left a meaningful portion of the commercial market underserved, particularly private operators and programs requiring lower volumes and rapid iteration.

Apex addresses this manufacturing bottleneck by producing standardized satellite bus platforms at industrial scale. Rather than engineering each bus from scratch to a customer’s specifications, Apex offers a small set of pre-engineered configurations that can be delivered in months rather than years. By concentrating engineering effort on a productized, repeatable bus rather than custom programs, Apex compresses the throughput constraint that has limited the small satellite market.

Founding Story

Apex was founded in 2022 by long-time friends Ian Cinnamon (CEO) and Max Benassi (CTO). The company was founded based on Cinnamon’s and Benassi’s firsthand operational experience within the defense and aerospace industries.

Cinnamon brings experience scaling venture-backed technology companies and navigating the defense industrial base. He holds a B.S. from MIT and an MBA from Stanford GSB. After Y Combinator, he co-founded Superlabs, which was acquired by Zynga in 2014.

In 2016, Cinnamon co-founded Synapse Technology Corporation. Synapse developed computer-vision systems for automated X-ray security and was acquired by Palantir in 2020. Following the acquisition, Cinnamon worked in Palantir’s Aerospace and AI business development group, where he observed that government and defense customers faced long, expensive development cycles driven by bespoke satellite programs.

Benassi contributes aerospace hardware and manufacturing expertise. He spent more than six years at SpaceX as a senior propulsion engineer, working across Falcon 9, Falcon Heavy, and Starlink, and later served as Engineering Director at Astra, where he gained further insight into the evolving unit economics of space systems. Apex’s industrialization thesis is anchored in Benassi’s view that, having seen SpaceX commoditize launch, satellite manufacturing is the next major scalability bottleneck in the space value chain.

In terms of notable hires, the company brought on board Adam Corey as Chief Business Officer in June 2023. Corey was previously co-founder and managing partner of Village Global.

Product

Apex produces standardized satellite bus platforms. A satellite bus is the main structural body of a satellite, providing power, thermal control, and navigation necessary for the mission payload to operate. Each platform Apex produces comes with pre-engineered configuration packages to service a range of missions.

Apex’s value proposition runs along two dimensions: time-to-orbit, where Apex can deliver a bus in as little as six months and enable a full mission launch in under a year; and procurement velocity, where Apex was the first US small-sat manufacturer to implement transparent, web-based pricing, removing the opaque negotiation cycles typical of the satellite industry. Apex segments its offerings by payload capacity, power output, and orbital destination. Each platform is designed to be compatible with the SpaceX Transporter (Rideshare) missions.

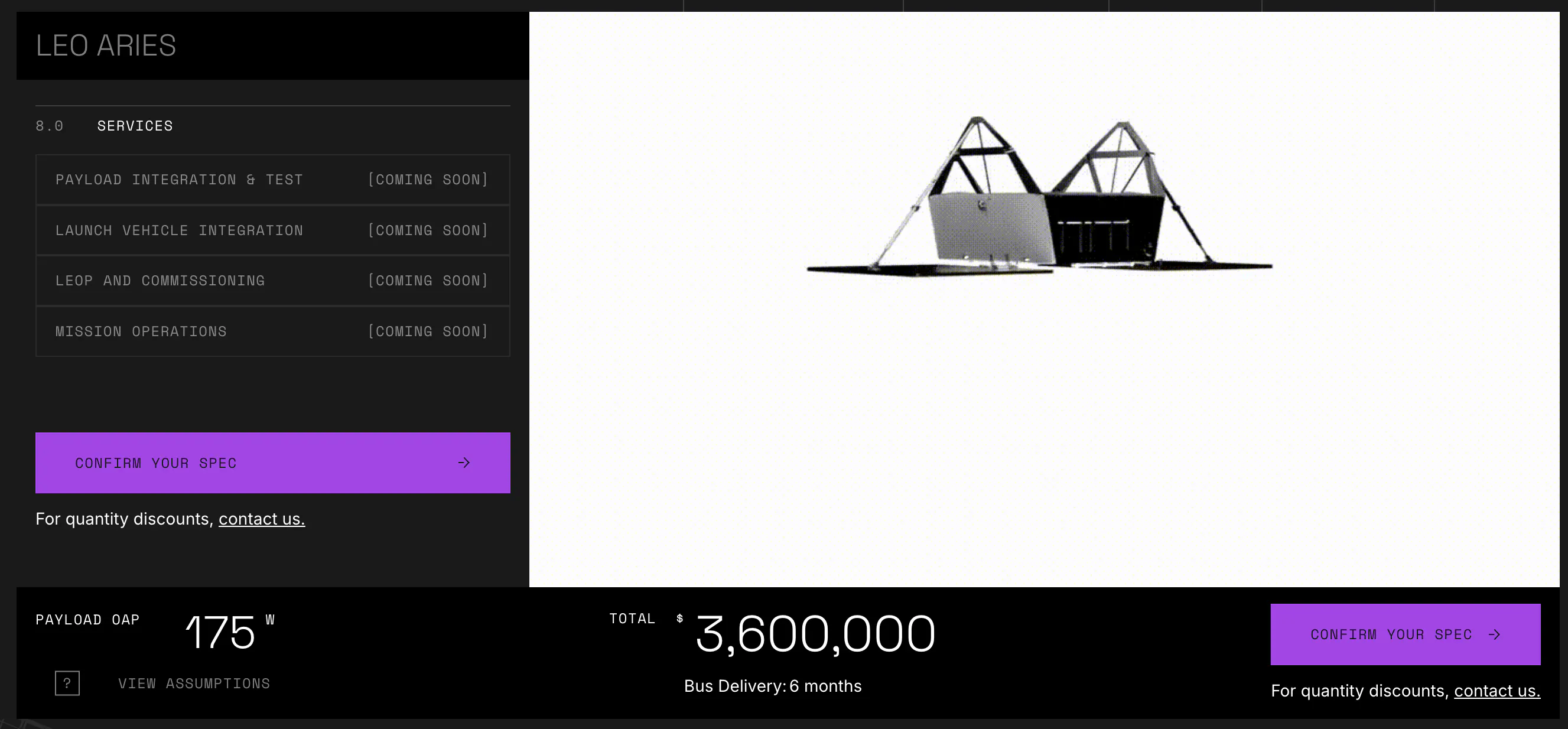

Aries

Source: Apex

Aries is Apex’s flagship and most mature product, specifically engineered for the “Full Plate” configuration of a SpaceX Rideshare mission. Aries’ main uses are earth observation applications and low-data-rate communications (such as Internet of Things connectivity). It provides a critical solution for startups and government agencies that cannot wait several years for a custom bus. The LEO platform features a 125 kg bus weight supporting up to 150 kg of payload at 175 W of Orbit Average Power (OAP). Base pricing ranges from $3.5 million to $5.7 million, excluding launch costs.

In March 2024, Apex launched Aries SN1, providing the company with essential flight heritage. As of March 2025, the satellite had been operational in orbit for over a year. SN1 hosted sensitive payloads for multiple defense customers, including an edge-processing payload for Anduril and a payload for Booz Allen Hamilton.

GEO Aries

Source: Apex

GEO Aries is a radiation-hardened variant of the Aries bus designed for geostationary orbit (36K km). At $13.5 million and a 15-month lead time, it allows customers to deploy smaller payloads (up to 120 kg) to GEO at a fraction of the cost of traditional telecommunications satellites. The first in-orbit demonstration was scheduled for late 2026.

Nova

Source: Apex

The Nova platform is designed for missions requiring greater mass and power without sacrificing the productized delivery model. Nova targets advanced remote sensing, telecommunications, and high-stakes security applications such as space-based interceptors. The platform supports a 300 kg payload capacity with 1 kW of OAP and agile propulsion for precise maneuvering. The base configuration starts at $6 million, with an in-orbit demonstration scheduled for 2026.

Comet

Source: Apex

Comet is a high-power, flat-packed bus optimized for mass-launch efficiency. Its flat form factor allows for maximum density within a rocket fairing, mirroring the design philosophy popularized by Starlink. Comet is intended for power-hungry missions such as Direct-to-Device (D2D) telecom and Synthetic Aperture Radar (SAR). It supports between 450 and 3K kg payloads, depending on the variation, with 6 kW of OAP. Pricing has not yet been disclosed but is expected to land in the single-digit millions, with a 24-month lead time. The first in-orbit demonstration was on the roadmap for 2028.

Service Ecosystem

Beyond hardware, Apex offers a standardized package of mission services. This includes physical mating of the customer payload to the bus, environmental testing, and managing the “last mile” logistics with the launch provider. Apex also provides mission operations to manage the satellite’s health and telemetry during its five-to-seven-year operational lifespan.

Market

Customer

Apex targets a diverse set of operators requiring rapid satellite deployment for remote sensing, telecommunications, and national security missions. The core value proposition across all segments is the compression of the traditional satellite procurement cycle, enabling customers to move from design to orbit on a timeline previously unattainable in the aerospace sector.

In-Orbit Demonstration & Rapid Validation. The Aries platform serves as the primary vehicle for in-orbit demonstrators, targeting startups, research laboratories, and emerging defense primes where speed of validation is the critical metric. This segment typically involves low-volume orders of one to two units, allowing customers to bypass the multi-year research and development phases associated with bespoke bus architecture. Apex manages the end-to-end integration, launch, and on-orbit commissioning, providing a turnkey solution for companies like Aetherflux, a space-based solar power startup, to test prototype payloads in live environments.

Defense & National Security. As of 2025, national security represented approximately two-thirds of Apex’s revenue stream, driven by a shift in US defense doctrine toward proliferated architectures. Apex operates through a dual distribution channel: as a satellite supplier to major primes and as a direct contractor for the Department of Defense. Apex is also expanding its international defense footprint through strategic partnerships, including with the Hungarian manufacturer Remred to penetrate the European market. In March 2026, Apex announced its first deal with a Japanese customer: NEC Corporation purchased an Aries bus to support a 2027 high-throughput optical communications technology demonstration mission.

Telecommunications & Global Constellations. The Comet satellite bus is designed to serve the emerging direct-to-device 5G market, which requires large constellations typically ranging from 200 to 1K satellites. While this remained an early-stage opportunity for Apex with manufacturing capacity still scaling and Comet yet to establish flight heritage, its architecture is explicitly optimized for industrial-scale production. This segment represents Apex’s primary long-term growth vector, characterized by high-volume manufacturing programs and potential contract values in the multi-billion-dollar range.

The US space industrial base is transitioning from legacy cost-plus satellite procurement to high-velocity, industrial-style acquisition. For decades, the Department of Defense relied on bespoke satellite programs characterized by decade-long development cycles and cost-plus contracts that emphasized technical novelty over manufacturability and cost control. This model limited competition and constrained production scale.

The Space Development Agency (SDA) has reshaped this dynamic. By institutionalizing an acquisition framework based on fixed-price contracts and recurring satellite tranches every 24 months, with unit prices typically landing in the low double-digit millions per spacecraft, the SDA reintroduced price discipline and industrial competition. This approach provides predictable demand, regular contract cadence, and long-term planning visibility, enabling manufacturers to invest in production capacity and supply-chain optimization. As a result, emerging satellite integrators such as Apex are positioning themselves as high-velocity Tier 2 suppliers (specialized component manufacturers selling into the prime contractors) to traditional defense primes.

In parallel, Apex maintained direct engagement with the US Space Force, a strategic priority following the 2025 unveiling of the Golden Dome initiative, the largest near-term demand catalyst for the US satellite manufacturing base, which is treated in detail under Key Opportunities below.

Market Size

Apex operates in the global satellite manufacturing market, which is shifting from low-volume, bespoke engineering toward standardized, industrial-scale production. This transition is driven by the rise of large, proliferated constellations, where procurement is dictated by manufacturing throughput, unit economics, and delivery reliability rather than mission-specific customization. These dynamics apply across both commercial and defense customers.

Globally, as of 2025, the satellite manufacturing market represented approximately $50 billion to $60 billion per year, including activity in China and Russia. Small satellites accounted for roughly 40% of this total, implying an addressable market of approximately $20 billion in 2025.

The majority of global demand is concentrated in telecommunications. By active-satellite share as of July 2024, Starlink alone accounted for roughly 60% of all operational LEO satellites, and SpaceX vertically integrates this production internally, making this portion of the market effectively inaccessible to third-party manufacturers. As a result, commercial demand outside of Starlink was relatively stable with limited near-term growth, sized at roughly $8 billion as of 2025. Incremental market expansion is more likely to come from defense and national security programs, such as Golden Dome, although the scale and timing of this demand have not yet been fully defined.

Competition

Competitive Landscape

The small satellite manufacturing sector has historically been dominated by incumbent defense prime contractors that act as system integrators and hold the primary contracts with end customers. Within this structure, smaller satellite manufacturers typically operate as subcontractors to the primes or receive limited standalone awards, often restricted to one or two units intended to demonstrate specific technologies rather than support scaled production.

Competitive activity is concentrated around a small set of US primes: Lockheed Martin, Northrop Grumman, and RTX (Raytheon), with newer vertically integrated entrants such as Rocket Lab and Sierra Space. The most direct competitive pressure on Apex comes from agile satellite manufacturers that have been acquired by large defense primes, such as Terran Orbital or Blue Canyon Technologies. These hybrid organizations combine startup-level execution speed with the capital resources, contracting access, and institutional credibility of their parent companies.

Apex differentiates primarily on speed of execution. Incumbent primes are structurally constrained by legacy processes and compliance overhead and cannot match high-velocity delivery timelines. Apex can deliver satellites to orbit in under 12 months, which constitutes its core competitive advantage as defense and commercial customers push back against historically slow procurement cycles.

This emphasis on speed is shared by other venture-backed players, such as Loft Orbital and Muon Space, each operating within a defined niche. Apex does not yet possess a durable long-term moat: companies pursuing similar high-velocity strategies have historically been acquired by large defense primes rather than remaining independent.

Competitors

York Space Systems: York, founded in 2012, is a designer and manufacturer of standardized spacecraft bus platforms with a primary focus on US government and defense customers. The company was one of the few non-prime contractors to secure a meaningful contract with the SDA, notably delivering spacecraft for Tranche 1 of the Proliferated Warfighter Space Architecture (PWSA). York successfully manufactured and shipped 21 of the 42 satellites awarded to it for the Tranche 1 transport layer, demonstrating its ability to execute at scale within the SDA’s fixed-price, high-cadence procurement model.

In 2022, AE Industrial Partners acquired a majority stake in York, one of the rare private-equity-led transactions in the satellite manufacturing sector. In January 2026, York completed an initial public offering, raising approximately $630 million. York reported $253 million in 2024 revenue, with more than 95% derived from defense customers. York’s business model closely parallels Apex’s emphasis on standardized buses and repeatable manufacturing; the primary difference is the breadth of customer mix: York is a near-pure-play defense supplier, whereas Apex pursues a broader strategy that spans defense and commercial contracts.

Terran Orbital (acquired by Lockheed Martin): Terran Orbital, founded in 2013, was a pioneer in the venture-backed satellite manufacturing sector, specializing in mass production of standardized satellite platforms ranging from nanosatellites to large smallsats. Prior to its acquisition, Terran Orbital had raised approximately $300 million in private capital, in addition to public market funding following its 2022 SPAC-merger listing. In 2024, Terran Orbital was acquired by Lockheed Martin for approximately $450 million, bringing the company under the control of one of the largest US defense primes.

The acquisition price represented a material discount relative to Terran Orbital’s prior private-market peak. Its product strategy and industrial ambition were closely aligned with Apex’s positioning as of May 2026, particularly the emphasis on standardized satellite buses and high-rate production. Its outcome shows a key structural risk: venture-backed satellite manufacturers pursuing similar go-to-market strategies have historically struggled to remain independent and have ultimately exited via acquisition at valuations below prior private-market marks.

Loft Orbital: Loft Orbital, founded in 2017, operates a satellite-as-a-service model and primarily acts as a systems integrator, sourcing satellite buses from partners such as Airbus rather than manufacturing them in-house. The company refurbishes and integrates satellites to host customer payloads on accelerated timelines, typically delivering missions in under one year. Its core offering is a multi-payload colocation model, in which several customers share a single satellite and split mission costs, allowing faster access to orbit without full satellite ownership. In 2025, Loft Orbital raised a $170 million Series C led by Tikehau, bringing total funding to approximately $325 million, with notable investors including BlackRock and Temasek.

Commercial traction includes approximately $500 million in lifetime bookings, anchored by a large constellation contract with EarthDaily and additional contracts with the SDA. Internationally, Loft Orbital has expanded into the UAE through a joint venture with Marlan Space. Loft Orbital’s value proposition overlaps significantly with Apex’s, with speed to orbit as the primary differentiator, but the underlying business models diverge: Apex builds and sells the bus; Loft buys and integrates buses from third parties.

Muon Space: Muon Space, founded in 2021, is a space systems company that designs, manufactures, and operates LEO satellite constellations focused on earth intelligence and remote sensing missions. The company delivers end-to-end systems, combining satellite hardware, mission design, and on-orbit operations, with an emphasis on standardized platforms optimized for rapid deployment. In 2025, Muon Space raised a $146 million Series B led by Congruent Ventures, bringing total capital raised to approximately $225 million. Its investor base includes Activate Capital, Acme Capital, Costanoa Ventures, and Radical Ventures.

While Muon Space’s primary market is earth observation, the company competes directly with Apex in US Space Force and defense-related programs, particularly missions involving intelligence-focused payloads. In a meaningful technical differentiation, Muon signed an agreement with SpaceX in 2026 for Starlink mini laser terminals, with Q3 2026 integration enabling persistent optical inter-satellite connectivity in orbit, a capability Apex did not currently offer as of May 2026.

Business Model

Apex generates revenue through the direct sale of satellite hardware and a standardized package of associated mission services. The core of the business model is the productization of the satellite bus, moving away from the industry’s legacy cost-plus artisanal model to prioritize speed of execution and unit-cost reduction.

Source: Apex Configurator

The Three Pillars of Industrialization

To achieve Henry-Ford-style mass production in orbit, Apex utilizes three strategic levers.

First, the company relies on extreme standardization. Unlike legacy primes that perform extensive redesigns for every client, Apex utilizes a single development cycle for all customers. By eliminating non-recurring engineering for individual orders, the company reduces R&D overhead and prevents the expansion of engineering teams. Customization is only entertained for large-scale constellation orders or major Space Force contracts where the volume justifies the technical deviation.

Second, Apex secures its production timeline through carefully planned supply chain management and vertical integration. To mitigate the bottleneck of long-lead items, Apex employs a dual-sourcing strategy complemented by internal development of select propulsion and avionics subsystems.

Third, the operational strategy centers on Factory One, a facility designed to mirror the high-rate assembly lines of the automotive industry. Apex is scaling this infrastructure to achieve a target production capacity of over 200 satellites per year. This shift toward automated, high-throughput manufacturing allows the company to amortize fixed facility costs across a high volume of standardized units.

The primary competitive advantage for Apex is its speed of satellite delivery. While traditional satellite procurement often spans years, Apex delivers hardware in months. This speed-to-orbit is the company’s defining value proposition.

Traction

Apex reported $60 million in revenue in 2025, supported by over $100 million in contracted bookings. As of 2025, the company served approximately 12 major customers, with roughly two-thirds of revenue derived from defense-related programs.

A major inflection point occurred in February 2025, when Apex was awarded a $45.9 million direct contract by the US Space Force. The contract covers the delivery of multiple satellite vehicles across several orbital regimes, with program execution and performance obligations extending through 2032.

In parallel with direct government contracts, Apex has deepened existing relationships with leading defense and aerospace primes. Building on the 2024 SN1 in-orbit validation, Apex’s partnership with Anduril now positions Apex satellite buses as a preferred hardware platform within the Lattice Defense Ecosystem. Additional named customers include BAE Systems, reinforcing Apex’s role as a core supplier for proliferated government satellite constellations.

Production cadence is also accelerating: Apex delivered three additional Aries buses to customers in Q1 2025 alone.

As of 2025, Apex was scaling its manufacturing operations. A key use of proceeds from the Series D financing is the expansion of Factory One, specifically a 55K sq ft new facility adjacent to the existing Playa Vista site, bringing total manufacturing footprint to over 100K sq ft and targeting a 50% production increase, with move-in during 2026. The expansion is intended to support execution against the existing backlog and anticipated future demand.

Valuation

In September 2025, Apex raised a $200 million Series D led by Interlagos, which valued the company at over $1 billion. As part of this round, Tom Ochinero, founding partner at Interlagos and former Senior VP at SpaceX, joined the Apex board. The Series D brought Apex’s total funding to approximately $518.5 million across all disclosed rounds, with major investors including Interlagos, Point72 Ventures, 8VC, and Andreessen Horowitz.

The Series D followed a $200 million Series C in April 2025, led by Point72 Ventures and co-led by 8VC. Ten months before that, in June 2024, Apex had raised a $95 million Series B led by XYZ Ventures and Charles River Ventures. The Series B was preceded by a $16 million Series A in April 2023 led by XYZ Ventures, and a $7.5 million seed round in October 2022 led by Andreessen Horowitz. Round-specific valuations for the Series A, B, and C were not publicly disclosed at the time of each announcement.

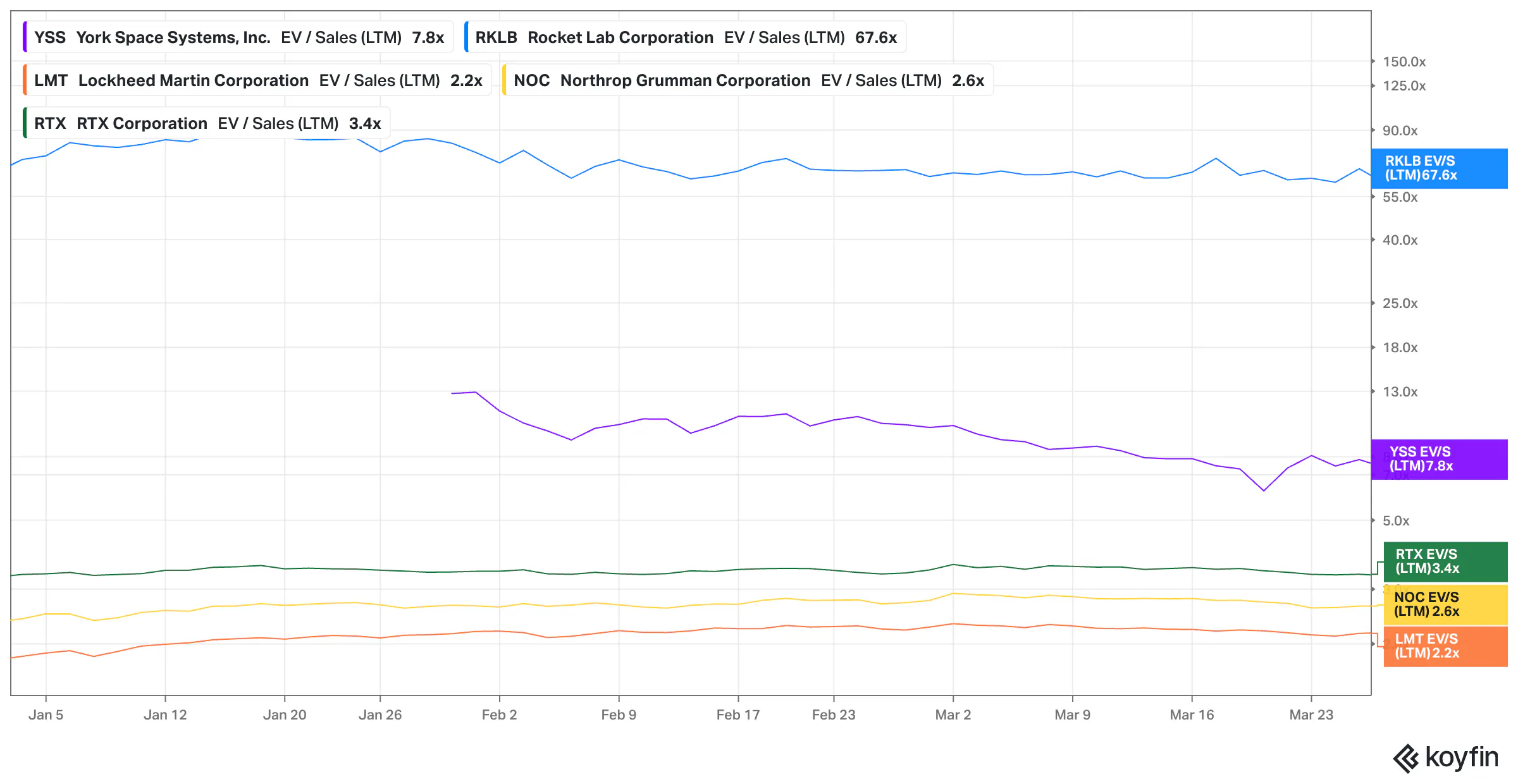

One primary public benchmark for Apex is York Space Systems, a direct competitor that completed an IPO in January 2026 at a debut valuation of approximately $4.8 billion. After an early dip in which York hit a 52-week low of approximately $16.93 per share in the weeks following the IPO, the stock recovered.

As of May 2026, York traded around $33 per share with a market capitalization of approximately $4.3 billion, within roughly 2% of its IPO debut. York reported $386 million in 2025 revenue (up roughly 52% year-over-year from $253 million in 2024) and management guided to $545 million to $595 million for 2026. On 2025 actuals, York traded at a revenue multiple of approximately 12x, or approximately 8x on the midpoint of 2026 guidance as of May 2026.

Source: Koyfin

York traded above traditional prime contractors, which typically commanded 2-3x revenue multiples, but well below vertically integrated players such as Rocket Lab, which traded at approximately 63x. York’s recovery from the post-IPO dip read as a positive signal for Apex: the public market, on net, validated a high-throughput, defense-anchored small-satellite manufacturer at a multiple meaningfully above legacy primes.

Key Opportunities

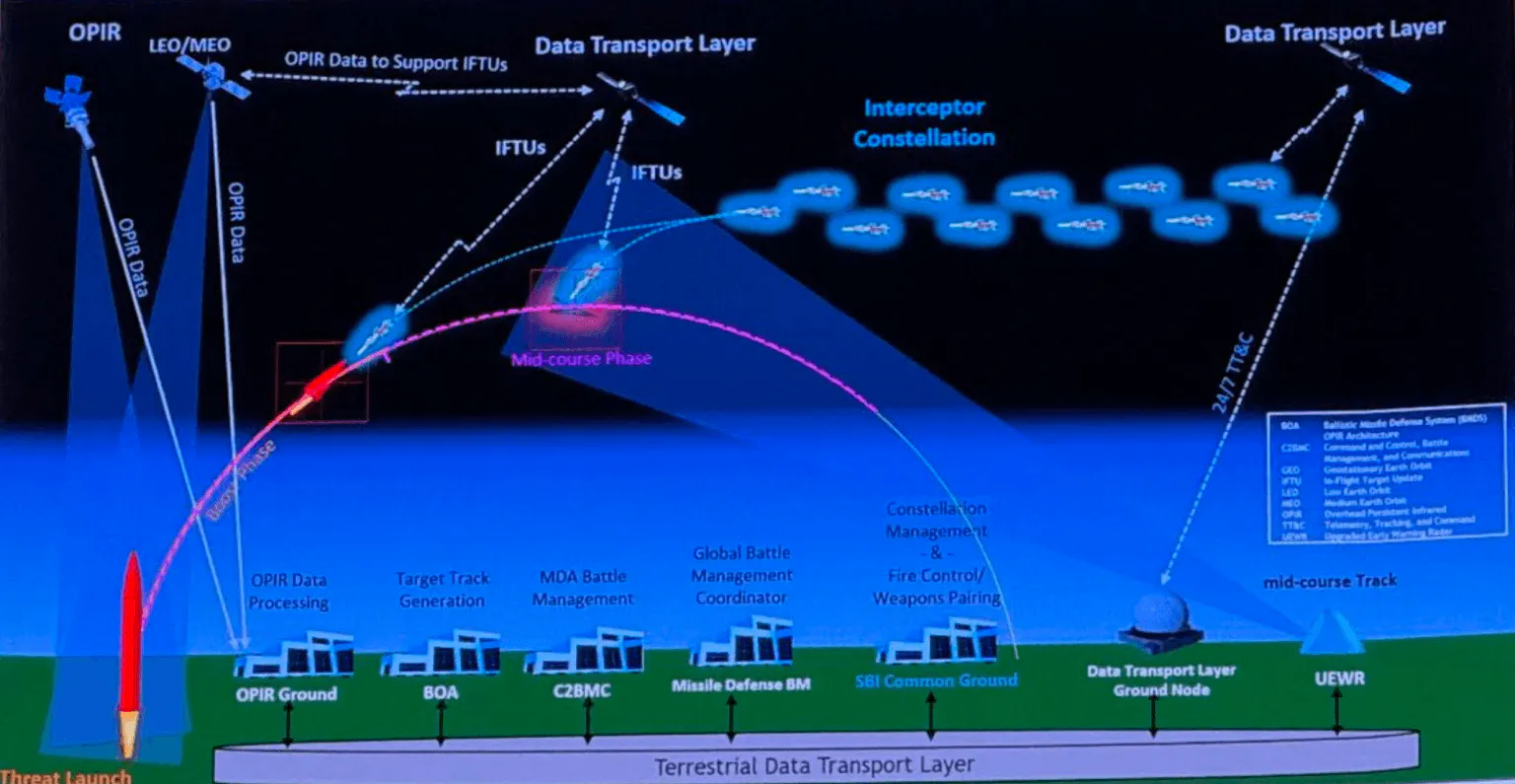

The Golden Dome Missile Defense Architecture

Source: SpaceNews

The US Golden Dome missile defense initiative, a generational shift in US missile defense built around space-based sensors and space-based interceptors, represents a material opportunity for Apex due to the scale and structure of the architecture. Golden Dome is a space-based defense network that uses satellites to detect, track, and intercept ballistic and hypersonic missiles before they reach their targets. It is designed as a multi-layered system composed of space-based sensors, command-and-control nodes, and interceptor platforms. At full deployment, the architecture is expected to require thousands of interceptors supported by distributed space-based data processing. The program launched with an initial $25 billion appropriation, and as of March 2026 the official Space Force estimate of total program cost had risen to approximately $185 billion.

Apex’s opportunity is concentrated at the satellite platform layer. If production scale reduces the unit cost of a standardized small satellite bus to approximately $3.5 million, the satellite hardware component of Golden Dome alone could represent more than a $30 billion total addressable market. This estimate excludes payloads, launch, and ground infrastructure, and reflects only the underlying spacecraft platforms.

The market opportunity for Golden Dome is highly competitive. Incumbent defense primes such as Lockheed Martin and Northrop Grumman are active participants, alongside fast-moving companies such as SpaceX and True Anomaly. As of October 2025, SpaceX had reportedly secured a $2 billion contract to deliver an initial 600-satellite constellation for missile tracking, indicating both the scale of the program and the premium placed on rapid manufacturing and deployment.

In April 2026, the US Space Force awarded up to $3.2 billion in space-based interceptor prototype contracts to twelve companies, including Anduril, Booz Allen Hamilton, General Dynamics Mission Systems, Lockheed Martin, Northrop Grumman, Raytheon, SpaceX, and True Anomaly. Apex was not on the list. The exclusion does not close the door; the SDA’s tranche-based procurement model continues to produce follow-on contract rounds, and Apex has aligned Project Shadow (June 2026 launch) as the operational proof point intended to position the company for future Golden Dome awards under a fixed-price procurement model. Apex’s Series C and Series D financings were explicitly aligned with this opportunity, funding the manufacturing capacity required to support sustained, high-rate satellite and interceptor production. Whether Project Shadow translates into contract flow is the central open question for Apex’s Golden Dome upside.

5G Direct-to-Device (D2D) Market

Mobile network operators are seeking to eliminate terrestrial coverage gaps by enabling standard smartphones and connected devices to communicate directly with satellites, bypassing ground-based 5G infrastructure. This approach, known as direct-to-device (D2D), establishes a direct radio link between consumer devices and satellites without reliance on terrestrial base stations. The addressable population for D2D connectivity is estimated at nearly 5 billion people globally. Industry projections indicate that by 2033, more than 425 million monthly active users will rely on D2D services as device compatibility expands and safety and emergency-use cases mature.

Apex’s opportunity in this segment is driven by the scale and cadence of D2D constellation deployments, which require rapid production of large satellite volumes. Typical D2D architectures require a minimum of 200 satellites, as observed in programs led by MDA and EchoStar, and can scale into the thousands. For example, Logos Space received FCC approval for a 4.2K-satellite broadband constellation. At assumed unit prices of approximately $1.5 million, these programs translate into individual contract values ranging from $500 million to $1 billion.

The Comet satellite platform is specifically engineered to meet the technical demands of D2D constellations. Comet employs a flat-pack architecture optimized for high-density launch configurations and is designed to support the high power budgets required by large-aperture D2D antennas, delivering up to 6 kilowatts of onboard power.

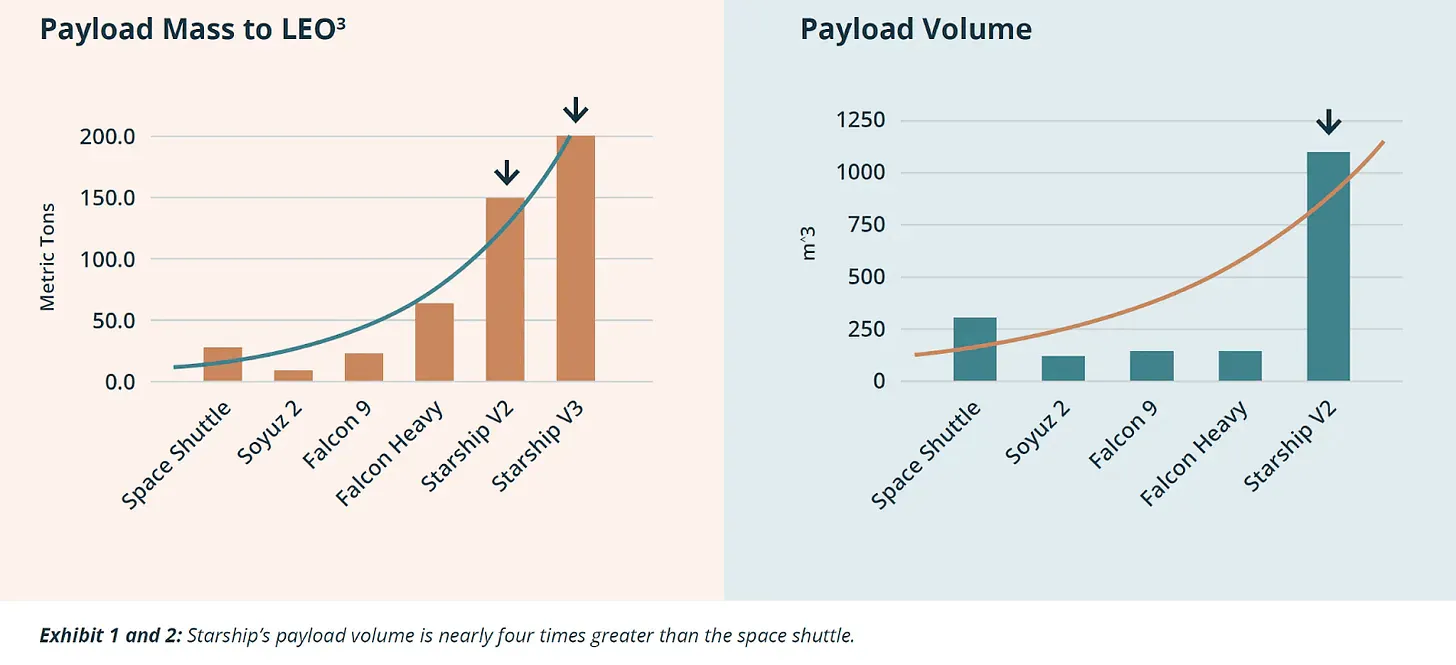

Strategic Scaling via SpaceX Starship

The successful operational deployment of SpaceX’s Starship would represent a structural inflection point for Apex’s business model. Starship’s projected LEO payload capacity of approximately 150 metric tons, roughly 3x that of Falcon 9, could meaningfully reduce launch costs, which as of 2025 accounted for nearly one-third of total constellation program costs. A reduction at that scale would accelerate the industry’s shift toward large-scale, standardized satellite deployments.

Source: The Overview

For Apex, three downstream effects matter. First, lower-cost access to orbit expands the economic viability of large constellations for a wider set of commercial and sovereign customers, increasing demand for high-volume, standardized satellite platforms. Second, lower launch costs enable new infrastructure-driven use cases, including space-based data centers and in-orbit compute platforms.

Source: The Overview

Third, these architectures require the repeated deployment of commoditized hardware at scale, exactly the high-rate, repeatable production profile Apex is built around. Major technology and aerospace players including Google and SpaceX have publicly explored space-based data center concepts. Such systems would increase both the total number of standardized assets deployed in orbit and the replenishment cadence, as orbital data centers are expected to have shorter operational lifetimes than traditional space assets driven by rapid computing chip obsolescence.

Key Risks

Launch Availability & Bottlenecks

Apex’s 12-month speed-to-orbit commitment is structurally dependent on access to external launch capacity. While the introduction of heavy-lift vehicles such as Starship is expected to increase total launch throughput, the small-satellite market continues to face a persistent risk of constrained access to orbit as operators of mega-constellations such as Starlink and Kuiper prioritize the deployment of their own internally manufactured spacecraft.

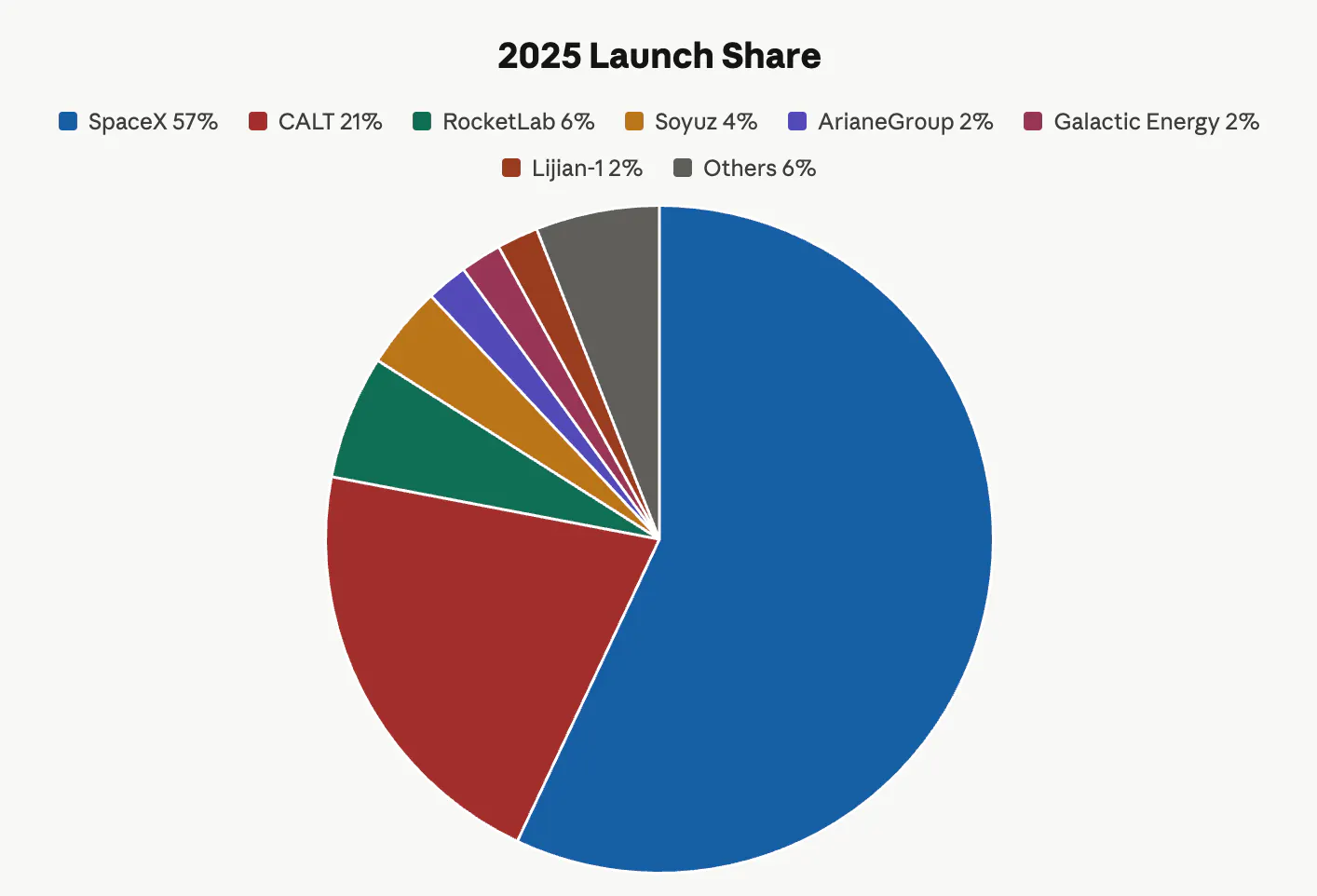

For an independent satellite bus manufacturer, disruptions in the rideshare market or preferential allocation of launch capacity to sovereign or internal payloads create a structural bottleneck that cannot be mitigated through manufacturing execution alone. Although multiple launch providers exist globally, the number capable of delivering reliable, high-cadence launches at scale is limited. As of 2025, SpaceX and CALT (China Aerospace Science and Technology Corporation) together accounted for approximately 88% of global launches, resulting in a highly concentrated launch supply. A sustained re-prioritization of SpaceX launch capacity toward internal deployments would materially impact Apex’s ability to meet delivery timelines and execute its business model.

Source: Space Stats; Contrary Research

The Consolidation Threat

The legacy small-satellite manufacturing market is characterized by consolidation. Many agile manufacturers that successfully demonstrated a standardized, productized approach have been acquired by incumbent defense primes, as illustrated by Lockheed Martin’s $450 million acquisition of Terran Orbital in August 2024 and RTX’s acquisition of Blue Canyon Technologies. These transactions reflect the difficulty of sustaining independent scale in a market dominated by large integrators.

Given relatively flat commercial demand outside vertically integrated operators, Apex may face a constrained pool of independently addressable customers. In this context, operating a large, capital-intensive manufacturing facility increases strategic pressure, as fixed costs must be supported by consistent high-volume contracts. This dynamic increases the likelihood that Apex becomes an acquisition target for players seeking to secure additional capacity in the value chain, including launch providers with direct access to orbit or telecommunications operators with direct access to end customers.

This consolidation risk is reinforced by structural changes in the telecom sector. Legacy television revenues are declining, while broadband markets are experiencing increased competition driven by Starlink. As telecom operators consolidate or vertically integrate to defend margins and control infrastructure, further consolidation within the small-satellite manufacturing market is likely.

Capital Intensity of Factory One Scaling

Apex has committed to doubling the footprint of Factory One and increasing satellite production capacity by 50% using Series D proceeds. The target capacity of over 200 satellites per year requires sustained, high-volume contract flow to absorb fixed manufacturing costs. The company’s existing backlog of approximately $100 million is meaningful but does not yet support the full output capacity of the expanded facility.

This creates a structural dependency on Golden Dome, SDA Tranche cadence, and large D2D constellation orders materializing on schedule. Each of these demand vectors carries timing and political risk: Golden Dome’s $185 billion projected program cost extends through 2029 but its annual flow depends on Congressional action; SDA tranches have historically slipped relative to original timelines; commercial D2D programs remain pre-production for most operators. If two or more of these demand vectors slip in the same window, Apex would face a margin squeeze that could pressure either pricing discipline (forcing concessions to fill the factory) or the speed-to-orbit narrative (if the company throttles production to preserve unit economics).

The Comet platform also lacked flight heritage as of 2026, which is a precondition for major D2D contract awards. If Comet’s 2028 in-orbit demonstration slips, the multi-product growth narrative narrows in the near term.

Golden Dome Exclusion & Project Shadow Dependency

Apex was not among the twelve companies awarded space-based interceptor prototype contracts in April 2026, the first major Golden Dome procurement round. The winners, including Anduril, Booz Allen Hamilton, General Dynamics Mission Systems, Lockheed Martin, Northrop Grumman, Raytheon, SpaceX, and True Anomaly, collectively received up to $3.2 billion in commitments. Apex’s strategic response, Project Shadow, is a self-funded $15 million space-based interceptor demonstration scheduled for launch in June 2026. The mission uses the Nova satellite platform to host an “Orbital Magazine” payload comprising two scaled interceptor prototypes powered by high-thrust solid rocket motors, designed to prove system-level capability ahead of formal Space Force requirements definition.

This concentrates a meaningful share of Apex’s Golden Dome optionality on a single demonstration mission. If Project Shadow slips, fails to demonstrate the targeted capabilities, or produces results that the Space Force does not view as competitive with already-funded primes, the company’s path into the largest near-term defense satellite opportunity narrows. The downside scenario is that Golden Dome consolidates around the April 2026 award winners, leaving Apex to compete for SDA Tranche follow-ons and commercial constellation work without the largest near-term defense satellite opportunity in its addressable pipeline.

Summary

Apex operates in the small satellite manufacturing market, which is moving from bespoke, low-volume programs toward standardized, higher-throughput production as LEO constellations and defense demand increase. Apex offers standardized, flight-proven satellite buses with shorter delivery timelines than legacy primes. Key open questions include the depth of commercial demand outside defense primes, the company’s ability to sustain margin discipline as Factory One scales, exposure to market consolidation as telecom operators and launch providers continue to integrate vertically, and whether Project Shadow translates the Golden Dome opportunity into contract flow once the demonstration mission concludes.