Thesis

As of August 2024, 65% of Americans live paycheck to paycheck, with personal finances defined by limited liquidity and minimal margin for error. As of January 2025, an unexpected cost of $1K can cause significant financial distress for these Americans, with 59% of Americans not having enough savings to cover such emergencies. This financial instability is exacerbated by a system that relies on static credit scores and inflexible underwriting models, excluding people without traditional credit histories or thin credit lines from building personal credit.

Concurrent with this instability has come an increase in predatory lending practices, with payday lenders collecting $2.4 billion in borrower fees in 2022, up $200 million from 2021. That same year, banks generated $7.7 billion in overdraft fees. Meanwhile, regulatory enforcement against these practices has weakened, leaving many consumers exposed to exploitative fees and high-cost loans. In January 2025, the U.S. Consumer Financial Protection Bureau (CFPB) dropped an enforcement action against Capital One, which had accused the bank of denying customers more than $2 billion in promised interest on its “360 Savings” accounts. A month later, in February 2025, the CFPB dismissed an additional four cases related to predatory practices by lenders and financial services firms.

In an attempt to address these growing instabilities, Tilt Finance offers cash advances, budgeting tools, and financial insights that target underserved consumers. The company uses transaction data and insights rather than traditional credit scores to evaluate customers, providing immediate access to cash without relying on conventional credit infrastructure. This product addresses liquidity gaps and short-term financial instability among low- and moderate-income Americans.

Founding Story

In 2016, Warren Hogarth (CEO) and Justin Ammerlaan (CTO) co-founded Tilt Finance with the goal of creating a more accessible and flexible financial platform for individuals underserved by traditional institutions. Tilt’s approach emphasizes analyzing real-time financial behavior, such as income patterns, recurring transactions, and account activity, to assess eligibility and support credit decisions. This method allows them to serve people who may not qualify for conventional credit products.

Source: Forbes

Warren Hogarth was born and raised in Western Queensland, Australia, on a cattle ranch, and completed a degree in chemical engineering and commerce at the University of Queensland. Initially focused on working in industry through an internship at a refinery, he hadn’t considered pursuing a PhD, viewing it as a path reserved for academics. That perspective shifted after attending a lecture on biotechnology, nanotechnology, and the future of energy and biology, which inspired him to pursue a doctoral degree. Motivated by the desire to see the world beyond Australia, he applied to international programs and became both a PhD student at the University of Queensland in chemical engineering and a Fulbright Scholar at Princeton University.

Drawn to entrepreneurship, Hogarth planned to build a fuel cell startup in 2002, but as the energy density and technology evolved faster than expected, the market outpaced his ability to compete. Due to visa constraints, he applied to business school to remain in the U.S. and was accepted to Harvard Business School, where he immersed himself in its innovative culture. Working throughout his studies to make ends meet, a mantra he carried into the early years of Tilt, he started a fintech company during school in 2007. However, the company encountered issues with securities law and faced stiff competition from another startup called KaChing, which would later be known as Wealthfront. Hogarth also experienced firsthand how a lack of credit history could limit credit access and create barriers.

Despite early momentum, Hogarth couldn’t continue with the startup, as his co-founders deferred business school to keep building while his visa prevented him from doing the same. After graduating, he joined Sequoia Capital as an investor. One major draw to founding his own company stemmed from a desire to build a team grounded in collaboration and shared learning, something he found lacking at Sequoia, where investors spent more time with their portfolio companies than with one another. With a growing conviction to tackle everyday financial problems, Hogarth began searching for a technical co-founder. He was eventually introduced to Ammerlaan through a close friend, and both shared a vision of improving financial lives through smarter, more inclusive tools.

Ameerlaan, who had founded both a hedge fund and a software platform, brought technical expertise to the venture. He holds a BS in mathematics and computer science from the University of Tasmania and a Master’s in Management from Melbourne Business School. Together, Hogarth and Ammerlaan launched the new company, then called Empower, with the belief that personal finance should be simple, transparent, and built for the realities faced by the underbanked.

The company announced its rebrand from Empower to Tilt in August 2025, reflecting a renewed mission to expand access to fair credit through a broader range of products designed to support users over the long term. In 2019, Tilt expanded its leadership team by hiring Stephanie Lin (formerly IPSY’s Vice President of Marketing) as Chief Market Officer and Mac Muir (formerly Engagement Manager at McKinsey) as Head of Operations and Finance. In 2022, Muir became the CFO of Tilt.

Product

Cash Advance

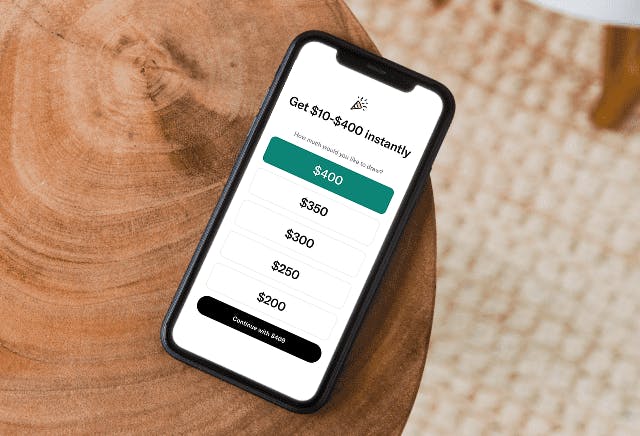

Tilt’s flagship product is its cash advance feature, which provides users with immediate access to dollar credit ranging from $10 to $400. Advances can be disbursed either instantly or within a few business days, depending on the user’s selected delivery method. Repayment is automatically withdrawn from the user’s linked bank account on a scheduled date. Traditional short-term credit options, such as payday loans, can carry APRs of almost 400%. Tilt’s model charges no interest, imposes no late fees, and does not require a credit check. Instead, eligibility is determined based on income, transaction patterns, and recurring expenses.

Source: Tilt

This approach expands access to users who may be excluded from conventional lending due to a lack of credit history. Use cases of Cash Advance include covering unexpected bills, avoiding overdraft fees, or bridging paychecks. To support user flexibility, Empower offers instant delivery (for a tiered fee) and free standard ACH transfers. The system is designed to scale responsibly for users who maintain consistent income and positive repayment behavior, qualifying them for higher advance amounts over time, reinforcing retention and user engagement.

Line of Credit

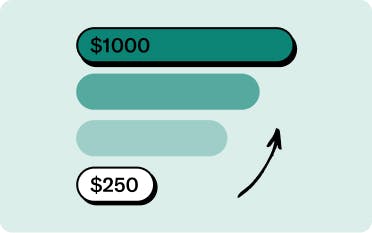

Tilt’s Line of Credit is a line of credit designed for users seeking more structured borrowing than what the company’s core cash advance features provide. Thrive offers users access to a credit line ranging from $200 to $400, which can increase up to $1K over time based on repayment history and continued eligibility. Funds are disbursed instantly upon request, and users are offered flexible plans that can be tailored to their cash flow needs.

Source: Tilt

The credit product fills a critical gap between short-term liquidity and long-term financial stability. Unlike traditional lenders, the credit line does not require a minimum credit score to qualify, which aligns with Tilt’s mission. It is designed for individuals seeking a flexible way to build credit history, particularly those underserved by conventional lenders. This structure helps more users beyond episodic borrowing into a more consistent credit-building behavior.

The product is issued in partnership with FinWise Bank, a Utah-based institution that handles compliance and regulatory oversight. This partnership allows Tilt to focus on product experience, data-driven underwriting, and servicing, while maintaining adherence to industry standards. Together, they create a credit-building progression path that scales with user behavior and financial health.

Credit Cards

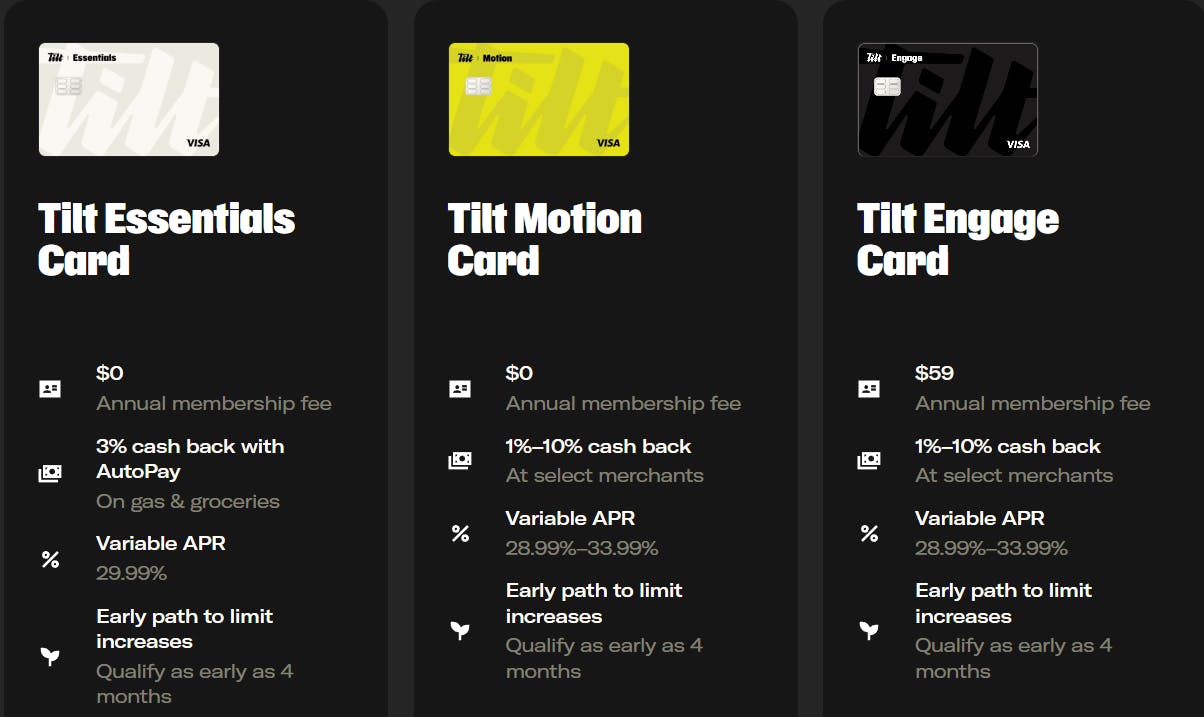

With its rebranding to Tilt, Tilt has retired its Petal card line and replaced it with three new Tilt cards. Issued through WebBank, the cards include Essentials, Motion, and Engage.

Engage and Motion primarily cater to consumers with lower credit scores or thin files. While Motion has no annual fee, Engage has an annual fee of $59. Both carry a 28.99%-33.99% APR and offer 1-10% cash back for select purchases. Each card has a transaction fee of 5% or $5, whichever is greater, and may apply late fees of $40.

Essentials is better for everyday expenses and bonus cash back, making it the more stable option. It carries no annual fee, offers a 3% cash back with AutoPay, and a fixed APR of 29.99% when the account is open, which will vary with the Prime Rate. Unlike Engage and Motion eliminates penalty fees and transaction fees, making it more attractive to users looking for a steadier option.

Source: Tilt

This transition positions Tilt to better suit its consumers and goals. Instead of focusing on strictly building credit, the Tilt cards will be more accessible for a broader range of consumers. While traditional credit card issuers only look at credit history, Tilt also uses a user’s bank account to see their spending habits. The company looks for responsible spending rather than just a good credit score.

All three cards include access to Leap by Petal, a behavioral rewards program designed to encourage financially healthy habits through goal-based incentives. Participation in Leap is optional and does not impact a cardholder’s ability to use their credit card, but it offers a structured path toward greater credit access to those who engage.

At its core, Leap provides cardholders with the opportunity to earn rewards such as a credit limit increase by completing two specific goals. Goal 1 requires users to make six consecutive monthly payments of either their minimum payment or 15% of their statement balance, whichever is greater, by the due date. The payments must be “qualifying payments,” meaning returned or disputed payments do not count. Users who do not carry a balance for a particular month are not penalized, and inactivity delays progress. However, missed payments reset the streak. Goal 2 ties directly to a user’s VantageScore, a credit score system to assess consumer creditworthiness. Petal 1 and Petal 1 Rise cardholders must avoid a drop of 50 points or more from their Leap baseline score, while Petal 2 users must avoid a drop of 25 points.

Credit score visibility and goal tracking are integrated into the Leap dashboard in the Petal app, which helps users monitor their progress. For those without a VantageScore at the start, Petal establishes a baseline score after approximately three months of usage. If a user completes Goal 1 but still lacks a score, they can be considered for an increase.

Upon completing both goals, users are considered for a credit limit increase, subject to account standing and a review of their financial profile. This includes evaluation of income, obligations, and capacity to repay. If approved, users receive an increase of at least $50, with adjustments based on their individual creditworthiness. Petal notes that only one Leap-based credit limit increase is available per user, and credit limits are capped at $5K for Petal 1 and $10K for Petal 2.

Leap blends educational elements with real financial rewards. It reinforces credit best practices while lowering the perceived barriers to responsible usage. Leap enhances the appeal of Petal cards among credit newcomers and serves as a retention mechanism, giving users a clear path to product upgrades and deeper financial inclusion.

Debit Card

Tilt's debit card offers users access to cashback perks, which can be activated directly through the app. Eligible users can select one perk at a time, such as rewards for spending in specific categories. Once activated, perks apply automatically to qualifying purchases. Users can switch between available perks at any time, though only one can be active at a time. Each perk comes with its own maximum cashback amount and eligibility terms.

Source: The College Investor

Automatic Savings

Tilt’s AutoSave feature helps users set aside money toward personal financial goals. Users can choose either weekly savings or align transfers with their predicted paycheck schedule. The platform uses income and expense data to identify optimal times for transfers, ensuring that funds are not withdrawn during periods of low balance. Up to four transfers can be made weekly, Monday through Thursday, with flexibility to adjust or pause the plan at any time. Savings are deposited into Empower’s FDIC-insured account and are accessible at any point.

Spend Tracking and Budgeting Tools

To promote better financial awareness, Tilt includes a suite of tools for monitoring income and expenses. Users receive monthly spending summaries and can set category-specific trackers with personalized limits and frequencies. Real-time alerts notify users of paychecks, bills, or purchases, making it easier to maintain control over cash flow. Budgets can be created and edited through the Analysis tab, helping users understand and manage where their money is going.

Market

Customer

Tilt targets the financially underserved: individuals who are either excluded from traditional credit or lack the financial stability to use it effectively. Consumers are disproportionately lower-income, often living paycheck to paycheck, and face volatile or irregular income streams.

45 million Americans are considered credit invisible or have thin credit files, excluding them from access to mainstream credit cards or personal loans. 42% of Americans report being unable to access financial products due to low credit scores. This number increases to 74% among individuals with poor credit. Tilt’s model of offering no-interest, no credit check advances is one of the few ways for this group to responsibly access credit.

There’s also distrust in traditional banking institutions, amplified by the collapse of banks like First Republic and Silicon Valley Bank in 2023, leaving nearly 50% of Americans questioning the safety of their money as of April 2023. This creates space for fintech platforms like Tilt to serve as alternatives.

At the same time, the erosion of financial literacy, particularly among Gen Z and Gen Y, has driven a growing demand for real-time, personalized financial guidance. Tilt’s blend of budgeting tools and real-time alerts appeals directly to these users, especially as more turn to mobile-native solutions for everyday financial decisions.

Market Size

Empower operates primarily within the consumer fintech industry, with a specific focus on the cash advance and short-term liquidity market. This market includes products such as payday loans, credit card cash advances, merchant cash advances, and mobile-based cash advance apps. Traditional credit card cash advances often carry high interest rates and no grace period, while payday loans are associated with steep fees. In contrast, Tilt and its peers offer lower-friction alternatives that still require repayment within a short timeframe. The broad cash advance market was valued at $73.7 billion in 2022.

Competition

Chime Financial: Chime was founded in 2013 as a fintech company offering fee-free banking services, early pay, and debit and credit card products. In August 2021, the company raised a $750 million Series G round at a valuation of $25 billion, bringing its total raise to over $2.6 billion. Later, the company went public at a valuation of $11.6 billion, raising $700 million in its offering and an additional $165 million in shares. Key investors include Sequoia Capital, General Atlantic, Tiger Global, Softbank, and Dragoneer Investment Group. Its digital banking services and large user base set it apart from Tilt’s focus on cash advances, budgeting, and credit-building tools, making Chime a broader banking alternative. As of August 2025, Chime has a market cap of $10.8 billion.

Varo Bank: In 2015, Varo Bank was founded to offer checking, savings, personal loans, cash advances, and credit-building services. Varo became the first neobank to secure a full-service national bank charter, allowing it to operate as a fully regulated bank without relying on a partner bank. It has raised $1 billion as of August 2025, including a $510 million Series E round. The company was targeting a $55 million Series G in early 2025, of which it had closed $29 million by February 2025. Notable investors include Warburg Pincus, Lone Pine Capital, and BlackRock. While Tilt operates through partnerships and focuses on cash advances and credit services, Varo offers a more centralized platform built around direct deposit banking with regulatory independence and a broader suite of core financial products.

Current: Founded in 2015, Current provides mobile checking accounts with features like early direct deposit, cashback rewards, and instant gas hold removal. It raised a $220 million Series D round led by Andreesen Horowitz in April 2021, valuing it at $2.2 billion. In December 2024, it secured $200 million in new capital from Cross River Bank and General Catalyst, bringing its total funding to over $600 million. Other investors include Wellington Management, Tiger Global Management, and Foundation Capital. While both Tilt and Current offer financial tools aimed at underserved consumers, Current operates more broadly across the digital banking stack, offering core banking services in addition to liquidity and credit features. Tilt is more narrowly focused on cash flow smoothing and credit-building as entry points into consumer finance.

MoneyLion: Founded in 2013, MoneyLion offers a wide range of financial products, including personal loans, cash advances, credit cards, cashback banking, high-yield savings, and portfolio management. In 2019, it raised $100 million in a Series C round by Edison Partners and Greenspring Associates, bringing its total funding to over $200 million. In April 2025, Gen Digital acquired MoneyLion for about $1 billion. MoneyLion’s broad product mix spans lending, banking, and investing verticals, making it a holistic wellness platform. This suite of products’ approach aligns with Tilt’s diverse offerings but leans more heavily into investment and banking products.

EarnIn: EarnIn was founded in 2012 and focuses on earned wage access, allowing users to access up to $150 per day of their earned wages. It also provides tools for paycheck maximization, savings, credit monitoring, and financial planning. The company raised $125 million in a Series C round from DST Global, Andreesen Horowitz, Spark Capital, and Coatue Management in 2018. As of August 2025, it has raised a total of $190.1 million and was valued at around $527 million. Unlike Tilt’s broader financial ecosystem, EarnIn concentrated exclusively on short-term liquidity tied to wages, making it a more niche player.

Dave: Dave was founded in 2016 and provides cash advances, banking services, goal savings tracking, and a side hustle feature. Dave raised a $50 million Series B round from Norwest Venture Partners in October 2019, bringing its total raise to $186 million before going public via SPAC in 2022 at a market value of $3.1 billion. The company has emphasized its proprietary AI underwriting engine, CashAI, which determines ExtraCash eligibility based on over 180 data points related to income, employment, spending, and account history, while avoiding the use of credit scores. Additionally, its generative AI assistant, DaveGPT, offers real-time, in-app financial support with an 89% issue resolution rate. Dave’s reliance on dynamic underwriting and embedded generative AI creates a differentiated product experience that contrasts with Tilt’s more streamlined but similarly automated approach to cash advances and budgeting.

Brigit: Brigit started in 2019 and offers short-term cash advances, automated overdraft protection, credit-building services, and financial health tracking. It also provides users with the opportunity to earn and save more money through side gigs or exclusive offers. The company operates on a subscription model with tiered prices at $8.99 and $14.99 per month. Brigit raised $35 million in a Series A led by Lightspeed Venture Partners, with participation from DCM, Nyca, Cannan, DN Capital, and CRV. The company has entered into a definitive agreement with Upbound Group to be acquired for up to $460 million in December 2024.

Business Model

Tilt generates revenue through a subscription model priced at $8 per month as of August 2025, which provides access to its core services, including cash advances, budgeting tools, and personalized financial recommendations. Users can request cash advances of up to $400 without interest. There is no fee for receiving a cash advance via ACH to an external bank account, though instant delivery incurs a tiered fee as follows:

Tilt also earns interchange revenue, alongside income through interest, transaction fees, and late fees through affiliated credit products such as Petal and Thrive.

Traction

Since launching in 2017, Tilt has steadily scaled, reporting 250K users in 2018, over 600K users in 2020, and 2 million active subscribers in 2024, and over 3 million subscribers and 5 million customers as of August 2025. It reached profitability in 2022. As of 2025, Tilt claims to have helped users with over $2 billion in disbursed advances, facilitated credit access, and user financial progress.

In April 2024, Tilt acquired Petal, a credit card provider known for underwriting customers without traditional credit scores, expanding its credit-building offerings. Prior to the acquisition, Petal was valued at $800 million in January 2022, but faced a cash crunch later that year. Over its lifetime, Petal raised more than $300 million in equity and over $680 million in debt financing from investors including Valar Ventures, River Park Ventures, and Core Innovation Capital. Tilt also acquired Cashalo, a Philippine consumer credit and lending platform. Cashalo secured a $75 million loan facility from Community Investment Management in June 2025.

As of July 2025, the platform has an estimated 175K new app downloads per month. It also maintains a 4.8 rating on the iOS App Store and 4.7 on Google Play, based on hundreds of thousands of reviews, suggesting high user satisfaction.

Valuation

In September 2022, Tilt raised a $150 million Series B round, bringing its total equity funding to nearly $175 million. This round followed earlier funding milestones, including a $4.5 million seed round led by Sequoia Capital and Initialized Capital in 2018, and a $20 million Series A in 2020 backed by Icon Ventures, Defy Partners, and Nubank founder David Velez. This brings Tilt’s post-money valuation as of August 2025 to $796.8 million.

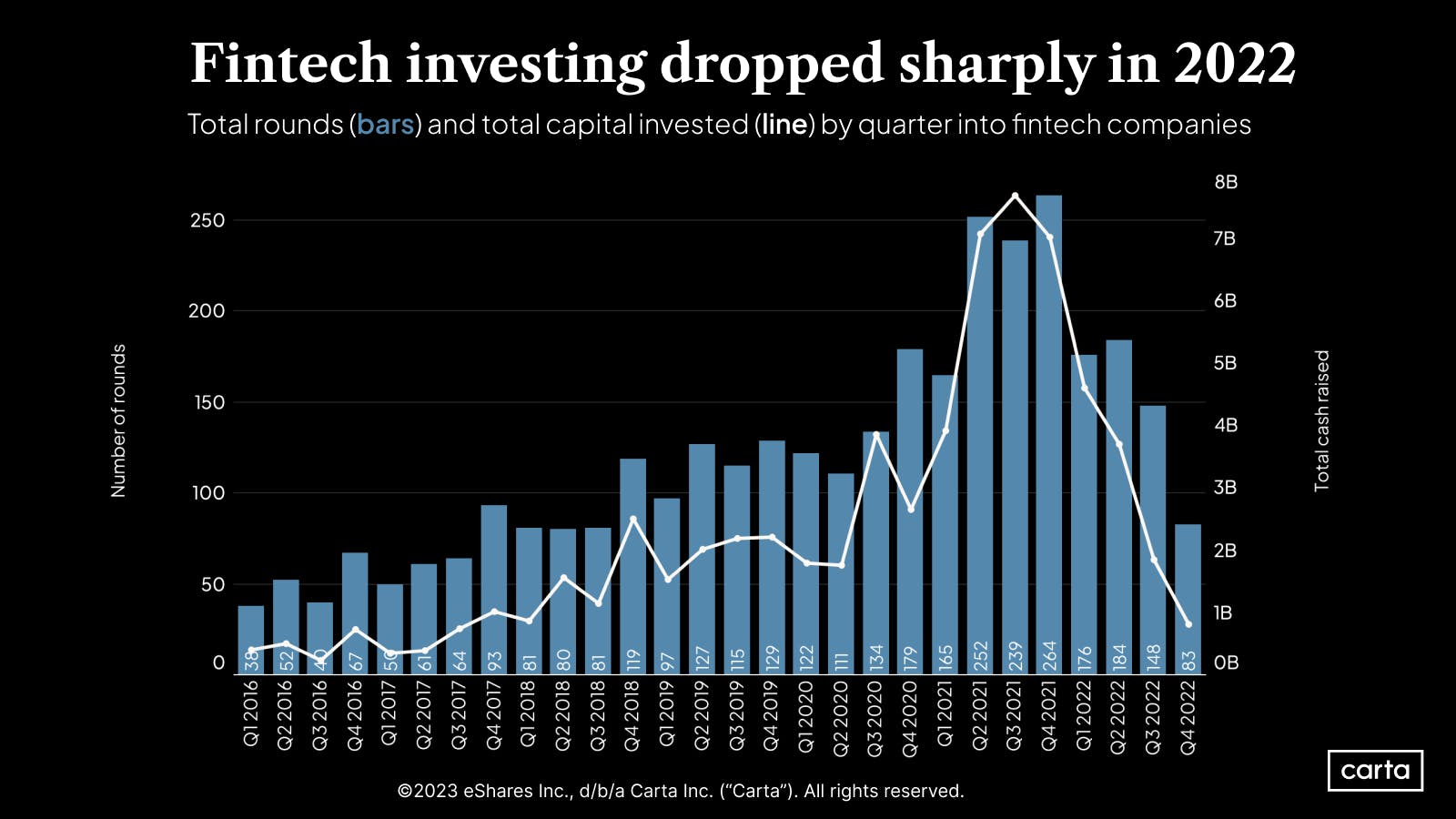

Fintech funding experienced a notable decline following the peaks of late 2020 to early 2022. From 2022 through 2024, venture capital inflows into fintech slowed significantly, with less funding and fewer acquisitions compared to prior years. While deal activity and funding are picking up in 2025, it remains muted compared to the boom period before 2022. This resurgence is evident in transactions involving several of Tilt’s competitors, such as MoneyLion’s acquisition and Brigit’s purchase, alongside public listings from firms like Chime. This context highlights both the challenges and opportunities Tilt faces as consolidation trends and shifting investor sentiment in the fintech sector.

Source: Carta

Key Opportunities

Expansion of Credit Limits

Tilt has demonstrated the ability to raise its Cash Advance cap, increasing the limit from $150 in 2020 to $400 in 2025. As demand for accessible, short-term liquidity grows, Tilt can build on this progression to meet larger emergency funding needs while maintaining underwriting discipline. The company operates within a growing segment, of which over 3 million U.S. borrowers use small-dollar credit-building loans, amounting to $845 million in outstanding balance, of which 93%, or 2.8 million individuals, are either without credit scores or have nonprime ones. By increasing available limits for qualified users, Tilt has an opportunity to improve retention and product utility for those progressing financially while staying within the same ecosystem.

Credit Building Through New Financial Products

A large addressable segment exists among the 50 million credit-invisible Americans who lack access to mainstream credit. Tilt’s existing offerings, such as credit monitoring and partnerships like Thrive, introduce new tools for this audience. Among credit-invisible individuals, 59% want to build their credit score, 22% report difficulty in purchasing or leasing a vehicle, 21% face higher deposits for utilities, 16% experience challenges securing an apartment, and 12% are unable to qualify for a mortgage. Offering credit-building pathways aligns with users’ longer-term needs while improving eligibility for Tilt’s products.

Key Risks

Credit and Default Exposure

Tilt’s primary product, no-interest, no credit check cash advances, serves users with limited or poor credit histories, but it also creates material exposure to non-repayment; the only consequence for users is that they cannot receive another cash advance until the existing balance is repaid. The company relies on income patterns, recurring bills, and spending behavior to determine eligibility. While this may increase access, it reduces the predictability of credit risk compared to traditional scoring methods. Although not directly comparable, analogous products like merchant cash advances have reported default rates ranging from 7% to 12%, compared to the 1.13% in early 2024 for traditional business loans. Without collateral, Tilt is exposed to similar loss potential should repayment behavior deteriorate.

Subscription Model Vulnerability in a Price-Sensitive Segment

Tilt operates on an $8 monthly subscription fee, a model that may be fragile given the financial constraints of its core user base. Many users seek Tilt during short-term financial hardships, and the perceived value of a subscription may decline if product usage is occasional. Fintech apps experience rapid attrition, with 73% of users churning within the first seven days. Retention drops after initial engagement, with rates of 14% in week 1 and only 7% in week 4 for first-time users. If users do not remain active for several months, Tilt may operate at a loss, given customer acquisition costs that average $202 per use in the fintech space.

Competitive Landscape

The consumer finance landscape has become crowded, with neobanks, payday advance platforms, and credit builders competing across overlapping demographics. Players like MoneyLion and Brigit have begun integrating additional services such as investing, gig-income generation, or employer partnerships. In the 2010s, over 300 neobanks launched worldwide. By 2023, 48.3% of U.S. banked households primarily accessed their accounts via mobile devices, a nearly 9x increase from the previous decade, showcasing the growing demand for mobile financial services.

Tilt’s focus on subscription fees and its product suite limits its network effects relative to peers who diversify into full-stack banking or employer-based benefits. Additionally, the acquisitions of competitors, such as Brigit by Upbound and MoneyLion by Gen Digital, suggest increasing consolidation and scale advantages elsewhere in the market.

Despite offering a narrower product suite than some competitors, Tilt ranks #37 in the iOS App Store Finance as of August 2025, behind Chime at #10, but ahead of other competitors. This suggests that Tilt’s current positioning resonates with users. However, as competitors layer on features, expanding Tilt’s offerings may be essential to sustaining retention, increasing customer lifetime value, and defending against churn over time.

Summary

Tilt Finance is developing a financial platform designed for underserved and credit-invisible Americans. Primarily focused on providing cash advances to address short-term liquidity needs, Tilt has expanded its offering to include structured credit products and credit card access. This creates a product ladder that helps users transition from immediate financial support to building long-term credit participation. By bypassing traditional infrastructure, Tilt aims to solve the critical issue of financial access by providing marginalized consumers with timely tools to manage immediate financial needs and navigate short-term challenges, while creating pathways toward sustainable credit building.