Recent global conflicts, from Russia and Ukraine to Iran and Israel, have seen a resurgent awareness of the frailty of US munitions stock, which has been drawn down by both direct and indirect involvement in these events. While exact stockpile volumes are not disclosed, it is estimated that supplies of US warheads and the missiles that carry them have declined by nearly an order of magnitude since their peak during the Cuban Missile Crisis. Analysts have estimated that in the event of a conflict in the Pacific between China and Taiwan, US munitions supplies could be depleted in as few as three days, with some higher-tier terminal-phase missile supplies potentially depleted in the first 24 hours of conflict.

This was a foreseeable problem. Advocates for deterrence have supported expanding munitions stockpiles and accelerating production timelines for decades. While improving technical performance (precision and range) is useful, increasing attritable mass, or the volume of munitions that can be produced and pointed at a target set per year, is the actual measure of credible deterrence. And we have a critical bottleneck problem.

Historically, the decline of US munitions production capacity has been attributed to the bottleneck imposed by solid-rocket motor (SRM) casting, which only a handful of US companies are authorized to perform as of May 2026. The limitation on expanding solid rocket motor production is not inherent to the motor mechanics, but rather the fuel these motors use for power: ammonium perchlorate (AP). AP is the oxidizer that enables high-performance SRM in the inventory, bound with powdered aluminum (fuel) in rubber to form a controlled explosive. This fuel is cured inside motor castings for multiple days in heavily regulated environments designed to prevent cracks or voids in the cured grain that can cause the motor to over-pressurize and explode.

The handling required for AP not only limits SRM production but also the production of AP itself. In the period following the Cold War, there were two primary AP producers in the US, the Kerr-McGee Chemical Corporation and the Pacific Engineering and Production Company of Nevada (PEPCON). On May 4, 1988, an explosion generated by some subset of the 9 million pounds of AP at the PEPCON chemical plant in Henderson, Nevada, caused a large fire, eventually killing two people and injuring 372 others. As of May 2026, there is now only one US producer of AP, the American Pacific Corporation (AMPAC) in Cedar City, Utah.

Because AP serves as a fundamental bottleneck to expanding SRM supply, new entrants to the munitions space won’t necessarily improve the US’s munitions production capacity, even if they are more nimble startups with more efficient processes. In fact, the opposite can be true: more demand for AP means there is less to go around, limiting production for any one company. A munitions base in which a single AP-plant accident can halt national missile production is more fragile than any other major military capability. Resolving this bottleneck by building a second, independent propulsion supply chain should be a strategic priority for the US defense sector.

One primary option for resolving this dependency is expanding scaled production of liquid-propulsion missiles, which are powered by widely available hydrocarbon fuels, high-test peroxide, and advanced engines adapted from commercial counterparts. In this piece, we outline how the missile supply chain became so brittle and why pursuing liquid propulsion is likely the best route to rebuilding a national munitions stockpile with a realistic timeframe and budget.

The Origins of Solid Propulsion

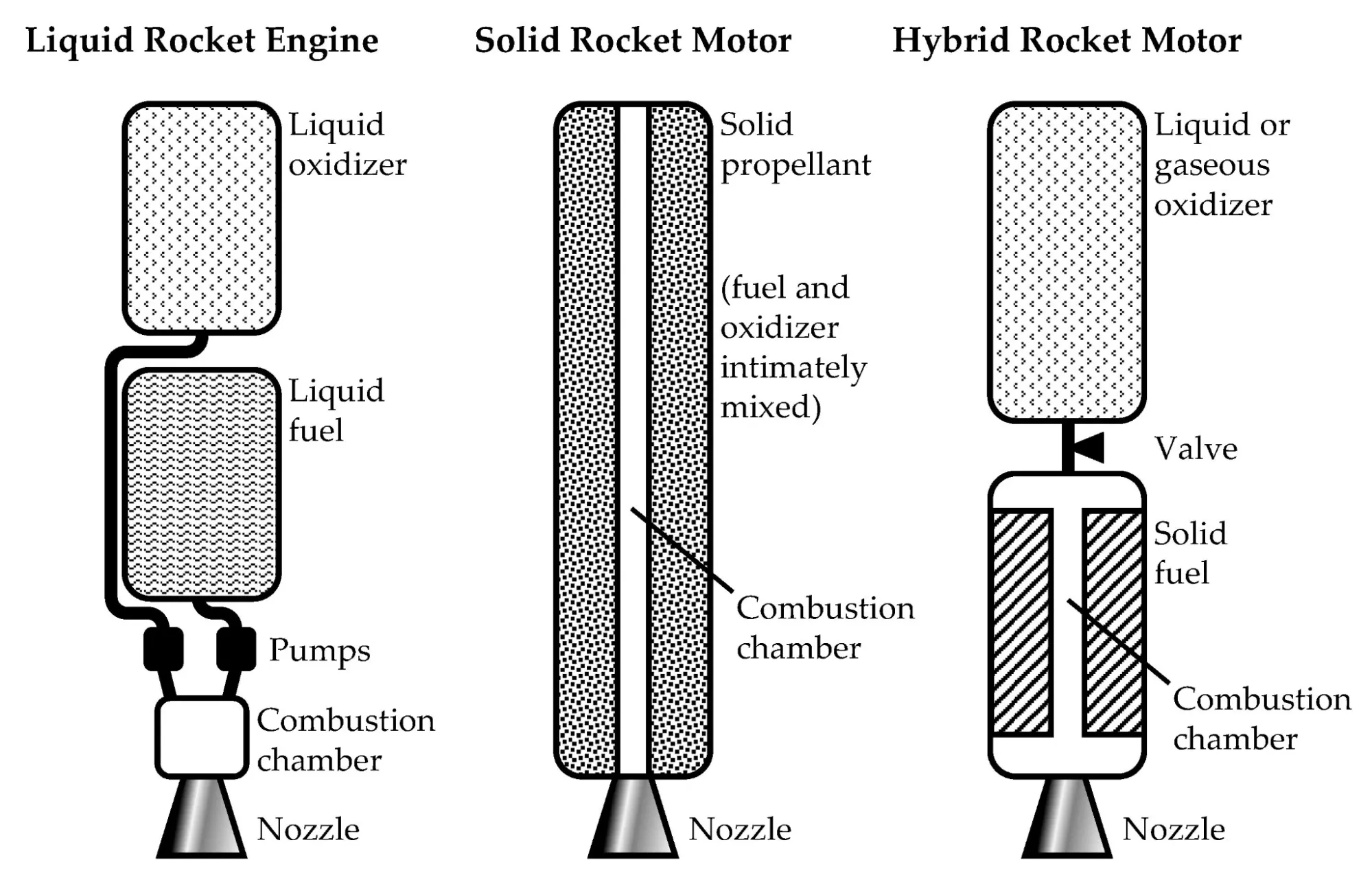

Missile fuel is a binary: it can either be solid or liquid. The choice of fuel governs a meaningful share of downstream decisions about how missiles are built and operated, including how motors are constructed, how missiles are armed for launch, and whether missiles can be shut down or throttled in flight. At the start of the US ballistic missile program in the 1940s, liquid propellants were used exclusively until the development of sufficiently performant solid propulsion fuels in the 1960s. In the decades since then, the US has transitioned to using only solid propulsion missiles, due largely to safety issues with early liquid technologies.

Liquid Propulsion Systems

Liquid-fueled missiles like the Atlas and Titan I, which were the first intercontinental ballistic missiles designed and built in the US, used cryogenic propellants such as liquid oxygen oxidizer (LOX) with RP-1 kerosene fuel. LOX boils at -183 °C, meaning it could not be stored in the missile itself because it boils off continuously and embrittles seals. On launch order, the sequence to prepare a LOX missile required 10-20 minutes before launch:

Pressurize and condition the propellant tanks

Pump RP-1 aboard

Begin LOX transfer from a vacuum-jacketed tank truck or fixed dewar (slowly, because flash-boiling at warm metal interfaces will rupture fuel lines); topping continues right up to ignition because of boil-off

Raise the missile from the silo on an elevator

Run a pre-flight checklist, then ignite

This timeline assumed nothing went wrong, but LOX leaks, fuel-line freeze-ups, and ignition aborts were common. Further, the warning time to launch in response to a strike from another ICBM (15–25 minutes flight time) was about the same as the required fueling time, which meant a launch-under-attack posture was essentially impossible.

However, there were some meaningful benefits to liquid systems, including the ability to assemble empty missiles with no fuel inside at scale without concern about detonation. Additionally, liquid fuel systems could be throttled or shut down after initiation, enabling more control over rocket flight.

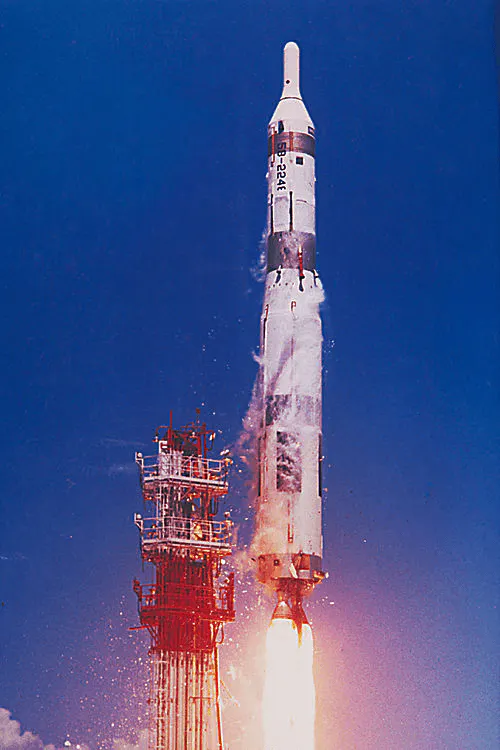

Source: Titan I Missile; Los Angeles Air Force Base

Titan II, the ICBM that followed Titan I, fixed the readiness problem by switching to hypergolic storable propellants, which could be loaded and left in the missile for years before igniting on contact, eliminating the ignition system. However, these propellants were toxic and corrosive, some destroying lung tissue even at low ppm, and others were both carcinogenic and flammable in air. Liquid-missile crews in the early 1960s worked in RFHCO ("rocket fuel handler's clothing outfit") suits while setting up these systems. Liquid-missile accident reports were almost exclusively associated with propellants, and included vapor clouds, Boiling Liquid Expanding Vapor Explosion (BLEVE), ruptures, and asphyxiations.

In October 1960, a Soviet liquid-missile ICBM ignited on the launch pad, killing an estimated 78 people. In Damascus, Arkansas, in 1980, a dropped socket wrench bounced against the ground and punctured a Titan II's fuel tank, ejecting a 9-megaton warhead into a field several hours after it was struck by the wrench due to the buildup of propellant vapors. The dangers associated with liquid missile fuels during this period ultimately motivated the US and most other global defense agencies to move towards solids. US defense leaders elected to transition to entirely solid-propellant munitions, citing storability, safety, and operational simplicity as driving factors, in the 1980s, and retired the final liquid-fueled missile, the LGM-25C Titan II, in May 1987.

Solid Propulsion Systems

Missiles with solid propulsion systems, like the Boeing Minuteman (the successor to the Atlas and Titan ICBMs), could in a silo fully fueled for their entire service lives, prepared for launch with minimal preparation and requiring no maintenance. The propellant grain was cast into the motor casing once, at the factory, and the motor was effectively a sealed appliance, requiring no plumbing, pumping, cryogenic fuels, or toxic vapors. The launch crew's job was monitoring and authentication, not propellant handling. The launch sequence for a solid rocket missile lasted about 60 seconds:

Two officers authenticate the order and turn keys simultaneously

Silo closure door is blown off by explosive bolts

Igniter fires the first stage

Missile flies

This quick turnaround from launch instructions (no fueling delay, no raising the missile, no countdown hold for valve opening) made true launch-on-warning and ride-out-and-respond doctrines possible.

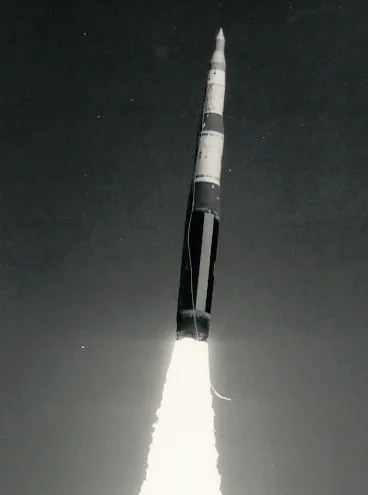

Source: Minuteman I; US Air Force

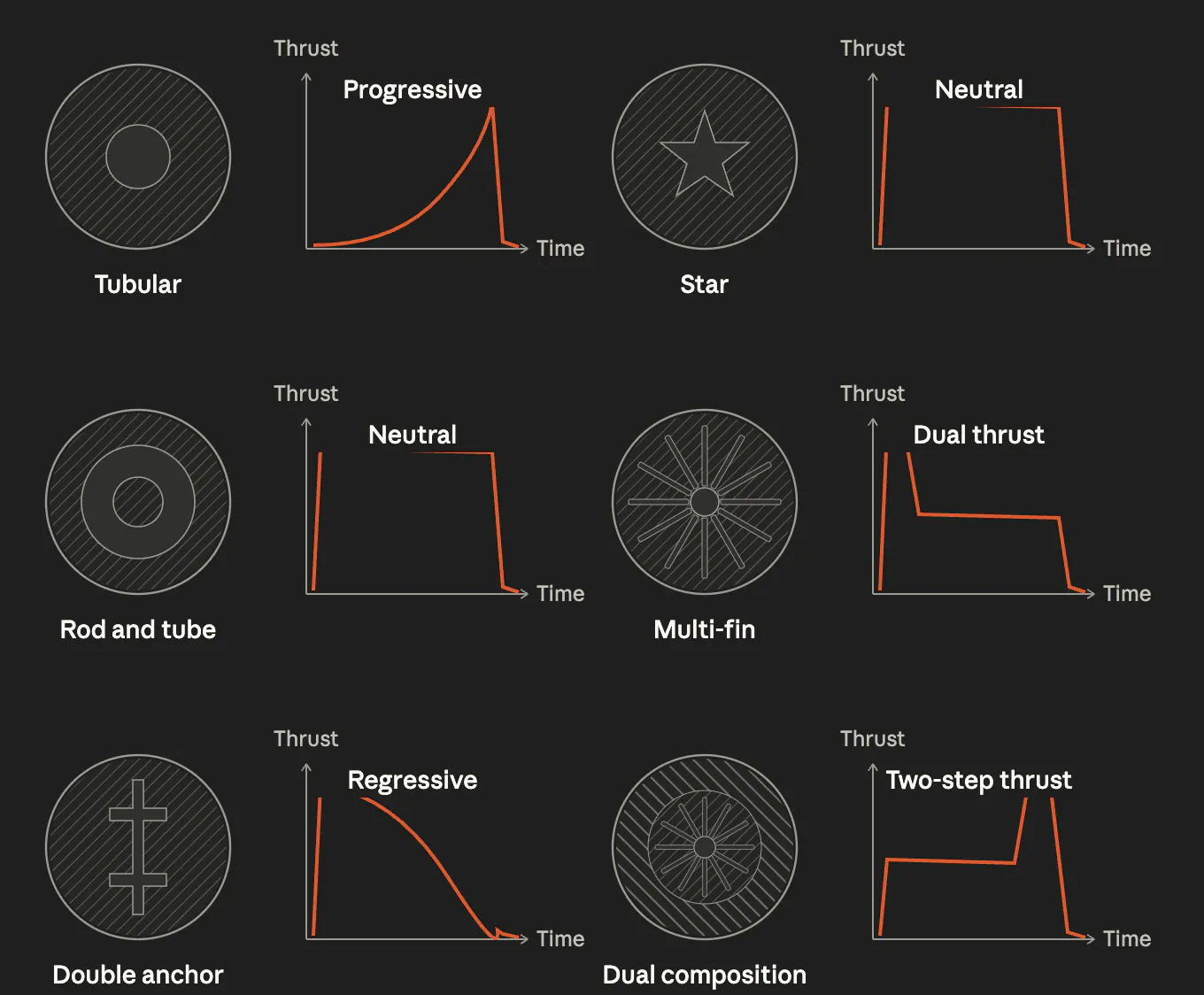

Unlike liquid engines, SRMs cannot be easily throttled, shut off, or restarted once lit. The propellant chemistry, grain shape (star, finocyl, slotted), nozzle throat erosion, and case insulation must all be modeled and qualified precisely before flight because the missile burns to completion on whatever thrust profile is baked into the geometry of the grain.

Progress in solid propulsion systems enabled the launch of the Polaris A-1 from the USS George Washington submarine in late 1960. The missile was gas-ejected from its tube by a steam generator, breached the surface, and ignited in the air. Cryogenic liquid fuel missiles couldn’t be prepared inside a submerged submarine because of the risks of explosion. Solid propellant made the submersible leg of the US nuclear triad, encompassing land, sea, and air launch, physically possible.

In contrast to liquid-missile preparation crews, solid-missile crews sat in hardened launch control capsules underground waiting for launch direction. The propellant was somebody else's problem, finished years earlier.

Supply Chain

Despite the simplicity of operating solid-propellant missiles, the production of SRMs remained challenging, ultimately shrinking the defense contractors building these parts from six in 1995 to only two in 2017 before rising back to four as of May 2026.

Ammonium Perchlorate Production

While the contraction in SRM builders is a real bottleneck for continued missile production, the drivers of this contraction make it unlikely that further investment will be sufficient to solve this problem without fundamental innovations. Specifically, the supply of AP required to build solid rocket motors contracted during the same post-Cold-War period that demand for new missiles fell, eliminating commercial incentives for new chemical producers. The construction of the one remaining domestic AP production plant, the American Pacific Corporation (AMPAC) in Cedar City, Utah, took place in 1989, just 18 months after the PEPCON disaster. Demand was actually guaranteed jointly by NASA and the DoD in 1989 in order to ensure that AP production in the US continued. The organizations funded the construction of a second AP production site and enabled producers to add a surcharge to the per-pound price of AP, which flowed through subcontractors and prime contractors back to the government as reimbursable costs. The government guaranteed minimum annual purchases for seven years, supplying both NASA and DoD missions that would have been critically vulnerable without the added production.

Composite solid propellants are typically formulated as 68-73% ammonium perchlorate (AP, NH₄ClO₄) oxidizer and 15-20% spherical aluminum powder fuel suspended in a hydroxyl-terminated polybutadiene (HTPB) prepolymer matrix, cured with an isocyanate into a crosslinked elastomer. Batches are mixed under vacuum in vertical planetary mixers, cast into insulated motor cases around a mandrel that defines the grain geometry. Consistency and precision of grain geometry govern the ballistic predictability of missiles: the burn rate is a function of local pressure and exposed surface area, so any unintended discontinuity (like porosity, propellant cracks, or case-liner-propellant debonds) instantaneously increases burn surface and drives chamber pressure up, producing either a catastrophic burst or a transition from deflagration to detonation.

Source: Melike Nikbay

Production of AP occurs in nitrogen-primed rooms, with all oxygen removed to prevent ignition. This is because solid propellants are so combustible that they have to be mixed in a vacuum and will explode upon contact with air. Workers who move material within these environments are sometimes called "angel pushers," a reference to the lethal consequences of an accident.

Because AP systems fall under DoT Hazard Class 1.3 (or 1.1 if detonable), facilities must comply with Department of Defense Explosives Safety Board (DDESB) quantity-distance criteria: mix bays, cast/cure pits, and storage magazines are sited at inhabited building distances scaling with net explosive weight, typically yielding standoffs of several thousand feet, with reinforced barricades, blowout panels, deluge suppression, conductive flooring, and Class II Division 1 electrical ratings. Operations are conducted remotely from hardened control rooms.

Given these challenges and the highly regulated nature of the industry, the process to stand up new plants is slow. Standing up a new AP facility today is estimated to require over a year for approval and around a decade for construction. This regulatory moat, combined with the safety profile of energetic-material plants, explains why no entrant has filled the gap in 25+ years.

Source: Contrary Research; DefenseNews, Deseret News, TechCrunch, and others. Note: Phase-by-phase timeline drawing on the Northrop Grumman second-source case study and the 1989 Cedar City precedent.

Northrop Grumman’s effort to become a second qualified US AP source ran from a May 2017 Army RFI to laboratory qualification in 2021 and was still scaling toward operational capacity as of April 2026; sitting in the middle of the 7-13 year range above.

Adjacent Constraints

Beyond ammonium perchlorate, the missile production supply chain is exposed to a series of concentrated upstream commodity risks. Heavy rare earth elements, dysprosium and terbium in particular, are essential alloying additions in the samarium-cobalt and neodymium-iron-boron permanent magnets used in missile guidance, actuation, and seeker assemblies. China controlled roughly 70% of mining output and 87% of global processing capacity as of 2025, a dependency Beijing has begun weaponizing through export licensing rules that largely deny shipments to companies affiliated with foreign militaries, including the United States.

Specialty alloys for high-temperature structures are similarly bottlenecked: 89% of US titanium sponge, the feedstock for titanium alloys, billets, and ingots, is imported from Japan, and niobium, the basis for the C103 alloy used in hypersonic vehicles and rocket nozzles, has not been mined in the United States since 1959. The USGS has noted that “concern” over US niobium supply has recurred in “every national military emergency since World War I.” Over 90% of global niobium production came from Brazil as of 2025, almost entirely from a single company (CBMM).

Nickel-based superalloys and cobalt-chromium superalloys used in airframe skins and hypersonic propulsion sit on top of these same constrained inputs, and the total National Defense Stockpile reserve for cobalt and cobalt alloys would be drawn down quickly under sustained surge demand. The net picture is a missile industrial base whose upstream materials layer is nearly as concentrated as its energetics layer, with single-country or single-firm exposure across multiple critical inputs.

Even those parts that have been reliably manufactured in the US are facing aging workforces and limited scaling. Carbon-carbon nozzle throats, rayon-based ablatives for nozzle liners, aerospace-grade composite cases, and pyrotechnic igniters are often manufactured by small businesses with a single furnace or autoclave.

On top of these limitations in assembling motors is a long path to adoption. Every motor for every program goes through years of static fires, environmental testing, and lot-acceptance protocols before the DoD will buy it. "Building a working SRM" and "building one the Pentagon will put on a Patriot or a GMLRS" are different problems separated by years of test campaigns.

Constrained Production

Despite the fragility of the solid rocket motor supply chain in the US, the Department of War still almost exclusively uses solid missiles. Other nations with meaningful missile munitions production programs use a wider range of technologies, including liquid-propulsion systems. Comparing the US’s stockpile against a sample of its major geopolitical adversaries, China, Russia, and Iran, is illustrative.

China: Solid propellant dominates defense systems at every tier, including ICBM scale. The DF-31 and DF-41 ICBMs and the JL-2/JL-3 SLBMs are all three-stage solid-fueled road-mobile or submarine-launched systems, with the silo-based liquid-fueled DF-5 ICBM the only major legacy holdover (this is being phased toward solid-fueled successors as Beijing builds out roughly 300 new ICBM silos). China sources AP and sodium perchlorate domestically and has enough spare capacity to be a primary exporter; China has been the primary exporter of sodium perchlorate to Iran for at least two decades, with shipments of thousands of tons documented between 2025 and 2026.

Russia: The most numerous Russian ICBM is the solid-fueled RS-24 Yars, and the SLBM leg (Bulava) is also solid; the heavy-ICBM tier is where liquid persists, in the legacy R-36M2 (SS-18 Satan) and its replacement RS-28 Sarmat. The Russian liquid-propulsion industrial base is itself stressed: a September 2024 Sarmat test catastrophically failed at Plesetsk, with personnel shortages at Proton-PM (the propulsion manufacturer) cited as a contributing factor.

Iran: Iran uses both solid and liquid missiles. The most numerous MRBM is the liquid-fueled Shahab-3 with its Ghadr and Emad derivatives. However, Iran is transitioning toward solid systems in recent years, an expansion that explicitly depends on Chinese sodium perchlorate. In response to these expansions, the US Treasury sanctioned networks of Chinese suppliers (Shenzhen Amor, China Chlorate Tech, Yanling Chuanxing) in April 2025.

As each nation adjusts its defense strategy to accommodate the challenges of scaling either solid or liquid munitions production, US production has lagged. In April 2026, the Trump Administration called on defense agreements to expand the production of missiles and other weapons, increasing production of missiles three to four times the current rates. Ramping up production with existing facilities will take multiple years, however, drawing criticism from defense budget analysts who estimate decades of production needed to rebuild stockpiles; Defense Secretary Pete Hegseth has claimed that stockpile depletion fears are “foolishly and unhealthily overstated.”

Source: Contrary Research; American Enterprise Institute, US Naval Institute, CSIS, US Army, and others. Note: Drawn from public Center for Strategic and International Studies (CSIS), Hudson Institute, Congressional Research Service (CRS), and Department of Defense (DoD) / contractor disclosures.

Alternatives to Solid Propulsion

Liquid Propulsion

Though liquid-propulsion missiles actually preceded solid-fuel systems, concerns about operational complexity, safety in the field, and storability pushed the industry towards solids despite the meaningful advantages that liquid systems deliver.

First, solids cannot replicate capabilities like throttling, in-flight shutdown, or restart that liquid propulsion missiles enable. While pulsed and pintle solid rocket motors have some of these capabilities, these are engineering accommodations of an inherent limitation and come with material and operational complexities of their own.

Second, liquid propellants are meaningfully more performant than solids, which is why they powered the first generation of ICBMs. Tactical solid rocket motors typically deliver around 250 seconds of specific impulse, while liquid bipropellant rockets achieve 300-450 seconds depending on propellant pair and stage configuration. Air-breathing architectures can exceed 1.5K seconds because they don't carry their own oxidizer. The performance gap means liquid missiles enable longer range for the same airframe, or equivalent ranges in a shorter, more maneuverable container.

Finally, and most importantly, liquid-propellant missiles deliver an unmatched production advantage because the missile itself is inert until propellants are introduced prior to launch. Essentially, missiles on the production line are like empty cars until minutes before launch. No sensitive munition handling, exclusion zones, or specialized energetic-material workforce are required to manufacture liquid missiles at scale. Liquid missile manufacturers argue that this enables gigafactory-style production more similar to existing automotive supply chains (manufacturing propelled vessels with tanks empty of fuels) than existing missile assembly operations.

As of May 2026, significant advancements in the materials and processes associated with the preparation and launch of liquid missiles have made some of the strongest arguments against liquid propellants obsolete. The operator burden of early liquid systems (pumping highly toxic fuels and manually reorienting missiles for launch) has been replaced by a fully automated system for missile fuel loading and preparation. Falcon 9, a liquid propulsion rocket, uses a launch sequence run by a flight director pressing one button, followed by 40 minutes of an automated sequence.

In addition, revived propellant pairs, like kerosene and hydrogen peroxide, are not only more widely available than early cryogenic propellants (like LOX and LH2) but are also storable for over five years. The Navy historically opposed liquid missiles because of the danger posed by fuels to personnel on manned subsea vessels. Today’s autonomous subsurface fleet changes this calculus, making liquid fuels more viable on autonomous platforms than they were on manned ones.

Hybrid Propulsion

A hybrid rocket pairs a solid fuel grain (typically a rubber-based polymer like HTPB, or paraffin) with a liquid or gaseous oxidizer (commonly nitrous oxide, hydrogen peroxide, or LOX). These designs share similarities with both solid- and liquid-only systems, but sidestep the ammonium perchlorate supply chain entirely by using an inert solid. The fuel grain is a polymer with no embedded oxidizer, and the oxidizer is a separately sourced commodity with civilian industrial supply chains.

Source: MDPI

These systems share other benefits with liquid propellant rockets. The oxidizer flow in these systems controls thrust, allowing for shutdown and throttle like liquid-only missiles (restart is also possible, though under more limited conditions than pure liquids). Similarly, the fuel sources are fully inert during manufacturing and storage.

Hybrid propulsion has lower performance efficiency (lower specific impulse) than pure liquids, but is comparable to or better than solids depending on configuration. Historically, hybrid rockets have suffered from combustion instability, low fuel regression rates (which force complex grain geometries like stars and wheels to increase surface burn area and achieve adequate thrust), and oxidizer-to-fuel ratio shift over a burn that complicates throttling. These complexities give hybrid propulsion systems performance on par with solid propulsion systems but with the complexity of liquid systems (i.e., the worst of both worlds).

Some neoprimes in the defense space are making traction towards addressing these issues, though the industry at large is looking for alternatives to hybrid propulsion altogether. Paraffin-based fuels and 3D-printed grain geometries are two proposed methods of addressing the regression-rate problem. Virgin Galactic’s SpaceShipTwo demonstrated operational hybrid propulsion at human-rated scale, and Firehawk Aerospace achieved successful test flights but has not reached production at scale.

Air-Breathing Architectures

Unlike liquid and hybrid missiles, air-breathing missiles don't carry oxidizer and instead pull oxygen from the atmosphere, compressing it through inlet geometry (ramjets) or sustaining supersonic combustion (scramjets). This architecture removes the need for an oxidizer, meaning systems require only a high-density hydrocarbon fuel (which is similar to jet fuel and has a civilian-adjacent supply base). Ducted rockets (also known as air-augmented rockets or ramrockets) combine the features of a traditional solid or liquid rocket and a ramjet by burning a fuel-rich gas generator, mixing it with captured ram air in a secondary combustor, and expelling the hot exhaust to create thrust.

Air-breathing propulsion systems can deliver up to 1.5K seconds specific impulse, similar to liquid systems and around six times higher than solid systems (ducted rockets sit between solids and ramjets at 800 seconds specific impulse). Ramjets have reached efficient cruise around Mach 4.5 in flight, while Scramjets have achieved efficient cruise at Mach 6-8. Such performance has been enabled by endothermic fuels, which decompose at high temperatures into lighter molecules that combust faster.

The limitation of ramjets, scramjets, and ducted rockets alike is the high speeds required to reach sufficient oxidizer flow in the combustion cycle, or to create more thrust than drag. Ramjets need to reach Mach 2.5, and scramjets need Mach 4.0. Both systems require a solid rocket booster to get to takeover speed, which means even an air-breathing missile is exposed to the AP supply chain.

In addition to reliance on solid boosters, ramjet inlet airframe integration (which requires chin inlets, mixed-compression configurations, and oblique-shock pressure recovery) is a real engineering burden and is part of why air-breathing tactical missiles haven't proliferated despite the performance advantage over pure solids. In addition to their reliance on AP-fueled solid boosters, these missiles depend on the similarly brittle supply chain of high-temperature alloys (Inconel, Rene, Hastelloy, Haynes).

As of May 2026, the Hypersonic Attack Cruise Missile program under the US Air Force, Raytheon, and Northrop Grumman is scramjet-based. Russia's Kh-31, Kh-41, and 3M80 missiles, and France's ANS and ASMP are ramjets operating in tactical roles (Russian Kh-31 and 3M80/Kh-41 use kerosene ramjets with solid boosters; French ASMP uses a kerosene-fueled ramjet with integrated solid booster).

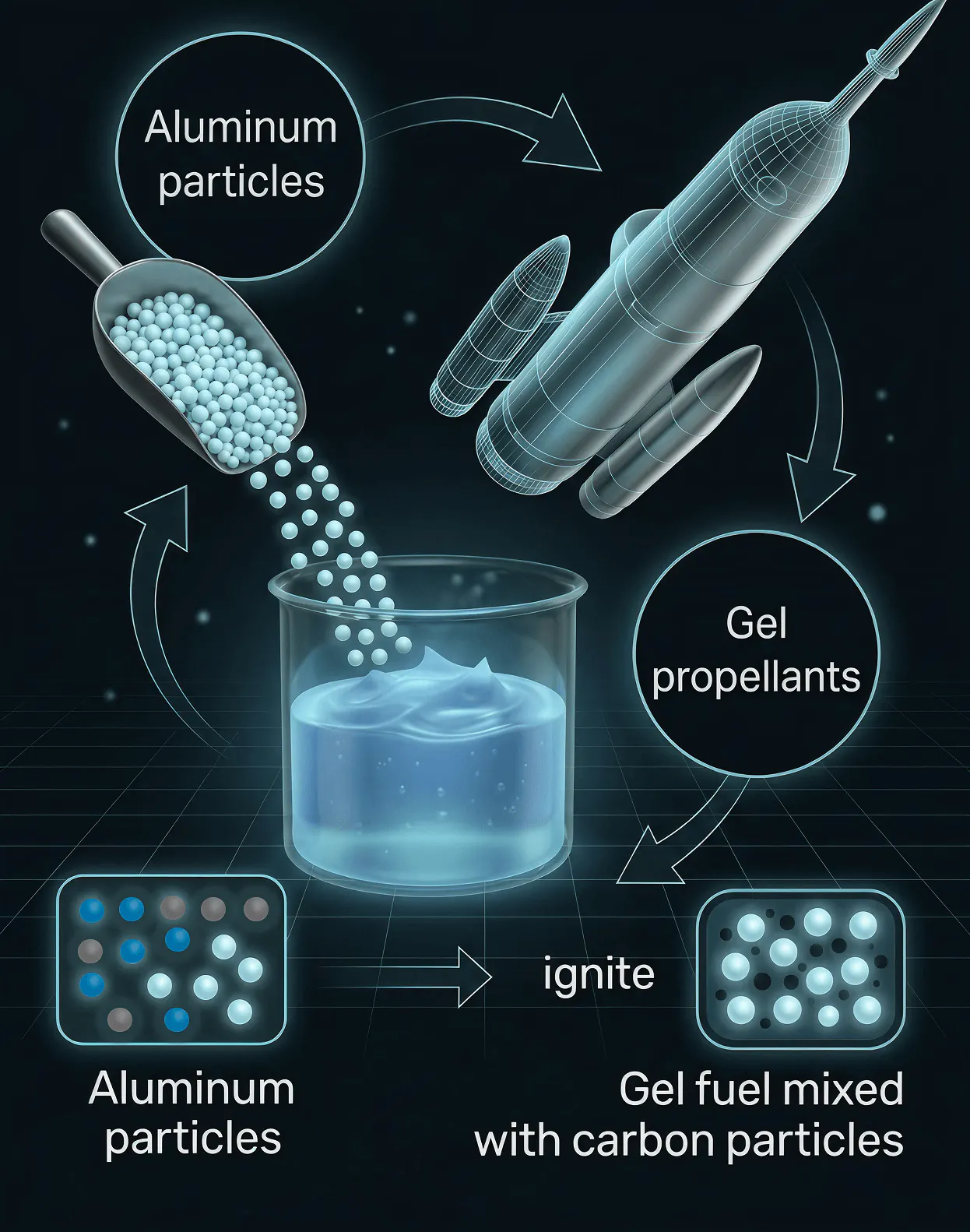

Gel Propellants

Defense contractors have explored several other early-stage alternatives to existing solid rocket motor systems. These include rockets fueled by gel propellants, which are formed by thickening liquid propellants with gelling agents to a non-flowing consistency. They combine the throttleability and high specific impulse of liquids with handling and storage characteristics closer to solids. Aluminum-loaded gels can exceed liquid hydrocarbon energy density, though the impacts on performance have not been tested extensively.

Source: MDPI; Contrary Research

The Defense Technical Information Center has flagged toxicity as the primary concern for gel propellant systems, particularly for naval applications. Hypergolic gel pairs (MMH/NTO derivatives) inherit the carcinogenicity and handling problems of their earlier liquid counterparts. Non-toxic gel formulations are being actively developed as alternatives.

Liquids as the Strongest Bet

Drawbacks to hybrid, air-breathing, and gel-based propulsion systems fundamentally limit their feasibility as replacements for solid rocket motor systems. Hybrid systems suffer from poor regression rates and combustion instabilities that have kept them out of fielded weapons despite ongoing technical advancements. Air-breathing systems need atmospheric oxygen and forward velocity to operate, requiring a boost from other missile types and ruling them out for exoatmospheric intercepts or high-thrust applications. Gel system chemistry is still immature and offers only marginal performance gains with added toxicity concerns.

Modern storable liquid bipropellants and pressure-fed designs have eliminated most of the old readiness objections, and, crucially, don't rely on ammonium perchlorate. The performance benefits of liquids and their straightforward supply chain make them the strongest candidate for replacing solid munitions at scale.

The Industry Landscape

For the last decade, US solid rocket motor production has been functionally a duopoly. Orbital ATK and Aerojet Rocketdyne had historically been the dominant suppliers of solid rocket motors to the US military and other defense hardware companies, prior to each’s acquisition by major defense primes. Northrop Grumman acquired Orbital ATK in 2018, and L3Harris acquired Aerojet Rocketdyne in 2023. During this period and in the years since, both incumbents and emerging aerospace neoprimes have experimented with a variety of approaches to addressing SRM missile supply chain limitations

Incumbents

L3 Harris

L3Harris is primarily a missile propulsion supplier rather than a missile prime. Solid rocket motors are the company’s primary output; L3Harris supplied the power stages for Javelin, Stinger, GMLRS, PAC-3, THAAD, the Standard Missile family (SM-2/3/6) via the Mk 72 booster and Mk 104 dual-thrust motor, and the LGM-35A Sentinel ICBM (where L3Harris also builds the liquid bipropellant post-boost propulsion system). On the air-breathing side, L3Harris makes the F107 turbofan that sustains the Tomahawk cruise missile and the scramjets used on the X-51A WaveRider and HAWC hypersonic programs, as well as throttleable solids as part of the TDACS divert/attitude system. The one place L3Harris is the missile prime is air-launched ballistic missile target vehicles, specifically MRBM Type 1/Type 2 missiles.

Production takes place in Camden, Arkansas, where L3Harris produces over 100K solid rocket motors per year, up from 75K per year before its 2025 expansion, line consolidation, and automation project (100K motors, not completed missiles, as multi-stage systems consume multiple tiny steering motors in addition to car-sized boosters). Capacity is being expanded under a $215.6 million DPA Title III cooperative agreement with the DoD, plus the $1 billion DoW investment closed in April 2026. The major sites being expanded include Camden (tactical SRMs), Huntsville, AL (a new 379K square foot inert-components plant), Orange County, VA (large strategic SRMs, expanding under the new Virginia Advanced Propulsion Facilities), and West Palm Beach, FL (air-breathing propulsion design). L3Harris also received a December 2025 letter of intent for 60 Zeus hypersonic motors from Kratos (a defense prime) and is targeting a 10X reduction in scramjet component build time via the GAMMA-H additive-manufacturing program.

Source: Zeus Hypersonic Motor; L3Harris

As of May 2026, L3Harris is spinning off its missile motor business, Missile Solutions, via IPO. In a first-of-its-kind partnership, the Defense Department is taking a $1 billion stake in the business ahead of an initial public offering later this year. Missile Solutions employs roughly 7K employees and posted ~$3.6 billion in revenue during 2025. CEO Chris Kubasik has framed this as "potentially starting a deconsolidation of the defense industry," reversing the 1990s-era roll-up. The Pentagon's "Go Direct-to-Supplier" initiative is the policy framework.

Northrop Grumman

Unlike L3Harris, Northrop Grumman is both a missile prime and a propulsion supplier, with the propulsion side coming largely from its $7.8 billion acquisition of Orbital ATK in June 2018, which folded the ATK solid rocket motor business into the new Northrop Missile Products unit. As a prime, Northrop builds the AGM-88E AARGM and its extended-range successor, the AGM-88G AARGM-ER (a supersonic air-launched anti-radiation missile with a solid rocket motor), the F-35-internal-bay AGM-88J Stand-in Attack Weapon (SiAW), and the LGM-35A Sentinel ICBM, a three-stage solid-propellant missile designed to replace the Minuteman III force.

As a propulsion supplier, Northrop produces the solid rocket motors for the Lockheed Martin Precision Strike Missile (PrSM), the Army's GMLRS and Hellfire rockets, and motors used across AMRAAM, Sidewinder, Stinger, the Standard Missile family, and Tomahawk. Northrop also makes the scramjet engine for the HACM Hypersonic Attack Cruise Missile and is the prime contractor for the Missile Defense Agency's Glide Phase Interceptor (GPI) against hypersonic glide vehicles (with L3Harris providing the boost motors).

Northrop says it has delivered over 1 million solid rocket motors over six decades but doesn't publish an annual figure; production is split across the Allegany Ballistics Laboratory in Rocket Center, WV (tactical SRMs including PrSM), Promontory and Magna, Utah (large strategic SRMs for Sentinel), and the 60K square foot Hypersonic Capability Center in Elkton, MD, opened in August 2023 for scramjet and ramjet production. Recent program demand includes a $235.7 million Lot 3 LRIP contract for 118 missiles in November 2023, with a sustainment plan covering 2,080 missiles through FY2051, plus FMS orders from Poland (360 missiles, $1.27 billion), the Netherlands (265, $700 million), Finland (150, $500 million), and Australia (63, $506 million). PrSM motors are being procured for a $4.9 billion indefinite delivery, indefinite quantity (IDIQ) contract awarded to Lockheed in March 2025 with a first delivery order of 400 missiles.

When Northrop acquired Orbital ATK in 2018, the FTC was concerned about vertical concentration with Northrop becoming a prime competitor with Lockheed and Raytheon on missiles, while also being the SRM supplier that those primes depend on. To approve the deal, the FTC imposed a consent order requiring Northrop to (1) supply SRMs to competitors on a non-discriminatory basis, and (2) firewall its SRM business, imposing hard internal information barriers so that proprietary data from Lockheed or Raytheon programs wouldn't leak to the Northrop missile prime arm.

Source: Northrop Grumman

In April 2026, Northrop petitioned the FTC to drop the consent order. Northrop argued that order is now obsolete because the SRM market has expanded beyond the old duopoly, with new entrants like Anduril and X-Bow and the $1 billion DoW investment in L3Harris's Missile Solutions spinoff. Lockheed Martin filed a comment in opposition in May 2026, arguing that the new entrants have not reached full-rate production and that Northrop remains the sole supplier of certain large SRMs.

Neoprimes

Anduril

Anduril* is a neoprime in the defense space, operating in both tactical software and hardware development. Anduril acquired Adranos in June 2023 to become a merchant supplier of solid rocket motors. Adranos was best known for its creation of ALITEC, an aluminum-lithium alloy fuel for solid rocket motors that it claims can produce up to a 40% range increase over traditional solid fuels. Anduril's acquisition of Adranos brought with it a 450-acre production facility in Mississippi. In March 2025, the US Army chose Anduril Rocket Motor Systems to develop a new 4.75-inch solid rocket motor for long-range precision rocket artillery.

Source: Anduril

The company began manufacturing the subsonic Barracuda cruise missile in 2024, and plans to build more than a thousand Barracuda-500 cruise missiles for foreign and domestic buys in 2026. Anduril created a "hyperscale production" strategy for Barracuda based on a simple design with fewer parts that uses commercial components and requires no more than 10 tools to assemble. The platform itself is air-breathing, not solid-rocket-propelled. But the missiles need to be launched from aircraft, which introduce some solid rocket motor dependencies. Production of 2K missiles per year takes place at the company’s manufacturing facility in Costa Mesa, California, and additional capacity is expected to be installed at the company’s upcoming Arsenal plant in Columbus, Ohio.

Castelion

Castelion was founded in November 2022 with the specific mission to create affordable, mass-produced hypersonic strike weapons by applying SpaceX-style fast iteration and vertical integration to munitions; the company was founded by a team of former SpaceX sales executives. The company’s flagship rocket is the Blackbeard hypersonic missile, which is powered by solid rocket propulsion. Rather than buying SRMs from L3Harris or Northrop Grumman, Castelion manufactures its own in-house.

In April 2026, the company won a $105 million US Navy contract to integrate Blackbeard onto carrier-based F/A-18 fighters, and the Army's RCCTO is separately funding a ground-launched variant under Project HX3.

The capacity for this build-out is concentrated in Project Ranger, a 1K-acre privately funded manufacturing campus in Sandoval County, New Mexico, that Castelion says it is building entirely with company money at a cost of about $220 million and that will be capable of producing thousands of Blackbeards per year by the end of 2026. Additional manufacturing operations in Texas (Allen and Midland) and California (in the company's new 90K square foot Torrance HQ).

Galadyne

Galadyne*, the newest addition to the missile manufacturing neoprime ecosystem, was founded by Chandler Luzsicza, who previously worked at Saronic and SpaceX as the lead propulsion engineer on Starship. Galadyne aims to apply SpaceX-style liquid propulsion economics to tactical missiles to achieve the scale of liquid missile production required to replenish US munitions stocks. The propulsion architecture is storable bipropellant: kerosene plus hydrogen peroxide, avoiding the ammonium-perchlorate energetics supply chain that bottlenecks every solid-rocket competitor. Liquid hydrogen peroxide and kerosene engines aren't unique to Galadyne (Ursa Major's Draper engine uses the same fuels), but Galadyne is the only company applying the combination as a full-stack missile builder rather than as a propulsion supplier. The company is actively developing the Striker missile for offensive strike and the Defender architecture for intercept (the latter pairing the rocket with an in-house exoatmospheric kill vehicle for next-generation interceptor missions).

Galadyne’s missiles are designed around a containerized launch system that integrates propellant handling, fueling, and launch infrastructure into a single deployable unit intended to remove the logistics-tail bottlenecks that constrain scaling of conventional liquid missile fielding. Manufacturing is being stood up in Texas, with Galadyne targeting the first full-scale missile test launch in June 2026.

X-Bow Systems

Founded in 2016, X-Bow is an emerging player in the solid rocket motor market, using 3D printing technology to produce motors and propellants. The company claims this approach significantly reduces production time and costs compared to traditional methods. Its proprietary process is called Advanced Manufacturing of Solid Propellant (AMSP). In this process, the company uses 3D printing to create the grains in casting (additive-manufactured grain geometries enable performance configurations that can’t be produced by cast-and-pour processes), but still relies on the same upstream energetics supply chain for AP as other solid rocket motor producers.

Source: Tectonic Defense

X-Bow’s SRM portfolio now spans Mk 72 boosters and Mk 104 dual-thrust motors for the Navy's Standard Missile family (PDR completed January 2026), a next-generation GMLRS motor under a $13.9 million joint investment between the Army and the Office of Strategic Capital, a $64 million DoD contract for large-diameter hypersonic SRMs (developed with Leidos Dynetics, Karman Space & Defense, and NSWC Indian Head), MK-290 replacement igniters under a V2X production contract, and X-Bow's own Bolt-family rocket motors. Production is concentrated at the company’s gigafactory SRM campus in Luling, Texas.

In May 2025, X-Bow announced the successful final closing of its Series B funding round, totaling $105 million. The strategic portion of this round was led by Lockheed Martin, which is a customer of X-Bow.

Ursa Major

Originally a liquid rocket engine company, Ursa Major is a neoprime building both liquid and solid engines and missiles as of May 2026.

Ursa Major’s first liquid motor was the 5K-pound-thrust Hadley engine, scaling production to one per week in 2023, and qualifying Hadley as the world's first rocket engine for space launch, in-space, and hypersonic missions. The company’s newest liquid motor, Draper, is a reusable liquid engine designed to remain storable for over a decade. The reusable engine is mostly 3D-printed and runs on non-cryogenic, non-toxic propellants (hydrogen peroxide and kerosene), unlike earlier Ursa Major liquid motors that run on liquid oxygen.

In 2023, Ursa Major introduced its Lync 3D-printed SRMs, which are operating on a shared machinery line that enables switching between specific motor types. In September 2024, Ursa Major was chosen by the DoD as one of the inaugural recipients of investments from the Office of Strategic Capital, with a $12.5 million joint investment in partnership with the US Navy to mature the Lynx process. In 2026, Ursa Major secured a US Navy contract to develop and hot-fire test a next-gen Mk 104 solid rocket motor.

The Path Forward

America's missile production hinges on a small number of ammonium perchlorate facilities, meaning a single plant accident can bring output to a standstill; a concentration risk that has no real equivalent elsewhere in the defense industrial base. AP production relies on narrow workforce pipelines for specialized energetics handling, layered environmental and explosives permitting, and purpose-built manufacturing equipment. Each of these inputs is hard to duplicate quickly, even with dedicated funding, which is why decades of rhetoric about supply chain expansion have produced so few second sources in practice.

Expanding the US missile supply will require not only innovation and scaling from private contractors, but also coordinated partnership with federal policymakers to enact some combination of permitting reform for energetic-materials facilities, investment in second-source AP and binder supply, and demand-signaling to revive liquid-propulsion munitions. Of these, demand-signaling for liquid propulsion is the lever most likely to produce capacity on a practical timeline because it avoids the AP bottleneck entirely.

In the near future, solids may remain dominant for ICBMs, MANPADS, and many tactical roles where their attributes are important, but reforming their supply chain will take too long to restore US production capacity and point-in-time stockpiles. The current solid-dominant posture is a legacy of Cold War survivability requirements, which are no longer relevant for most of the missions the United States now relies on (like anti-ship strike from distributed maritime platforms, long-range conventional fires, and attritable munitions launched from autonomous vessels). For those mission sets, the relevant question is no longer which munitions are simpler or safer to launch, but rather which munitions can be manufactured in the thousands of rounds per year using inputs already produced at industrial scale.

Liquid propulsion answers this question with commoditized hydrocarbon fuels, high-test peroxide, and the engine design advances driven by commercial analogs. Most importantly, these inputs are available at scale with dozens of industrial sources across the country, not just half a dozen. While a new AP facility could take more than 10 years to come online, a credible liquid-propulsion alternative is a matter of months out at the platform level and only 1-2 years from platform scale. The propellant chemistry is mature, the supply chain already exists at commercial scale, and engine production lines can be stood up using contract manufacturing rather than purpose-built energetics plants. The binding constraints to scaling are known engineering problems rather than industrial base problems requiring greenfield construction. Developing an alternative propulsion supply chain based on commercially manufactured hydrocarbons and peroxide should not be a hedge against solid-rocket-motor capacity, but the primary path to expanding munitions capacity on a practical timeline.

*Contrary is an investor in Anduril and Galadyne through one or more affiliates